Sample Category Title

EUR/GBP Weekly Outlook

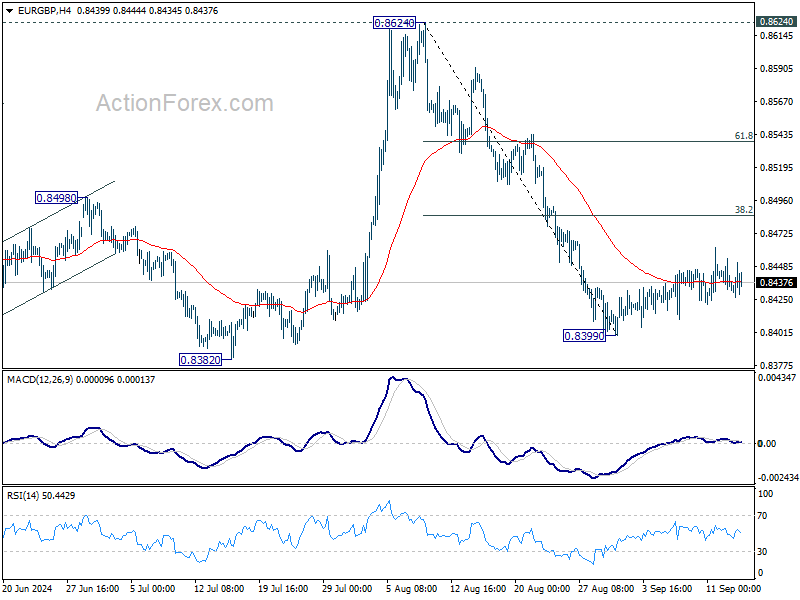

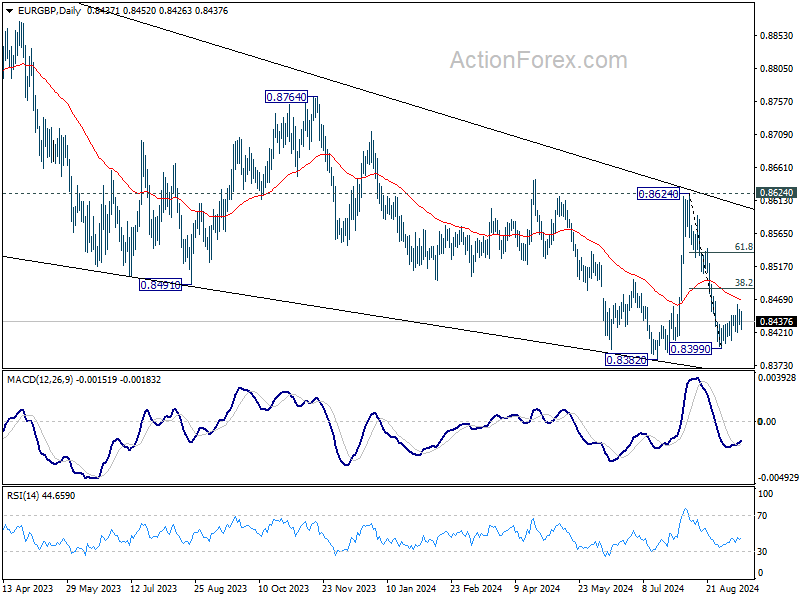

EUR/GBP was still bounded in consolidation above 0.8399 last week and outlook is unchanged. Stronger recovery might be seen but upside should be limited by 38.2% retracement of 0.8624 to 0.8399 at 0.8485. Break of 0.8399 will bring retest of 0.8382 low. Firm break there will resume larger down trend. However, sustained break of 0.8485 will bring stronger rally to 61.8% retracement at 0.8538 and possibly above.

