Sample Category Title

SNB’s Martin: Negative rates a possibility, but not on immediate agenda

SNB Vice Chair Antoine Martin indicated that the central bank may consider lowering interest rates, potentially even taking them into negative territory, as a tool to support the economy.

Speaking at an event overnight, Martin said "with inflation being reasonably low in Switzerland and with an economy that could grow faster, that tends in the direction of a lower policy rate,"

He further remarked that negative rates, although not imminent, remain a useful tool in the central bank's arsenal, stating, "There are imaginable scenarios where this is a tool that we would use because it's a particularly useful tool."

"But we're not today in a situation that this is something that we're considering," Martin added.

700 Reasons to Expect Higher Real Rates on Average

Now that central banks are cutting rates, the question of where they will stop comes into focus. Real rates have trended down for decades, but a very long-term view supports our thesis that rates will average higher in future than they did pre-pandemic.

Most peer central banks are already cutting rates and some are front loading the cuts. The Fed and the RBNZ have seemingly declared 50 to be the new 25, though it is not clear that the FOMC will continue at that pace. The ECB may also want to pick up the pace to offset fiscal consolidation, as Westpac economics colleague Illiana Jain points out in her piece in our latest Market Outlook report released this week.

Steep hiking phases followed by equally steep cutting phases may well be a general pattern when an inflation surge is largely driven by supply shocks that unwind of their own accord. Unlike the more organic sources of strong demand that central banks usually contend with, the demand component of the current inflation shock has also been partly self-correcting, driven as it was by pandemic-era stimulus. It should be no surprise then that the economies with some of the sharpest rate cycles – the United States and New Zealand – had ongoing fiscal stimulus after the pandemic.

While the need to reduce the restrictiveness of policy in these economies is clear, it is less obvious where policy might need to land to no longer be restrictive. The so-called neutral rate is uncertain. And as the FOMC ‘dot plot’ estimates for the long-run fed funds rate show, policy makers are even less sure about its level than in the past. While their views have diverged, all FOMC members are agreed that it is probably higher than was believed before the pandemic. This lines up with our long-standing house view that the global structure of interest rates is likely to be higher on average than it was between the GFC and the pandemic. The era of negative yields is over.

The rate that neither stimulates nor weighs on inflation at any point is also the rate that balances desired saving and investment. It will depend on whatever else is going on, including the drag or stimulus from fiscal policy. It is because of these other things that we expect a higher average rate structure. European governments need to consolidate, but as Iliana points out, by less and in a less abrupt manner than in the early 2010s. Western governments more generally are facing greater demands to spend on defence, energy transition and to meet the needs of an ageing population. The private sector, too, has more need to invest now, on energy transition and the energy demands of AI. It also has a bit more scope to do so given that Western banking systems are less constrained by the need to build up capital to meet the requirements of the Basel 3 rules. Asian economies remain an important source of saving, but not more than they were in the first two decades of the century. They might even be less of a saving source, depending on how large the stimulus is in China.

All of this is a guide to what central banks need to do to achieve their desired policy stance in the moment. It says less about where the rate structure is likely to gravitate to in the long run, when all the current shocks have played out. The answer to that question is also often labelled the ‘neutral rate’, a little confusingly. (Some researchers attach an extra star to their notation distinguish between these concepts.) This longer-term version is less of a guide to central bank decision-making now, and more of an anchor for pricing very long-term debt securities.

A plague on all your 20th century trend estimates

This long-term anchor concept still boils down to the rate that balances global saving and investment on average. But now we must consider the deeper and more structural drivers of those forces, and whether there are structural trends. A large body of research notes the downward trend in both short-term and long-term real interest rates. So far, though, there has been no consensus on the reasons for this.

Some recent research by Kenneth Rogoff, Barbara Rossi and Paul Schmelzing might provide some insights. They have compiled data on real long-term bond yields going all the way back to the year 1311, more than 700 years. An achievement in itself, their dataset shows that there has indeed been a slight downward trend over this longer period. Crucially, though, the period between the GFC and the pandemic was in fact a downward deviation from that trend. The authors therefore expect some reversion to trend in coming years. This contrasts with papers using shorter data sets, where the downward trend is less precisely estimated.