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

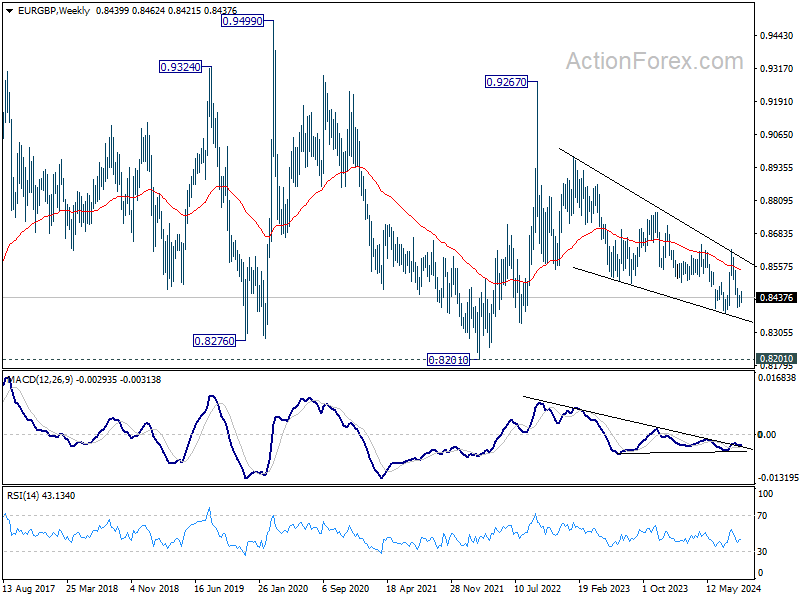

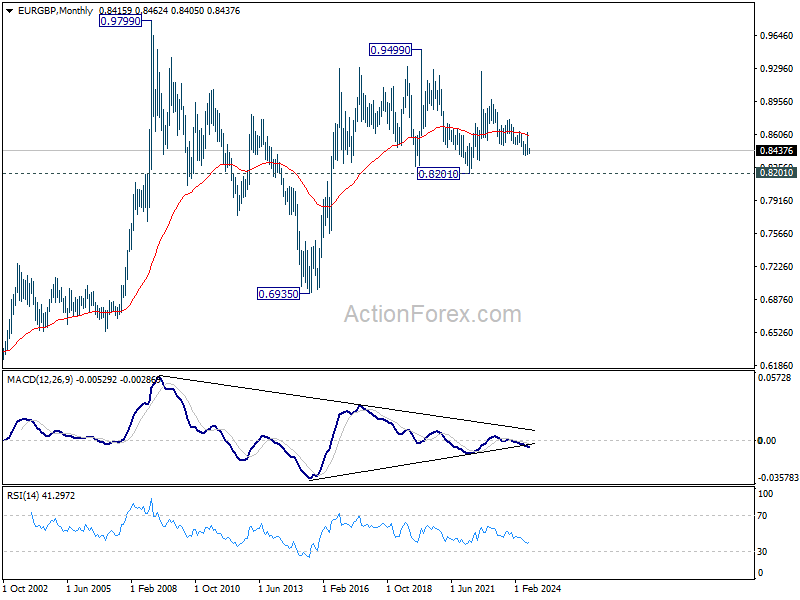

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

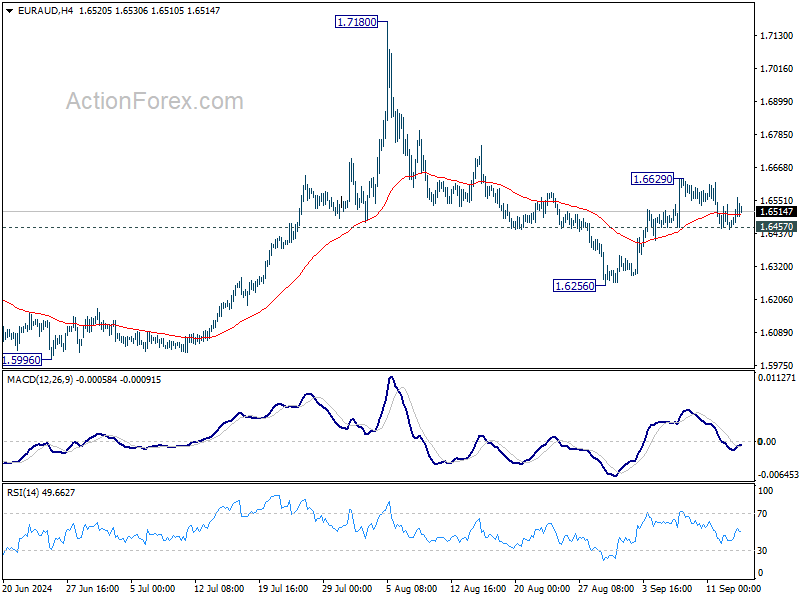

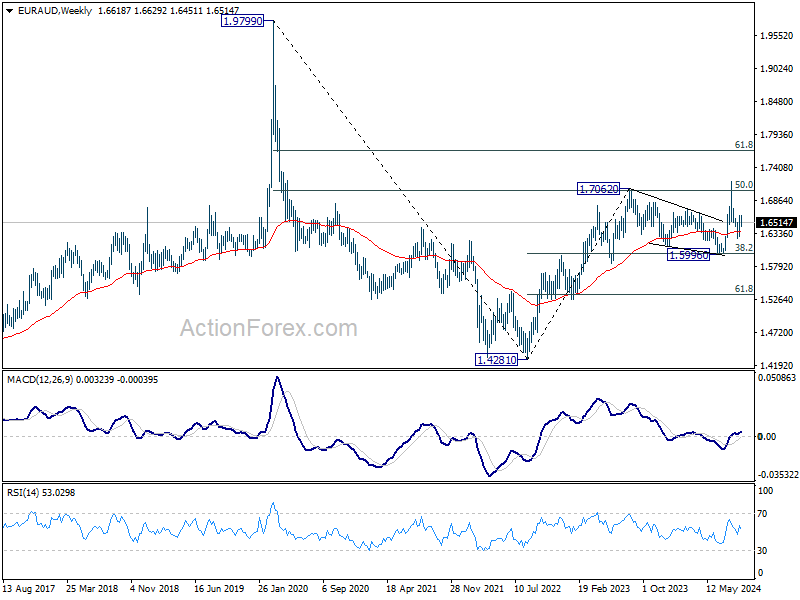

EUR/AUD Weekly Outlook

EUR/AUD retreated after edging higher to 1.6629 last week. Initial bias stays neutral this week first. For now, the favored case remains that corrective fall from 1.7180 has completed at 1.6256 already. On the upside, above 1.6629 will resume the rebound for retesting 1.7180 high. However, firm break of 1.6457 minor support will dampen this week and turn bias back to the downside for 1.6256 again.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still in favor to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

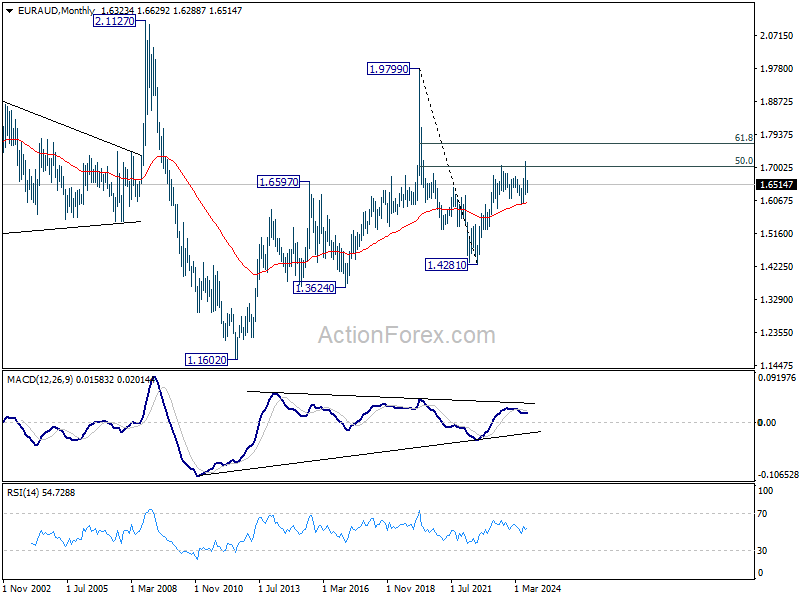

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5999) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

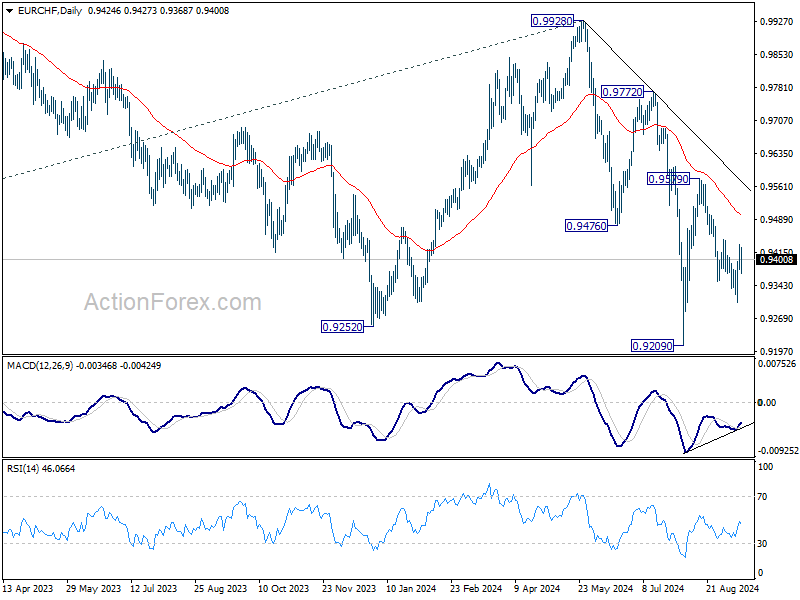

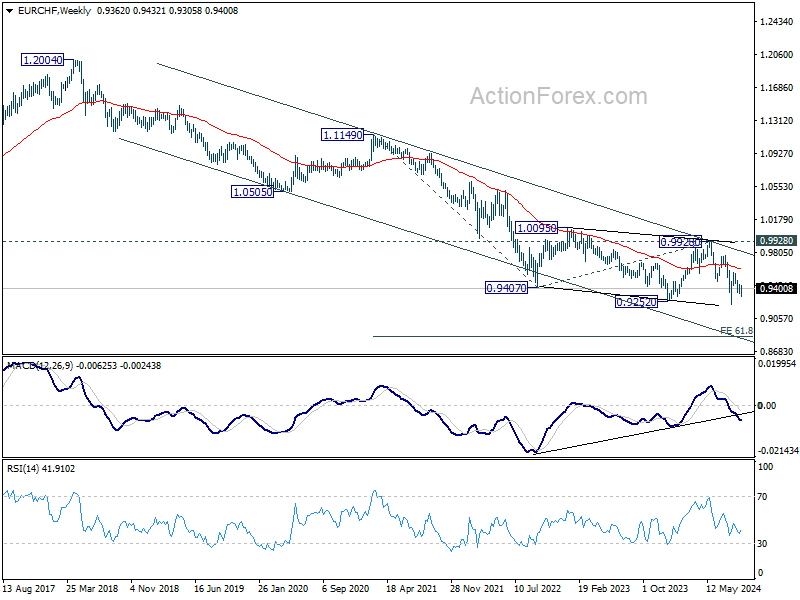

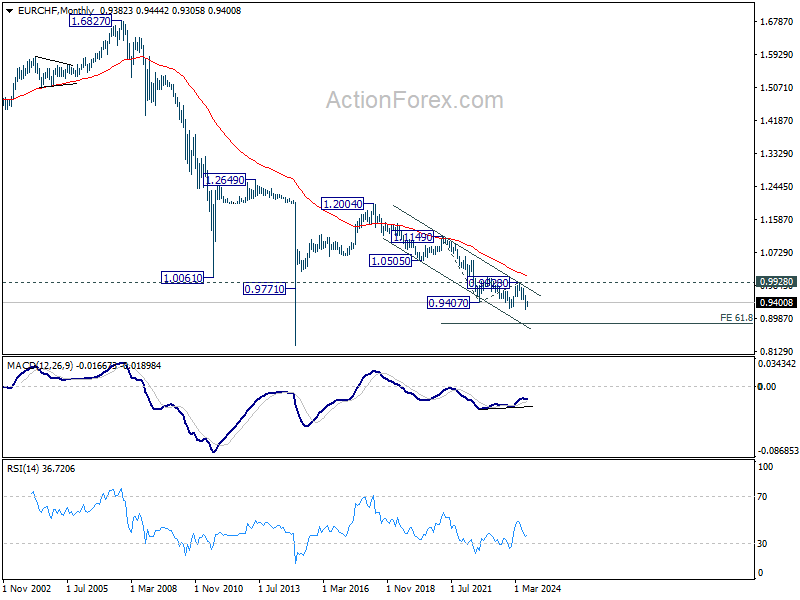

EUR/CHF Weekly Outlook

EUR/CHF edged lower to 0.9305 last week but recovered since then. Initial bias stays neutral this week first, and outlook remains bearish as long as 0.9444 resistance holds. On the downside, below 0.9305 will resume the fall from 0.9579 to retest 0.9209 low. Firm break there will resume larger down trend. However, decisive break of 0.9444 will argue that the fall from 0.9579 has completed as a corrective move. Intraday bias will be turned bias to the upside for 0.9579.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 9/16 – 9/20

Monday, Sep 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | 44.6 | |

| 23:01 | GBP | Rightmove House Price Index M/M Sep | -1.50% | |

| 06:30 | CHF | Producer and Import Prices M/M Aug | 0.10% | 0.00% |

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | -1.70% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 20.3B | 17.5B |

| 12:30 | CAD | Manufacturing Sales M/M Jul | 0.70% | -2.10% |

| 12:30 | USD | Empire State Manufacturing Index Sep | -3.9 | -4.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Aug | |

| Forecast: | Previous: 44.6 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Sep | |

| Forecast: | Previous: -1.50% | ||

| 06:30 | CHF | Producer and Import Prices M/M Aug | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Aug | |

| Forecast: | Previous: -1.70% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | |

| Forecast: 20.3B | Previous: 17.5B | ||

| 12:30 | CAD | Manufacturing Sales M/M Jul | |

| Forecast: 0.70% | Previous: -2.10% | ||

| 12:30 | USD | Empire State Manufacturing Index Sep | |

| Forecast: -3.9 | Previous: -4.7 | ||

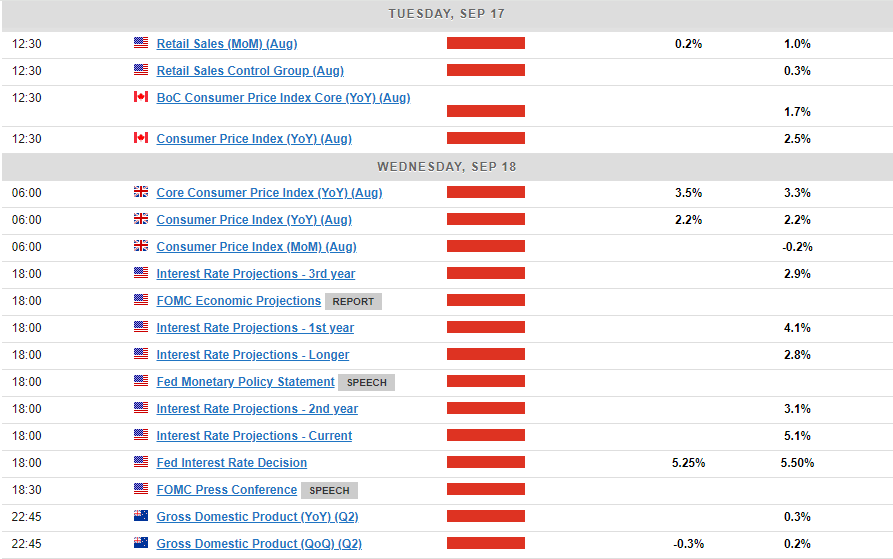

Tuesday, Sep 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 1.00% | -1.30% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 18.6 | 19.2 |

| 09:00 | EUR | Germany ZEW Current Situation Sep | -77.3 | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 17.6 | 17.9 |

| 12:15 | CAD | Housing Starts Y/Y Aug | 246K | 280K |

| 12:30 | CAD | CPI M/M Aug | 0.20% | 0.40% |

| 12:30 | CAD | CPI Y/Y Aug | 2.50% | |

| 12:30 | CAD | CPI Median Y/Y Aug | 2.30% | 2.40% |

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 2.60% | 2.70% |

| 12:30 | CAD | CPI Common Y/Y Aug | 2.30% | 2.20% |

| 12:30 | USD | Retail Sales M/M Aug | -0.10% | 1.00% |

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.20% | 0.40% |

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | -0.60% |

| 13:15 | USD | Capacity Utilization Aug | 77.90% | 77.80% |

| 14:00 | USD | Business Inventories Jul | 0.40% | 0.30% |

| 14:00 | USD | NAHB Housing Market Index Sep | 42 | 39 |

| 22:45 | NZD | Current Account (NZD) Q2 | -3.90B | -4.36B |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.97T | -0.76T |

| 23:50 | JPY | Machinery Orders M/M Jul | 0.80% | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jul | |

| Forecast: 1.00% | Previous: -1.30% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | |

| Forecast: 18.6 | Previous: 19.2 | ||

| 09:00 | EUR | Germany ZEW Current Situation Sep | |

| Forecast: | Previous: -77.3 | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | |

| Forecast: 17.6 | Previous: 17.9 | ||

| 12:15 | CAD | Housing Starts Y/Y Aug | |

| Forecast: 246K | Previous: 280K | ||

| 12:30 | CAD | CPI M/M Aug | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 12:30 | CAD | CPI Y/Y Aug | |

| Forecast: | Previous: 2.50% | ||

| 12:30 | CAD | CPI Median Y/Y Aug | |

| Forecast: 2.30% | Previous: 2.40% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Aug | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 12:30 | CAD | CPI Common Y/Y Aug | |

| Forecast: 2.30% | Previous: 2.20% | ||

| 12:30 | USD | Retail Sales M/M Aug | |

| Forecast: -0.10% | Previous: 1.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Aug | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 13:15 | USD | Industrial Production M/M Aug | |

| Forecast: 0.20% | Previous: -0.60% | ||

| 13:15 | USD | Capacity Utilization Aug | |

| Forecast: 77.90% | Previous: 77.80% | ||

| 14:00 | USD | Business Inventories Jul | |

| Forecast: 0.40% | Previous: 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | |

| Forecast: 42 | Previous: 39 | ||

| 22:45 | NZD | Current Account (NZD) Q2 | |

| Forecast: -3.90B | Previous: -4.36B | ||

| 23:50 | JPY | Trade Balance (JPY) Aug | |

| Forecast: -0.97T | Previous: -0.76T | ||

| 23:50 | JPY | Machinery Orders M/M Jul | |

| Forecast: 0.80% | Previous: 2.10% | ||

Wednesday, Sep 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Aug | -0.04% | |

| 06:00 | GBP | CPI M/M Aug | -0.20% | |

| 06:00 | GBP | CPI Y/Y Aug | 2.20% | 2.20% |

| 06:00 | GBP | Core CPI Y/Y Aug | 3.50% | 3.30% |

| 06:00 | GBP | RPI M/M Aug | 0.10% | |

| 06:00 | GBP | RPI Y/Y Aug | 3.40% | 3.60% |

| 06:00 | GBP | PPI Input M/M Aug | -0.10% | |

| 06:00 | GBP | PPI Input Y/Y Aug | 0.40% | |

| 06:00 | GBP | PPI Output M/M Aug | 0% | |

| 06:00 | GBP | PPI Output Y/Y Aug | 0.80% | |

| 06:00 | GBP | PPI Core Output M/M Aug | 0% | |

| 06:00 | GBP | PPI Core Output Y/Y Aug | 1% | |

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | 2.80% | 2.80% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | 2.20% | 2.20% |

| 12:30 | USD | Housing Starts Aug | 1.32M | 1.24M |

| 12:30 | USD | Building Permits Aug | 1.41M | 1.40M |

| 14:30 | USD | Crude Oil Inventories | 0.8M | |

| 17:30 | CAD | BoC Summary of Deliberations | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.50% |

| 18:30 | USD | FOMC Press Conference | ||

| 22:45 | NZD | GDP Q/Q Q2 | -0.40% | 0.20% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Aug | |

| Forecast: | Previous: -0.04% | ||

| 06:00 | GBP | CPI M/M Aug | |

| Forecast: | Previous: -0.20% | ||

| 06:00 | GBP | CPI Y/Y Aug | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 06:00 | GBP | Core CPI Y/Y Aug | |