It is important not to take this purely empirical observation as gospel. We do not yet know why there is a downward trend, or what might be the cause of the recent downward deviation. There are, however, some reasonable hypotheses. Recall that these are long-term real bond yields not the short-term rates used by central bankers to set policy. The market and policy apparatus the shorter rate applied to came in many centuries later than long-term sovereign bonds. It may be that the trend comes from a trend in the term premium or risk premium, rather than from the neutral short-term rate as we think of it now. For example, it could be that as experience with long-term debt markets increased, and governments became better at keeping their financial promises, investors among Europe’s Early Modern elites became more trusting over time and demanded a smaller term/risk premium over the (unobserved) ‘true’ risk-free rate.

Some other suggestive possibilities can be inferred from the fact that there was a break upwards in the trend following the Black Death in the 1340s, when one-third to a half of the population of Europe perished. If the underlying trend in interest rates reflects people’s willingness to wait until tomorrow, their need to be compensated for waiting will reflect their beliefs about how likely it is that they will even survive until tomorrow. Events like the Black Death surely shifted that subjective belief.

More broadly, rising longevity – or more precisely, greater certainty about your adult longevity – could be one of the reasons why people have seemingly become more patient and willing to accept less compensation for waiting, that is, a lower long-term interest rate. (The authors cite other research suggesting that elite males – the segment of the population who would have cared about yields on sovereign debt back then – were less likely to die in battle from the 1400s. That would have helped start the downtrend after the increase following the Black Death.) That is a reason to expect a slow downward trend, and to not assume that a lurch down after the GFC was permanent. There is a common thread here with other literature, including work from the Bank of Canada that focused on the need to save for longer (and more certain) retirements.

The academic debate remains unresolved. For anyone thinking about pricing bonds or planning fiscal policy, though, some of the latest research suggests it would be foolhardy to assume that the low-rates world of the GFC-to-pandemic period will continue.

Cliff Notes: Shifting Views on the State of the Economy

Key insights from the week that was.

In Australia, there was finally a sigh of relief for consumers as October’s Westpac-MI Consumer Sentiment Survey reported a 6.2% increase in the headline index to 89.8, a two-and-a-half year high. The chief culprit behind this improvement was a significant pull-back in interest rate hike fears, as consumers take the cue from lower measured inflation and the broader global economic backdrop, which has seen many other peer economies begin to lower interest rates. This led consumers to have a much more positive view on the economy, with the sub-indexes tracking the 12mth and 5yr ahead view up 14.3% and 8.0% respectively in the month. Meanwhile, the progress on family finances remained relatively more subdued, highlighting the extent to which cost-of-living pressures have loomed over households. While pessimism still dominates overall, this marked one of the most constructive single-month reads since the RBA began raising interest rates.

This backdrop bodes relatively well for businesses too, given that both business and consumer confidence tend to move together over an economic cycle. On the conditions front, the latest NAB business survey also suggested that business conditions have found somewhat of a ‘floor’ over the course of this year. This is consistent with our view that economic activity is current around its nadir, having slowed to 1.0%yr in Q2 2024. In a context of recent tax cuts and monetary policy easing on the horizon, there is certainly scope for further improvement in sentiment and, hence, consumer spending. We are forecasting a recovery in growth hereafter to a pace of 1.5%yr by year-end and 2.4%yr in 2025. For more detail behind our view and forecasts, please see our latest Market Outlook published on WestpacIQ.

The RBA’s September Minutes provided another opportunity to digest the Board’s views on the balance of risks. There were two important developments on this front. Firstly, on the topic of the supply-demand balance, the RBA acknowledged that momentum in demand was weaker than initially expected. This, in effect, toned down some of their hawkishness on inflation from August, when the Board was telegraphing a more pessimistic view on supply potential. Secondly, there was a larger emphasis on assessments of financial conditions and the risk that they could turn out to be insufficiently restrictive to return inflation to target. We will continue to watch how the discussion of these points evolves over the coming months, but for now, the RBA’s focus is clearly squared on the dynamics around underlying inflation. We continue to expect the RBA to deliver its first rate cut in February 2025, before reaching a terminal rate of 3.35%. In this week’s essay, Chief Economist Luci Ellis details the longer-run trends guiding our thinking behind the global interest rate structure.

Offshore, the focus remained on US monetary policy.

Before jumping into this week's events, a quick note on the September non-farm payrolls print released late last week. Non-farm payrolls surprised to the upside rising 254k and exceeding the median market expectations of 150k. There was also an upward revision of 72k for the previous two months, attributed to a recalculation of seasonal factors. The unemployment rate inched down to 4.1%, 0.3ppt below the FOMC's forecast for Q4 2024. And the average hourly earnings rose by 0.4%mth with annual growth at 4.0%yr, up from 3.6% in July.