| Forecast: 3.50% | Previous: 3.30% | ||

| 06:00 | GBP | RPI M/M Aug | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | RPI Y/Y Aug | |

| Forecast: 3.40% | Previous: 3.60% | ||

| 06:00 | GBP | PPI Input M/M Aug | |

| Forecast: | Previous: -0.10% | ||

| 06:00 | GBP | PPI Input Y/Y Aug | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | PPI Output M/M Aug | |

| Forecast: | Previous: 0% | ||

| 06:00 | GBP | PPI Output Y/Y Aug | |

| Forecast: | Previous: 0.80% | ||

| 06:00 | GBP | PPI Core Output M/M Aug | |

| Forecast: | Previous: 0% | ||

| 06:00 | GBP | PPI Core Output Y/Y Aug | |

| Forecast: | Previous: 1% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 12:30 | USD | Housing Starts Aug | |

| Forecast: 1.32M | Previous: 1.24M | ||

| 12:30 | USD | Building Permits Aug | |

| Forecast: 1.41M | Previous: 1.40M | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 0.8M | ||

| 17:30 | CAD | BoC Summary of Deliberations | |

| Forecast: | Previous: | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 22:45 | NZD | GDP Q/Q Q2 | |

| Forecast: -0.40% | Previous: 0.20% | ||

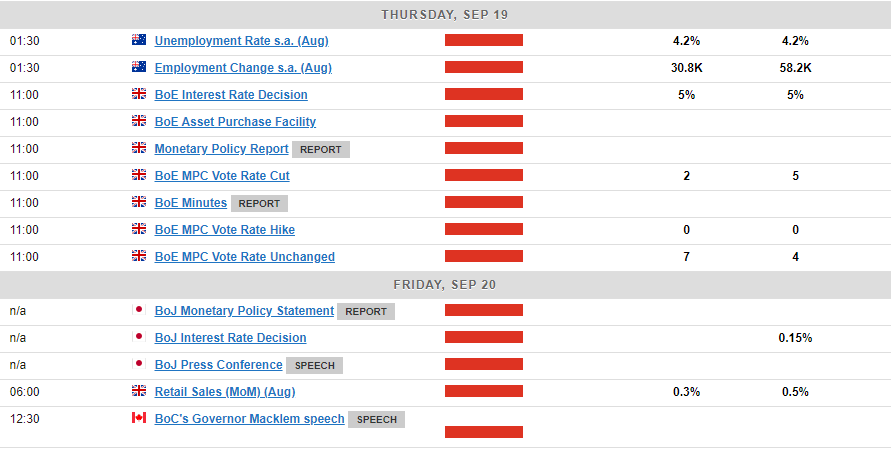

Thursday, Sep 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Employment Change Aug | 25.3K | 58.2K |

| 01:30 | AUD | Unemployment Rate Aug | 4.20% | 4.20% |

| 06:00 | CHF | Trade Balance (CHF) Aug | 5.05B | 4.89B |

| 07:00 | CHF | SECO Economic Forecasts | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 40.3B | 50.5B |

| 11:00 | GBP | BoE Interest Rate Decision | 5.00% | 5.00% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--2--7 | 0--5--4 |

| 12:30 | USD | Initial Jobless Claims (Sep 13) | 232K | 230K |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | 2.4 | -7 |

| 12:30 | USD | Current Account (USD) Q2 | -260B | -238B |

| 14:00 | USD | Existing Home Sales Aug | 3.85M | 3.95M |

| 14:30 | USD | Natural Gas Storage | 40B | |

| 23:01 | GBP | GfK Consumer Confidence Sep | -13 | -13 |

| 23:30 | JPY | CPI Y/Y Aug | 2.80% | |

| 23:30 | JPY | CPI Core Y/Y Aug | 2.80% | 2.70% |

| 23:30 | JPY | CPI Core-Core Y/Y Aug | 1.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Employment Change Aug | |

| Forecast: 25.3K | Previous: 58.2K | ||

| 01:30 | AUD | Unemployment Rate Aug | |

| Forecast: 4.20% | Previous: 4.20% | ||

| 06:00 | CHF | Trade Balance (CHF) Aug | |

| Forecast: 5.05B | Previous: 4.89B | ||

| 07:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | |

| Forecast: 40.3B | Previous: 50.5B | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.00% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--2--7 | Previous: 0--5--4 | ||

| 12:30 | USD | Initial Jobless Claims (Sep 13) | |

| Forecast: 232K | Previous: 230K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | |

| Forecast: 2.4 | Previous: -7 | ||

| 12:30 | USD | Current Account (USD) Q2 | |

| Forecast: -260B | Previous: -238B | ||

| 14:00 | USD | Existing Home Sales Aug | |

| Forecast: 3.85M | Previous: 3.95M | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 40B | ||

| 23:01 | GBP | GfK Consumer Confidence Sep | |

| Forecast: -13 | Previous: -13 | ||

| 23:30 | JPY | CPI Y/Y Aug | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | CPI Core Y/Y Aug | |

| Forecast: 2.80% | Previous: 2.70% | ||

| 23:30 | JPY | CPI Core-Core Y/Y Aug | |

| Forecast: | Previous: 1.90% | ||

Friday, Sep 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.25% | 0.25% | |

| 01:15 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.35% |

| 03:00 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.85% |

| 06:00 | EUR | GermanyPPI M/M Aug | -0.10% | 0.20% |

| 06:00 | EUR | GermanyPPI Y/Y Aug | -0.80% | |

| 06:00 | GBP | Retail Sales M/M Aug | 0.20% | 0.50% |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 12.3B | 2.2B |

| 12:30 | CAD | Retail Sales M/M Jul | 0.30% | -0.30% |

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | -0.40% | 0.30% |

| 12:30 | CAD | Industrial Product Price M/M Aug | 0.00% | |

| 12:30 | CAD | Raw Material Price Index Aug | 0.70% | |

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -13 | -13 |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: 0.25% | Previous: 0.25% | ||

| 01:15 | CNY | 1-Y Loan Prime Rate | |

| Forecast: 3.35% | Previous: 3.35% | ||

| 03:00 | CNY | 5-Y Loan Prime Rate | |

| Forecast: 3.85% | Previous: 3.85% | ||

| 06:00 | EUR | GermanyPPI M/M Aug | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 06:00 | EUR | GermanyPPI Y/Y Aug | |

| Forecast: | Previous: -0.80% | ||

| 06:00 | GBP | Retail Sales M/M Aug | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | |

| Forecast: 12.3B | Previous: 2.2B | ||

| 12:30 | CAD | Retail Sales M/M Jul | |

| Forecast: 0.30% | Previous: -0.30% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jul | |

| Forecast: -0.40% | Previous: 0.30% | ||

| 12:30 | CAD | Industrial Product Price M/M Aug | |

| Forecast: | Previous: 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Aug | |

| Forecast: | Previous: 0.70% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | |

| Forecast: -13 | Previous: -13 | ||

Markets Weekly Outlook – Central Banks to Rule the Roost

- Federal Reserve’s Upcoming Decision: Markets are split on whether the Fed will cut rates by 25 or 50 bps.

- Key data releases from China, Japan, the UK, and the US will shape market sentiment and potentially set the tone for Q4 2024.

- The DXY is nearing a critical support level, and its direction could determine the US Dollar’s trajectory ahead of the US election.

Week in Review: Market Participants Left with More Questions

As the week draws to a close, US data remained robust with a marginal uptick in both the core CPI and PPI prints. Data leading into Thursday’s US session seemed to solidify a 25 bps cut from the Federal Reserve, however the idea of a 50 bps cut gained renewed traction late in the day.

Comments from Former Fed Policymaker Bill Dudley, who explicitly said he would push for a 50 bps cut were he still in the committee. Some media outlets reported that it would be a tight decision between a 25 basis point and a 50 basis point change, which also played a role in the market’s dovish adjustment.

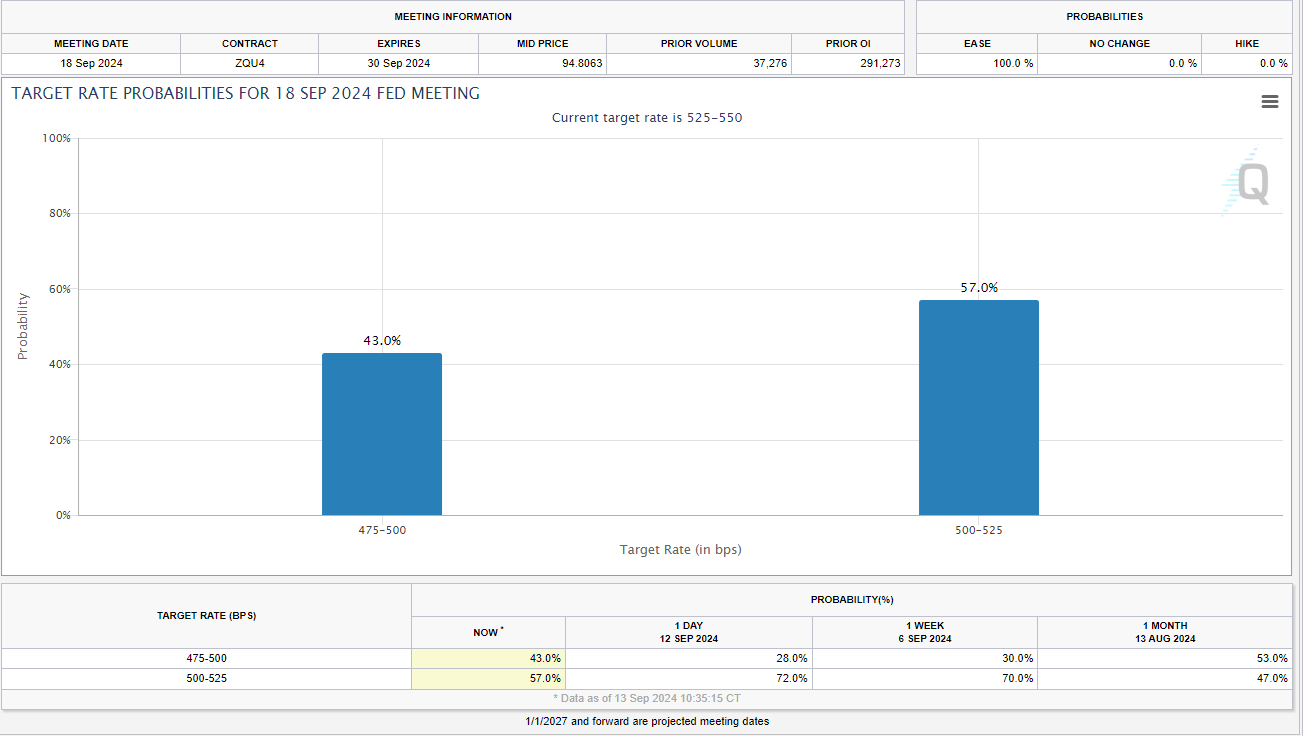

Market expectations saw a significant shift on Thursday with the probability of a 50 bps cut rising from 28% to 43%.

Source: CME FedWatch Tool

The most intriguing part of Dudley’s speech however was his comments about the Fed and surprises. Dudley said “It’s very unusual to go into a meeting with this level of uncertainty – usually the Fed doesn’t like to surprise markets”. Dudley hit the nail on the head as I for one cannot remember the last time I was prepping for a Federal reserve meeting with such uncertainty in play. There is growing chatter and something hinted at by ING Think Research as well in that if markets continue to aggressively price a 50 bps cut ahead of the Wednesday meeting, it could sway the Fed to deliver such a cut.

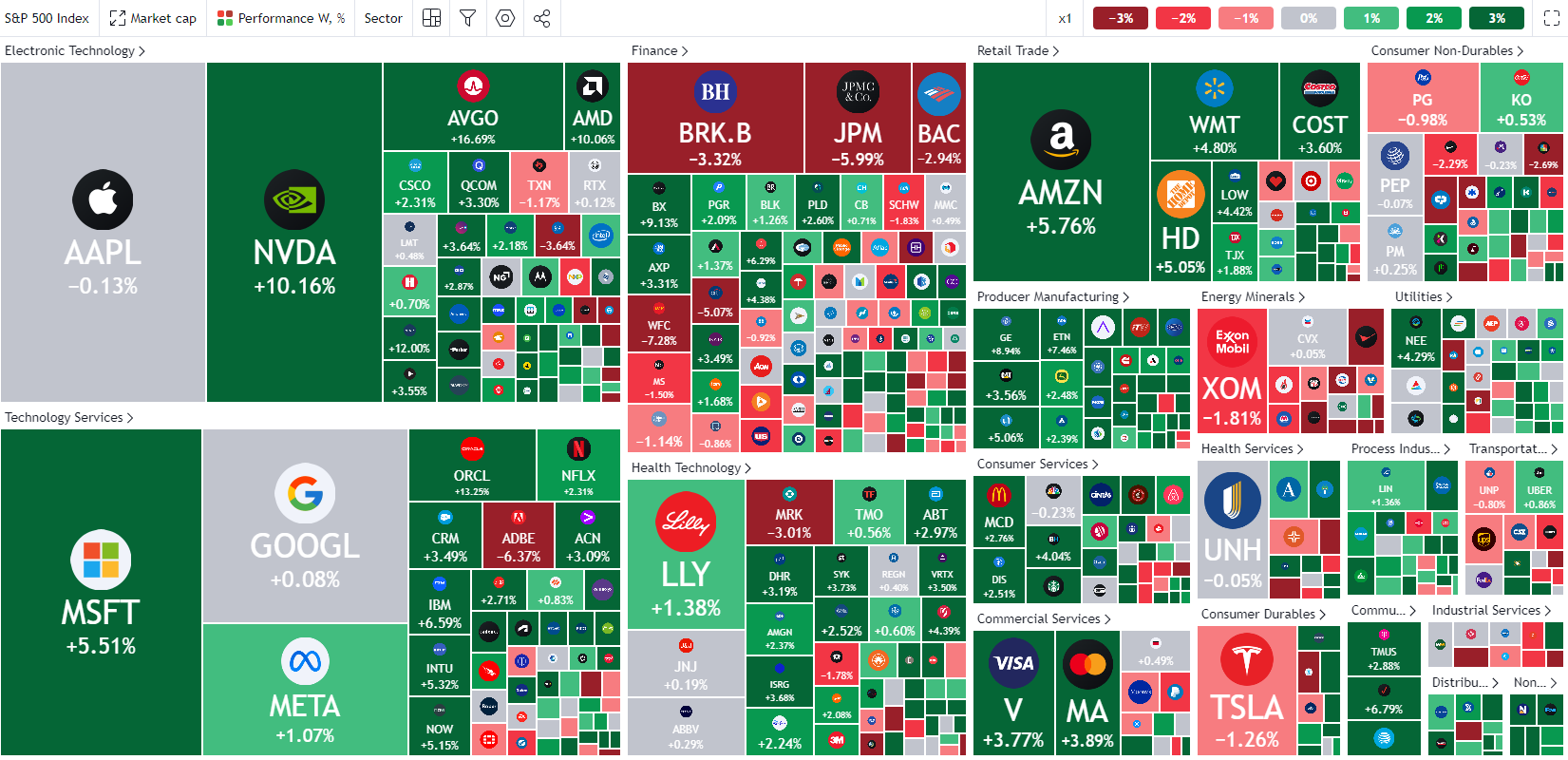

In light of the shift in rate expectations US equities continued their advance this week. The S&P 500 added around $1.8 trillion USD in market cap over the last week alone with NVIDIA up around 15% for the week. This leaves the S&P 500 just 1% away from all time highs, the Nasdaq 100 lags a little behind but is also within striking distance of the all time highs.

S&P 500 Weekly Heatmap

Source: TradingView

Gold received a shot in the arm Thursday afternoon following the rate cut chatter, coupled with rising concerns around the Russia-Ukraine conflict. This helped the precious metal push beyond the highs at 2531/oz before going on to print fresh highs around 2586/oz at the time of writing.

On the FX front we saw a recovery for both cable and EUR/USD with USD/JPY coming under pressure during the course of the week. The DXY remains a key player where FX moves are concerned and is heading into an important week which could set the tone for the US Dollar for the rest of the year.