This week, minutes for the FOMC's September meeting were released. They showed that both 25 and 50bp cuts were on the table and the committee chose to go with the latter. Interestingly, several members argued that a 25bp cut was more consistent with a gradual path to easing as well as providing a degree of predictability. And the committee expressed concern about how the 50bp cut will be perceived with the minutes noting that “it was important to communicate that the recalibration of the stance of policy at this meeting should not be interpreted as evidence of a less favorable economic outlook or as a signal that the pace of policy easing would be more rapid than participants’ assessments of the appropriate path”. With regards to the FOMC’s assessment of the US economy, the labour market was perceived to be close to the long-run maximum employment, and less tight than prior to the pandemic. Risks of its further unwanted deterioration were assessed to have increased (this is before the release of the September jobs data). And the FOMC had greater confidence in inflation's return to 2.0% noting upside risk had 'diminished'.

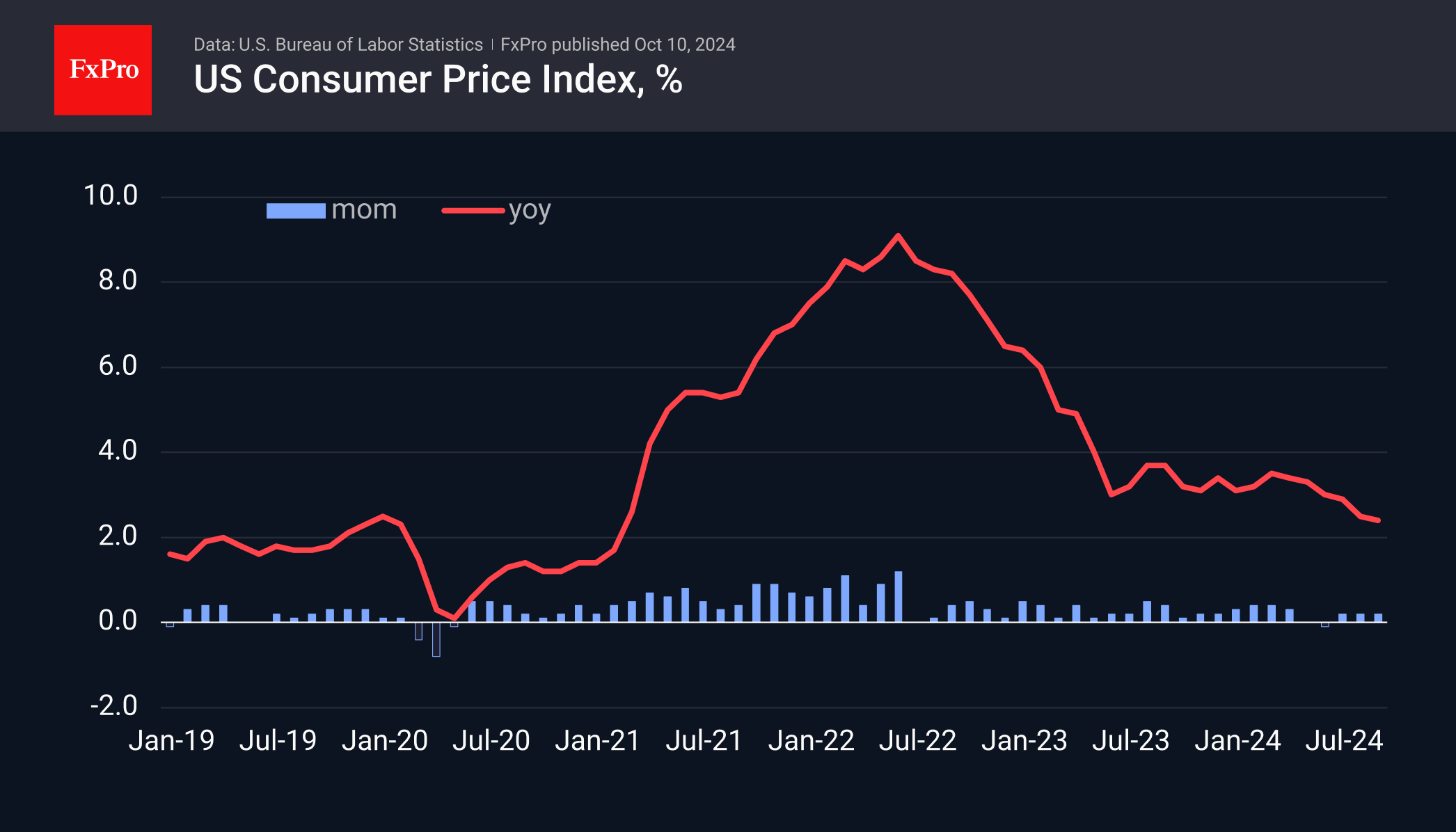

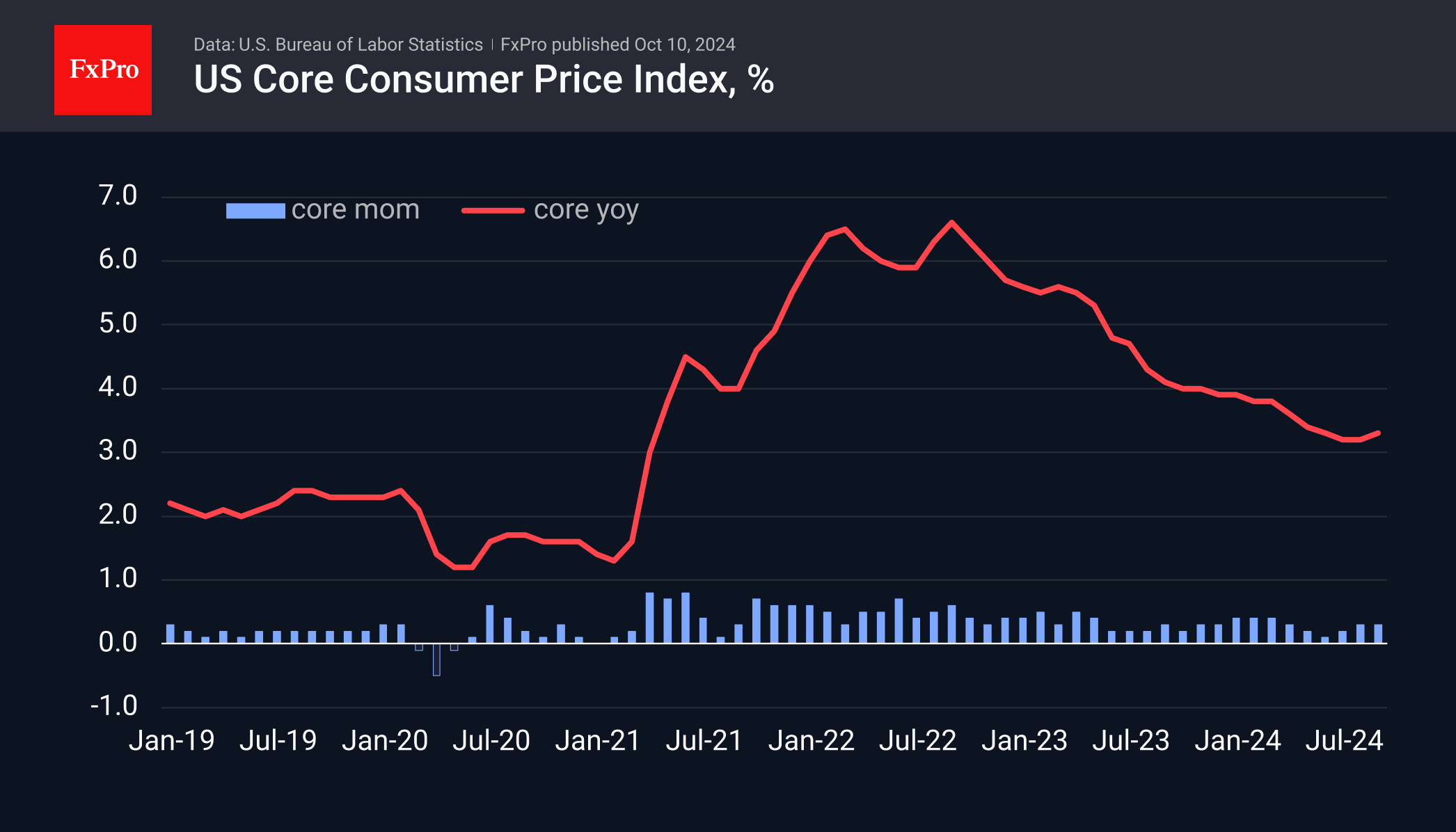

On the face of it, this week’s CPI data release for September was somewhat inconsistent with FOMC’s assessment, with both the headline and core CPIs rising slightly more than expected, by 0.2%mth and 0.3%mth respectively. Both rates were unchanged from August and fully in line with the averages over the last twelve months suggesting that inflationary pressures in the US remained stable last month. But details suggested that the upside surprise was accounted mainly by higher inflation in the core goods category and quite volatile items in it. The shelter component, one of the key drivers of headline inflation, showed that prices increased by 0.2%mth, half the average pace seen in 2024 so far. Ex-shelter, the annal CPI growth rate was just 1.1%yr. Subsequent comments from the FOMC members downplayed the importance of the September CPI print suggesting they are continuing to focus on the longer-term decline in inflation.