The Week Ahead: Will it be a 25 or 50 bps Cut from the Fed?

The week ahead is packed with high impact data releases in both developed and emerging markets. Three major central bank meetings and a host of other high impact economic data releases will drive market sentiment and could set the tone for Q4.

Asia Pacific Markets

In Asia, the upcoming week data dumps for China and Japan as well as a raft of Asian central bank meetings make for a busy week ahead.

In China the August data release is set for Saturday morning, and we anticipate another month of tepid growth figures. Key economic indicators, including industrial production (previously 5.1%, now forecasted at 4.8%), fixed asset investment (previously 3.6%, forecasted at 3.5%), and retail sales (previously 2.7%, forecasted at 2.5%), are all projected to slow down.

Market participants will also keep a close eye on the 70-city housing price data, seeking signs of stabilization. Although price declines have slowed over the past two months, the ongoing drop remains notable.

The Bank of Japan is anticipated to maintain its current rates following the 15 basis point increase in July. Nonetheless, if the forthcoming growth and inflation figures align with the central bank’s projections, it is expected to restart its rate hikes in December. This is in line with comments late on Friday from Sanae Takaichi, a candidate for Prime Minister who stated the time is not right for another rate hike.

Europe + UK + US

A busy week in developed markets with both the BoE and Federal Reserve rate decisions taking center stage. There are a host of other data releases as well which are likely to be overshadowed by the Central Bank meetings.

The Bank of England faces a different challenge to the Federal Reserve as UK data has remained strong. Recessionary fears have faded and market participants have tempered their rate cut bets following the latest batch of data. Part of the caution stems from services inflation, which, at 5.2%, remains higher than that of the US and the eurozone, similar to the trend in wage growth. However, this figure is notably lower than the Bank’s latest forecast, and July’s numbers also fell short of expectations. For now it appears a hold may be the most appropriate course of action before a cuts closer toward the year end.

The Federal Reserve meeting has already been covered in depth above. The challenges for the Fed are clear as markets grapple with either a 25 or 50 bps cut next week. I am leaning toward a 25 bps cut but as I said earlier there are a host of uncertainties. If markets continue to price in a 50 bps cut ahead of Wednesday, will the Fed spring a surprise?

Chart of the Week

This week’s focus is on the US Dollar Index (DXY), which continues to be intriguing and surprising. The week ahead could be make or break for the DXY as it still remains within striking distance of the psychological 100.00 level.

The DXY put in an impressive start to the week before the momentum began to wane. Tuesday and Wednesday saw some sideways price action before a selloff on Thursday as rate cut bets changed.

The index is currently trading just below the support level at the 101.18 handle with 100.50 needing to be cleared if we are to finally test the 100.00 mark.

On the upside now we have created a key area of resistance that needs to be cleared at around the 101.77 if a recovery is to gain any traction.

US Dollar Index (DXY) Daily Chart – September 13, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 100.50

- 100.00

- 99.55 (July 2023 Low)

Resistance:

- 101.80

- 102.16

- 103.00

- 103.80 (100 and 200-day MA)

The Weekly Bottom Line: Here Comes the Cut

U.S. Highlights

- Markets have been weighing the prospect that the Federal Reserve will opt for a 0.5 percentage point cut in the federal funds rate next week.

- Core consumer price index inflation surprised to the upside, lifted by a strong print from owners’ equivalent rent.

- The breadth of inflation continues to gradually narrow, but a still resilient economy supports the case for a standard 0.25 point cut at next week’s Fed meeting.

Canadian Highlights

- Canadian household net worth rose further in the second quarter of 2024, with gains in U.S. equities and deposits offsetting declines in real estate and Canadian equities.

- Consumer spending remains muted. TD Spend data shows spending on services slowing down, now tracking closer to goods spending, as debt servicing costs continue to weigh on household budgets.

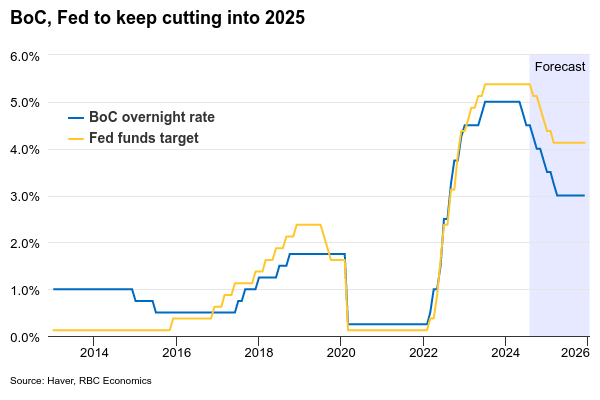

- The Bank of Canada is expected to continue its rate-cutting cycle, bringing the policy rate down to 3.75% by year-end. Stay tuned for our updated economic forecast that will be released next Tuesday.

U.S. – Here Comes the Cut

After Vice President Harris and former President Trump took their turn in the spotlight on Tuesday night, focus turned back to inflation and where the Federal Reserve is likely to take interest rates from here. Markets were weighing the possibility that the deteriorating economic backdrop was opening the door to a 50 basis-point cut in the Fed Funds rate next week. Alas, inflation didn’t seem to want to cooperate, as Consumer Price Index (CPI) inflation clocked in at 2.5%, as expected, with the core measure surprising to the upside amid an upturn in shelter prices. Current market pricing puts the odds of a 50 basis-point cut at basically a coin toss, but we think the state of the economy and the details of the report argue for a smaller 25 basis-point move next week.

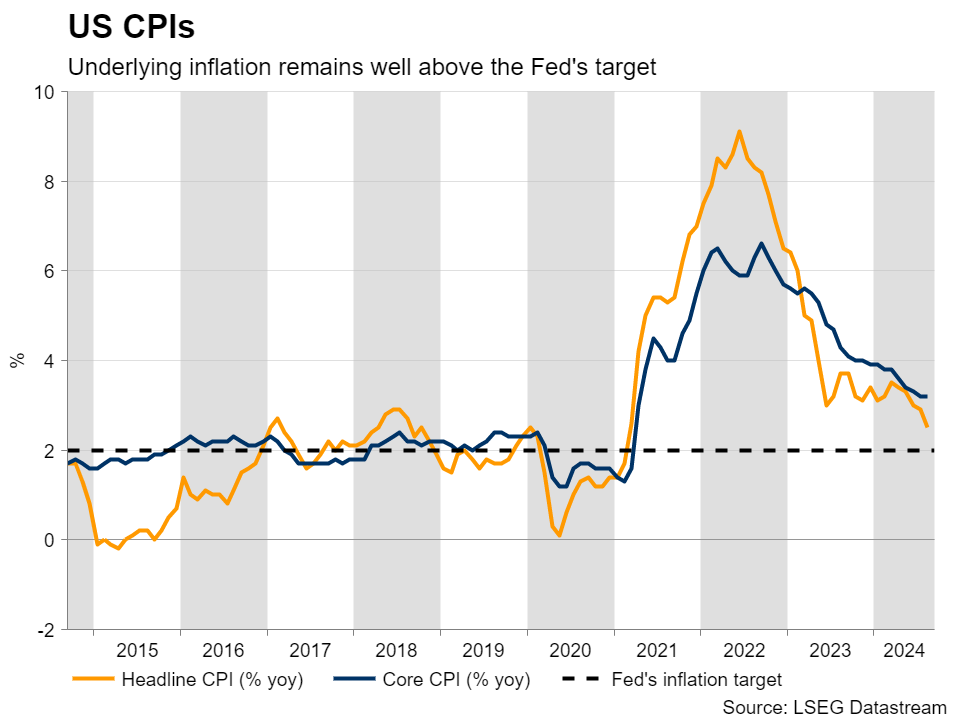

First, and foremost, this week’s report is a minor setback and not a return to the widespread inflation we saw in 2022. Most of the gain was powered by a strong showing in shelter costs, specifically owners’ equivalent rent (Chart 1). Growth here ticked up for the month, but this has been a steady contributor to inflation this cycle. While the rate could moderate slightly heading into the fall, it was the strongest print in seven months. Now, importantly, the Fed’s preferred measure looks at core personal consumption expenditure (PCE) inflation, where shelter prices carry a smaller weight. So, this upturn will have a comparably smaller impact on the Fed’s preferred inflation measure.

As for the two other major inflationary culprits, airfares and vehicle insurance, there is reason to expect moderation. New and used vehicle prices have cooled substantially, and after rising car valuations drove insurance rates higher, this impulse should continue to fade. On airfares, last month broke a string of negative prints for the category – an element of giveback that could easily fade.

All of which is to say, consumer price inflation is gradually becoming confined to fewer categories (Chart 2). Taking a lens to the three-month percent change of the CPI categories, the share of categories with prices still rising above a three percent (annualized) rate has been below the pre-pandemic average for the past three months. After the uptick in inflation last spring, the return to a downward trajectory is welcome. This trend will need to continue for few more months still before the year-on-year prints start to show the same normalization, but things are pointing in the right direction.

The data suggest that the Fed’s policy rate does not need to be as restrictive as it is, but while former NY Fed President Dudley this week suggested there was “a strong case” for a 50 basis- point cut, we think this is a tad premature. Between this week’s CPI report showing unexpected strength in core consumer prices, the upside surprise in the producer price index, and a labor market that continues to steadily add jobs, there is enough strength to suggest aggressively easing monetary policy is not yet warranted. Our view remains that a 25 basis-point cut next week is the most likely outcome, with two more cuts coming by year-end.

Canada – Spending Restraint Despite Wealth Gains

In the absence of major Canadian economic releases this week, the rates market’s head was turned towards our southern neighbour. Financial markets are leaning slightly towards a standard 0.25 percentage point cut at the Federal Reserve rate decision next Wednesday, but on Friday morning raised the odds of a larger 0.5 point cut to nearly a coin flip. Bond yields continued to trend downward as investors sought to lock in rates. Canada’s 10-year government bond yield fell 10 basis points. Meanwhile, the S&P/TSX index hovered near record highs, buoyed by strength in the resource sector, as gold prices advanced and oil rebounded. The index ended the week 3.7% higher, with a quarter-to-date gain of 8.0%.

Sparse though it was, the week brought forward several second-tier data releases. The national balance sheet and financial flow accounts for the second quarter of this year showed that Canadian household net worth grew by $42.4 billion. That was a relatively modest 0.3% quarter-on-quarter increase, but it built on top of a healthy 3.6% gain in the first quarter. Gains in U.S. equities and deposits more than offset declines in real estate and Canadian equities.

Household wealth growth is expected to accelerate by the end of the current quarter, barring any major disruptions in equity markets, which are tracking in the black on both sides of the border. House prices are also rising, and are expected to finish this quarter strong. Although some regional housing markets, particularly the Greater Toronto Area condo market, face headwinds due to supply-demand imbalances and still-high mortgage rates.

Despite wealth gains, the wealth effect on consumer spending remains muted, as most wealth is concentrated in the top 20% of households who typically have lower propensity to consume. Furthermore, adjusted for inflation and population growth, per capita household wealth has fallen nearly 15% from its 2021 peak. Since then, real per capita spending has contracted in seven of the last 11 quarters, underscoring that on aggregate, economic growth has been largely population-driven rather than productivity led.

Our internal data shows that while consumer spending on services is still chugging along, the pace is noticeably slowing (Chart 2). Services, which had been outpacing goods since 2021, are now tracking much closer to goods spending. Canadians may still have a nest egg—whether in real estate or investments—but they are hesitant to spend freely. With debt servicing costs still taking up 15 cents of every disposable income dollar, it’s no surprise that consumer enthusiasm is tempered.

With services inflation excluding shelter still elevated, a continued slowdown in services spending helps reduce the risk of renewed upward pressure on services prices. This provides peace of mind for the Bank of Canada in sticking with its course. We expect the Bank continue cutting its police rate in October, with another reduction in December, bringing the rate down to 3.75% by year-end. Stay tuned for our updated economic forecast that will be released next Tuesday.

Weekly Economic & Financial Commentary: Let the Easing Begin

Summary

United States: Firmer Inflation Tilts the Scales Toward 25

- The core Consumer Price Index rose 0.3% in August, the fastest increase in four months. Soft measures like NFIB price plans continue to signal a downward trend in inflation; however, recent price resiliency may prompt FOMC members to exercise a bit more caution in September.

- Next week: Retail Sales (Tue.), Industrial Production (Tue.), Existing Home Sales (Thu.)

International: European Central Bank Continues Carefully Along Its Rate Cut Path

- The European Central Bank (ECB) cut its Deposit Rate by 25 bps this week to 3.50%, as widely expected. Considering somewhat balanced commentary on economic developments in the policy statement, upwardly revised core inflation forecasts for this year and next, and some hawkish-leaning comments from ECB President Christine Lagarde in the post-meeting press conference, we remain comfortable with our view for the ECB to take a cautious approach to rate cuts.

- Next week: China Retail Sales, Industrial Production (Sat.), Bank of England (Thu.), Bank of Japan (Fri.)

Interest Rate Watch: Let the Easing Begin

- The FOMC is widely expected to kick off the long-awaited easing cycle at its meeting next week. Looking ahead to the September 17-18 meeting, we see three key developments.

Credit Market Insights: Uptick in Consumer Borrowing in July

- Total consumer credit increased $25.45B in July, the most since November 2022. The increase in consumer borrowing over the month shows that the consumer continues to rely on credit to maintain their levels of spending. That said, the trend in borrowing has continued to downshift this year, suggesting that consumers may be feeling the pinch of higher rates.

Topic of the Week: A (Labor) Force to Be Reckoned With

- In celebration of Hispanic Heritage Month, which kicks off this Sunday, we dive into the significant contributions that the Hispanic and Latino community has made to U.S. labor force growth over the past decade.

The U.S. Fed Will Finally Start Cutting Interest Rates

Wednesday will mark a much anticipated first interest rate cut from the U.S. Federal Reserve. Gradual but persistent labour market softening and slowing inflation make it clear that current high interest rates are no longer needed.

Indeed, the U.S. unemployment rate ticked lower in August but that was after having trended persistently higher over the last year, driven by a combination of slower hiring demand (as employment growth decelerates) and rising labour supply (as immigration boosts the size of the labour force). This makes it less likely that growth in consumer prices, which are more pronounced among service components, will pick up even with domestic consumer spending broadly holding up.

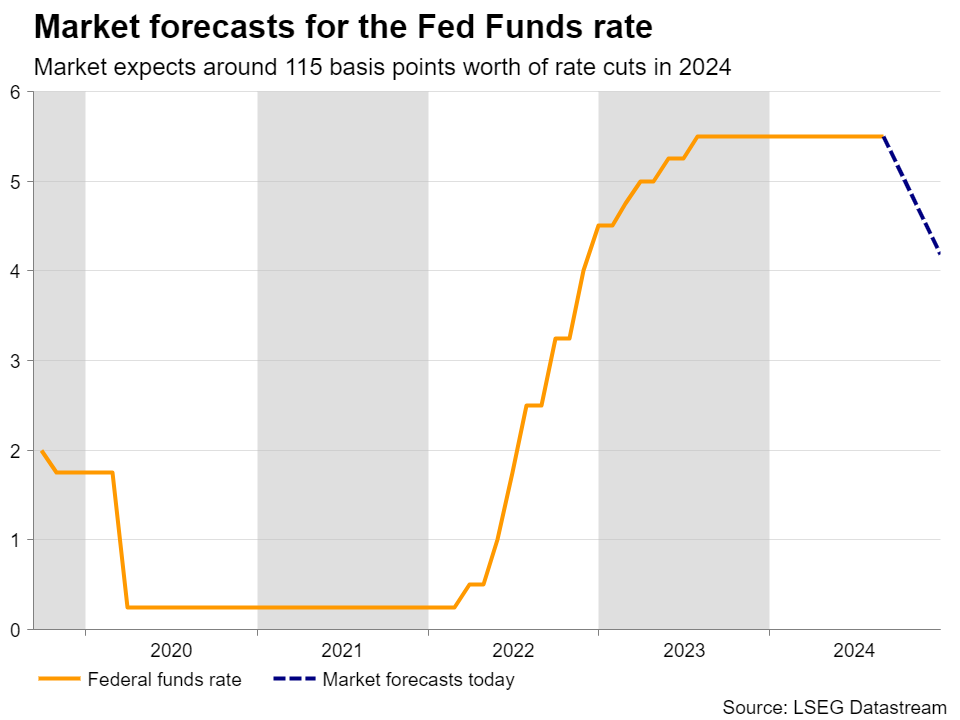

Expectations that inflation will remain lower should keep the Fed on a steady easing path. We expect the Fed’s Summary of Economic Projections will show a median of 75 basis points worth of cuts this year, up from the 25 bps that was expected in July and in line with our forecast. Outside of that, we think Governor Powell’s comments will likely stay on the cautious side—hinting at future rate cuts without committing to a pre-determined path to allow for more flexibility in future decisions.