Closer to home, the Reserve Bank of New Zealand cut the overnight cash rate by 50bp to 4.75% in line with expectations. The move was driven by an assessment that the economy has excess capacity which should facilitate lower price and wage-setting behaviours. “Subdued” economic activity and employment conditions which continue to “soften” were credited to the still-restrictive monetary policy stance. Westpac expects another 50bp cut to come in November and for the policy rate to fall to a low of 3.75% in 2025.

US Data: Stubborn Inflation vs Jobs Warning Bell

US inflation came in slightly above expectations, but a jump in weekly jobless claims shifted the focus to the need for further policy easing, dampening speculation that the Fed may not cut rates in November.

Consumer prices rose 0.2% m/m in September, the same as the previous month, while annual inflation slowed from 2.5% to 2.4%, above expectations of 2.3%. Housing and food were important drivers, accounting for three-quarters of the total price increase.

The core index, which excludes energy and food prices, accelerated its annual growth rate from 3.2% to 3.3%, the first acceleration in a year and a half. This proves that slowing inflation is no easy task in the context of full employment and is mediated by low oil and fuel prices.

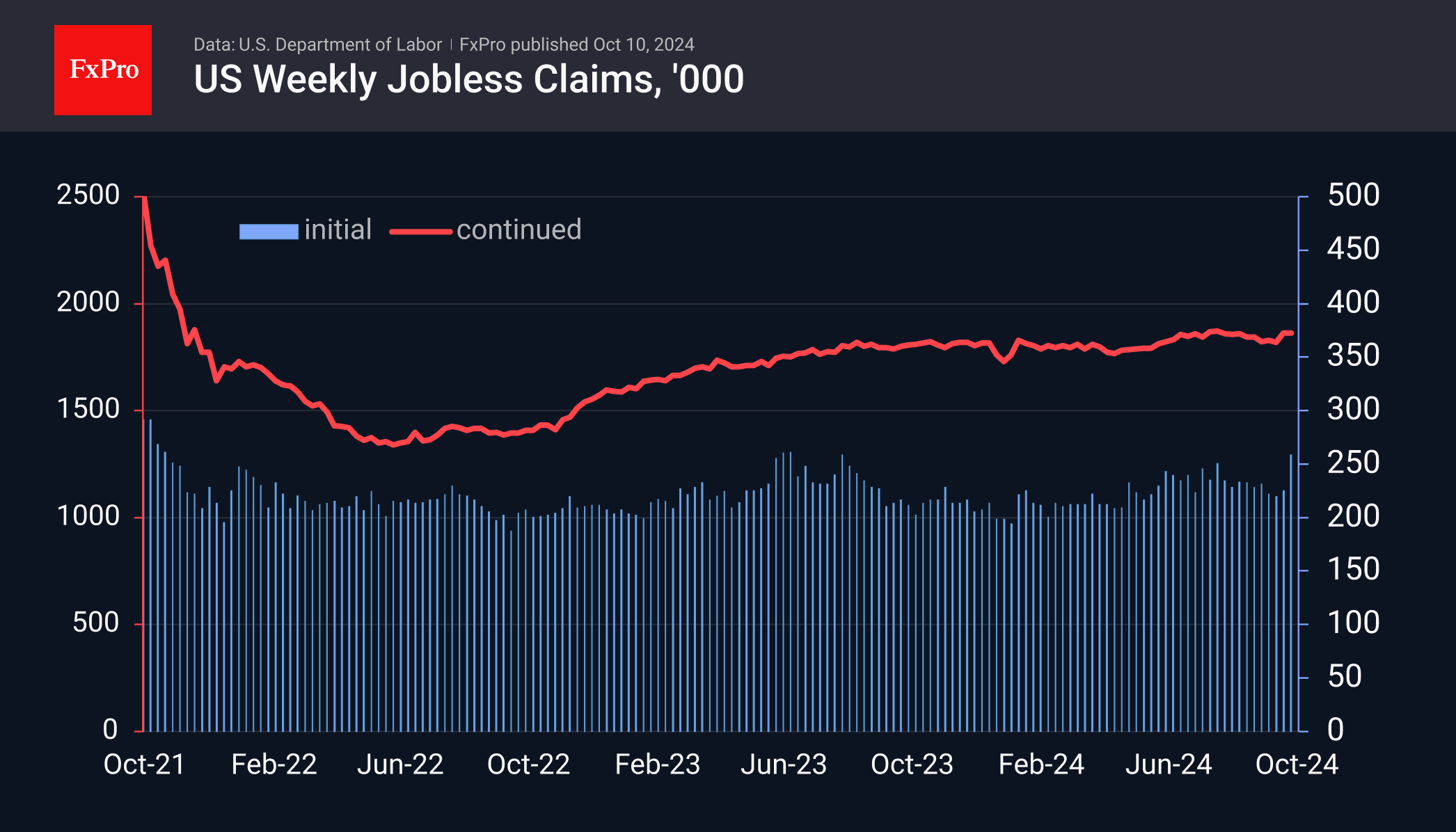

The impact of accelerating core inflation—usually a bullish factor for the dollar—was overwhelmed this time by an unexpected jump in jobless claims last week. Initial claims were reported to have risen to 258K from 225K the previous week and an expected 231 K. The current level is the highest since last August and the fourth highest in almost three years as the US labour market recovered from the shutdown shock.

About two months ago, financial markets reacted nervously to employment signals, but the return of weekly claims to normal levels reassured investors that we were seeing a short-term spike rather than a trend reversal. Now, the situation is reversed: strong NFPs versus the alarm from the weekly numbers.

The dollar fluctuated between 0.4% and 0.1% in the first moments after the data was released but has only lost 0.1% at the time of writing on such conflicting data. Perhaps investors will now eagerly look for signals from Fed members to learn their assessment of the situation, which the market will follow.

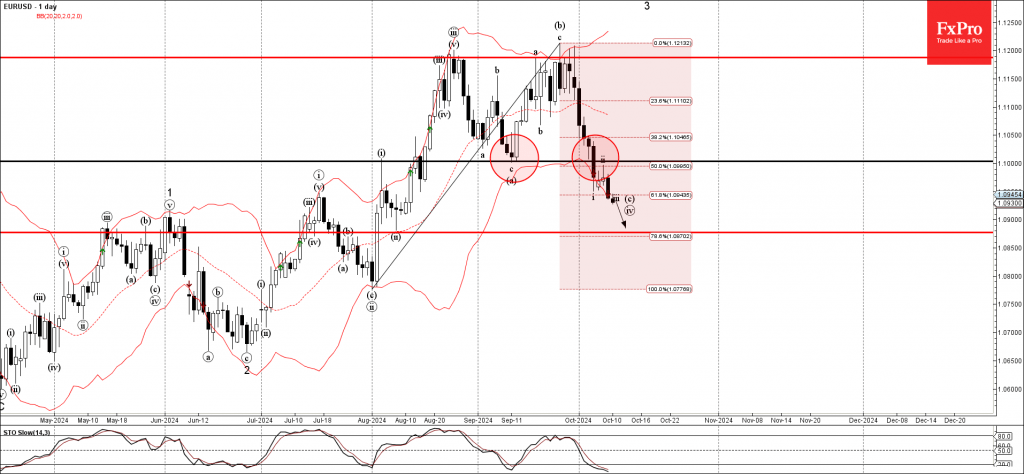

EURUSD Wave Analysis

- EURUSD broke support zone

- Likely to fall to support level 1.0875

EURUSD currency pair under the bearish pressure after the earlier breakout of the support zone located between the key support level 1.1000 (former monthly low from September) and the 50% Fibonacci correction of the upward impulse from July.

The breakout of this support zone accelerated the active minor impulse wave c of wave (iv) from the end of August.

Given the simultaneously bearish euro sentiment and bullish US dollar sentiment, EURUSD currency pair be expected to fall further to the next support level 1.0875, low of wave ii from August.

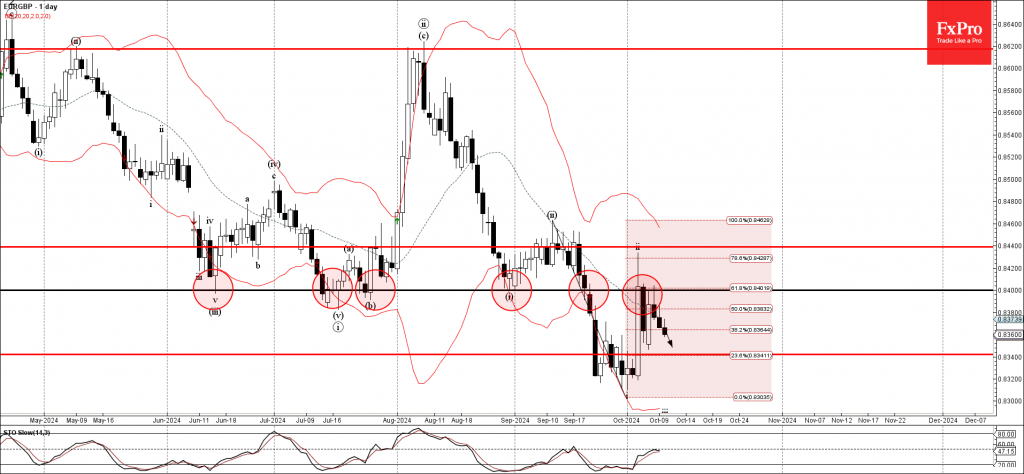

EURGBP Wave Analysis

- EURGBP reversed from resistance zone

- Likely to fall to support level 0.8340

EURGBP currency pair recently reversed down from the resistance zone located between the key resistance level 0.8400 (former strong support from June, July and August) intersecting 20-day moving average and the 618% Fibonacci correction of the downward impulse from September.

The downward reversal from this resistance zone started the active minor impulse wave iii.

Given the strongly bearish euro sentiment seen today and the clear daily downtrend, EURGBP currency pair be expected to fall further to the next support level 0.8340.

Fed’s Williams expects gradual move toward neutral policy

New York Fed President John Williams signaled today that monetary policy will continue to shift towards a more neutral stance in the coming months, aligning with ongoing progress toward price stability. He emphasized that while inflation remains above the 2% target, there has been clear movement in the right direction.

Williams noted, "Based on my current forecast for the economy, I expect that it will be appropriate to continue the process of moving the stance of monetary policy to a more neutral setting over time." He reiterated that this approach will help preserve both the economy's strength and the health of the labor market.

While acknowledging the work still needed to achieve price stability, he expressed optimism, stating, "The data paint a picture of an economy that has returned to balance." Despite inflation remaining elevated, the message from Williams was one of cautious confidence, suggesting the Fed’s shift towards less restrictive policy will proceed gradually.

Fed’s Goolsbee expects more close calls ahead on rate decisions

Chicago Fed President Austan Goolsbee, in an interview with CNBC today, highlighted the clear progress made in curbing inflation and cooling the labor market over the past 12 to 18 months.

“The overall trend... is clearly that inflation has come down a lot and the job market has cooled to a level which is around where we think full employment is,” Goolsbee stated.

Looking ahead, he noted there is broad consensus among policymakers that interest rates will need to drop a “fair amount” over the period.

However, in the near-term, Goolsbee expects more "close call" meetings for FOMC as members navigate through sometimes conflicting economic data.

Sunset Market Commentary

Markets

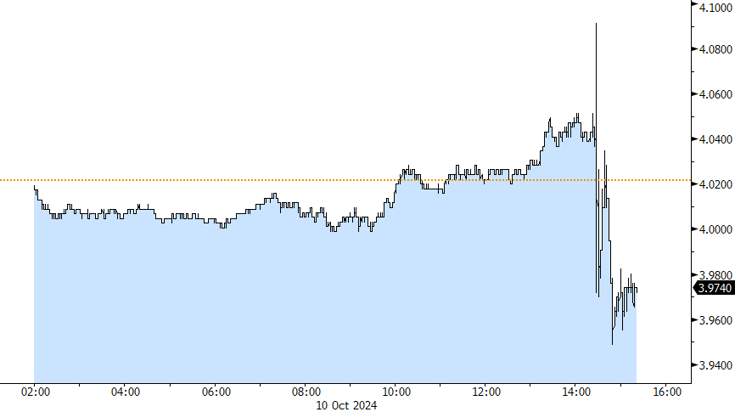

Data dependency = volatility. Today was a textbook example. The US economic agenda featured September CPI figures and the weekly jobless claims. The former came in at the topside of expectations with headline and core coming in at 0.2% and 0.3% m/m respectively, beating the consensus view by 0.1 ppt each. The yearly print as a result eased a little less than hoped-for in headline terms, from 2.5% to 2.4% and unexpectedly accelerated in the underlying gauge to 3.3%. Energy prices were a drag last month, falling almost 2% on a monthly basis, but food prices (0.4%) rose at fastest pace in about two years. Shelter prices, known for their stickiness, only rose by 0.2%, matching June’s low print which was in turn the slowest advance since August 2021. Offsetting this, however, is the quickening in core services ex housing inflation, a metric watched closely by the Fed. With the 0.4% m/m outcome, the annualized 3mMA is nearing 4% again. The broader services inflation gauge stood at 0.4% and 4.7% y/y. Bond yields’ first reaction was to extend previous daily gains with the 2-yr yield spiking to the highest level since mid-August. Enter weekly jobless claims. A big jump from 225k to 258k crushed expectations for a much more modest rise to 230k. States including Florida and North Carolina printed some of the biggest increases, revealing an impact from hurricane Helene. The upcoming readings may be affected similarly (hurricane Milton). The jury’s still out whether it turns out to be a temporary effect but since the Fed is now laser-focused on the labour market it does dictate the market reaction. Front-end yields in the US swapped intraday gains of as much as 7 bps for losses around 4 bps. But that’s nowhere near enough to table the idea of a 50 bps Fed cut in November again though. Current pricing still doesn’t fully discount a 25 bps move, even after today’s repositioning. Swings at the long end of the US curve were much more muted. The likes of the 10-yr trade flat. European/German yields pared earlier gains of 2-3 bps to around 1 bp. The dollar’s intraday volatility eventually ended up in small losses. EUR/USD rebounded from a 1.0910 low to 1.0948 currently. DXY’s trip above 103 ended quickly (102.83).

News & Views

Prices in the Czech Republic declined -0.4% M/M, its statistical office published today. KBC expected a decline of 0.6 M/M. Due to an even sharper decline last year (base effects) the monthly decline still raised the Y/Y measure from 2.2% in August to 2.6% September. The monthly decline in prices was, amongst others, driven by a 20.9% decline in the prices for package holiday. Prices of fuels for personal transport also declined 4.9% M/M. Monthly prices rises mainly came from higher food prices (0.8%) and of costs related to education (+10.6% M/M). Y/Y goods and services prices went up by respectively 1.2% and 5.0%. The September outcome was 0.3% higher than the CNB summer forecast, but in a brief comment today, CNB indicated that core inflation was slightly below the forecast. Still, today’s report suggests that headline inflation might move to/or even above the 3.0% CNB tolerance band by the end of the year, before easing again in early 2025. KBC maintains a scenario of gradual easing (25 bps steps) from 4.25% currently to 3.50% in February 2025. The policy rate then might stay at that ‘new equilibrium level’ for a longer period. The koruna trades little changed near EUR/CZK 25.32.

Hungarian inflation slowed more than expected by -0.1% M/M and 3.0% Y/Y (from 3.4%). Headline inflation returned to the MNB 3.0% target for the first time since January 2021. Analysis of the MNB tells that inflation of tradables declined 0.7% M/M to ease to 1.6% Y/Y. Market services prices increased 0.1% M/M holding the Y/Y-measure at 9.6%. Core inflation measures showed a mixed picture (core ex indirect taxes 4.8% from 4.6%, CPI ex processed food 5.5% from 5.8%, sticky price CPI 5.4% from 5.8%). After a pause in August, the MNB again eased the policy rate by 25 bps (to 6.5%) in September. We expect the MNB will (have to) stick to a cautious approach. Both core and inflation are expected to turn higher again toward the end of the year. As the forint weakened north of EUR/HUF 400, financial stability concerns will again get a bigger weight in the MNB assessment. In this respect deputy Governor Virag earlier this week indicated that chances of a skip at the October 22 meeting have grown. Lingering political tensions with the EU and market concerns on fiscal consolidation also don’t help the forint. The Hungarian currency declined from the EUR/HUF 399 area this morning to 400.6 currently.

Graphs

US 2-yr yield whipsawed on simultaneous release of stronger-than-expected CPI and surge in jobless claims

EUR/CZK: Czech koruna trades unchanged vs opening levels. September CPI won’t alter CNB’s gradual approach

EUR/HUF: below-consensus CPI doesn’t pave the way for further easing with forint again in the defensive

EUR/NOK: Easing Norwegian core inflation to nudge Norges Bank a bit further towards inaugural December cut?