In Canada, inflation trends have also been slowing. Tuesday’s consumer price index report for August is expected to continue that trend. We expect headline price growth will tick down to 2.1% year-over-year from 2.5% in July, and just a hair over the BoC’s 2% inflation target. Most of that August slowing is expected from a pullback in gasoline prices, but the BoC’s preferred core CPI measures are also expected to trend lower, with the closely-watched three-month annualized growth rate easing from an average of 2.6% in July.

Moving forward and as highlighted in our monthly update , growth in the U.S. is not expected to slow but not falter given unusually large amounts of fiscal spending that is expected to extend into the years ahead, while underperformance in the Canadian economy is expected to persist. We expect a 25 bps cut at every meeting for both the BoC and the Fed, but the BoC will reach a relatively lower terminal of 3% compared to a 4 to 4.25% range for the fed funds rate by Q2 next year. Risks are for a more aggressive easing path – something that central bankers have been clear that they are willing to conduct should the economic growth backdrop deteriorate more quickly than is currently expected.

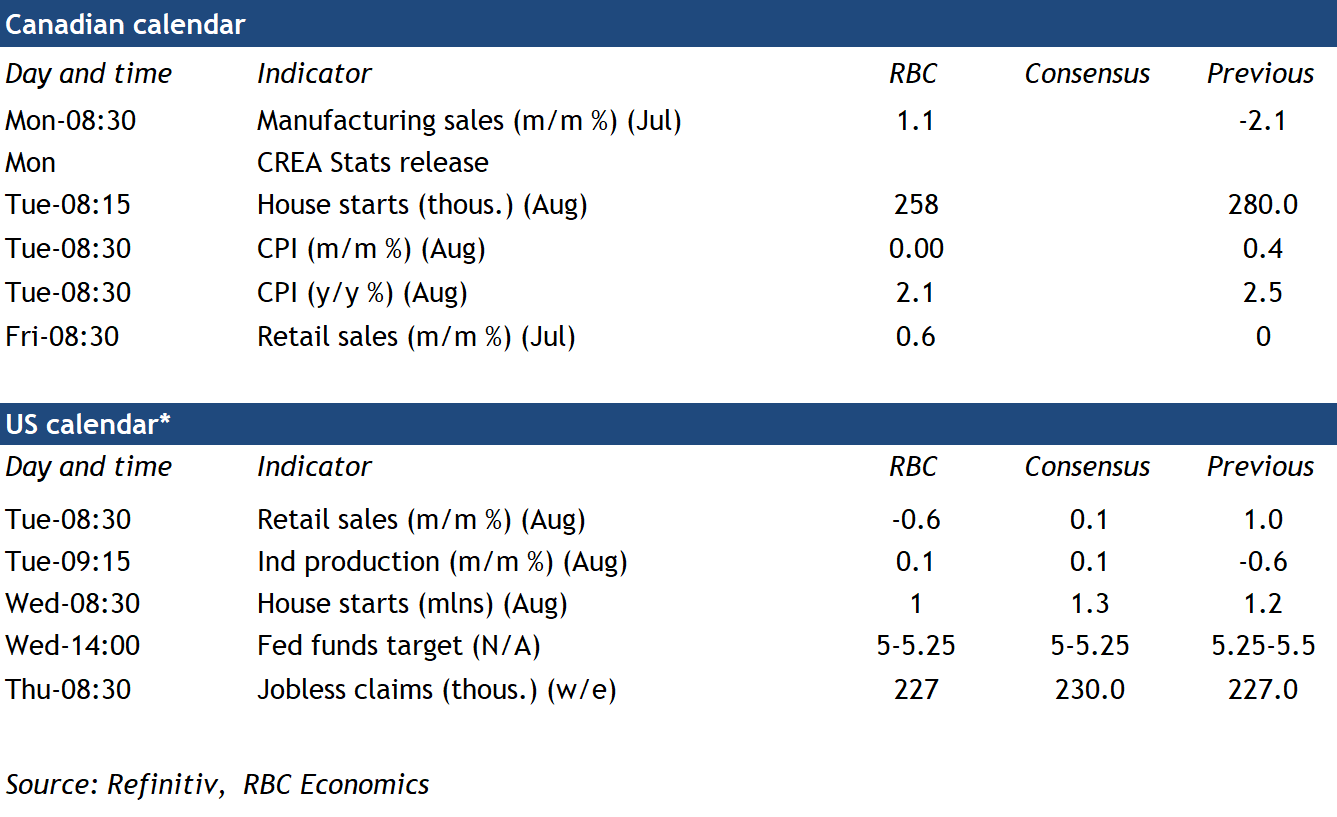

Week ahead data watch

We expect manufacturing sales increased by 1.1% in July, consistent with StatCan’s flash estimate. Much of that was led by higher sales in petroleum and coal, as well as chemical subsectors.

Statistics Canada’s advance estimate of Canadian retail sales was up 0.6% in July after two consecutive declines. Auto sales dipped 0.2% in Augus, by our count, and a drop in gasoline prices likely lowered sales at gas station.

The Canadian Real Estate Association (CREA) will publish the August resale housing statistics on next Monday. Early reports from regional housing boards have not flagged a sharp resurgence in home resales in the wake of initial Bank of Canada interest rate cuts. More interest rate cuts are likely to stimulate homebuyer demand across the country. but we expect this will be gradual.

U.S. retail sales likely edged lower by 0.6% in August, given both gas prices and auto sales were down during that month. Industrial production likely edged up 0.1%, following the 0.6% reduction in the prior month, the growth was mainly led by higher output in mining and utility sectors.

Week Ahead – Fed to Cut Interest Rates, BoE and BoJ to Remain on Hold

- Investors are split between a 25 and 50bps Fed rate cut

- BoE expected to stand pat, but resume cuts in November

- BoJ to also stay on hold, focus to fall on future hike signals

Let the Fed cuts begin

Since the July US employment report, which sparked fears of recession, investors have been trying to figure out the size of the potential rate cut the Fed will deliver at its September gathering, and the moment of truth has finally come.

On Wednesday, the Fed announces its decision, and it seems that it is not a matter of whether officials will press the rate cut button, but how strongly. In other words, by how many basis points will they lower the Fed funds target rate.

Following Chair Powell’s speech at Jackson Hole, where he noted that they will not tolerate further weakness in the labor market, investors locked their gaze on employment-related data, adding to their rate cut bets on any sign of softness. Even the NFP report for August was not as encouraging as expected, with investors seeing then a 30% chance of a 50bps rate cut at next week’s gathering.

That percentage came down to around 15% after the CPI data for August revealed that underlying inflation remained elevated well above the Fed’s objective of 2%, but it climbed back to 45% after media reports from the Financial Times and the Wall Street Journal said that next week’s decision would be a close call.

Having said all that though, with the Atlanta Fed GDPNow model projecting a solid 2.5% growth rate for Q3, it seems that there is no concrete reason for policymakers to start this easing cycle with an aggressive move. A 25bps cut seems the more sensible move.

If this is the case, the dollar could gain as those expecting a bigger one may get disappointed, but whether it could hold onto its gains may depend on the updated dot plot and Powell’s remarks about the Committee’s future course of action.

If the dot plot and Powell suggest fewer basis points worth of reductions this year than the 115 currently expected by the market, the dollar’s engines may receive more fuel. As for Wall Street, confidence that the world’s largest economy is not headed for a recession may keep risk appetite elevated, even if this means fewer-than-expected rate cuts.

US retail sales are due out on Tuesday, but given the importance of the Fed meeting, they are unlikely to hugely impact investors’ positioning.

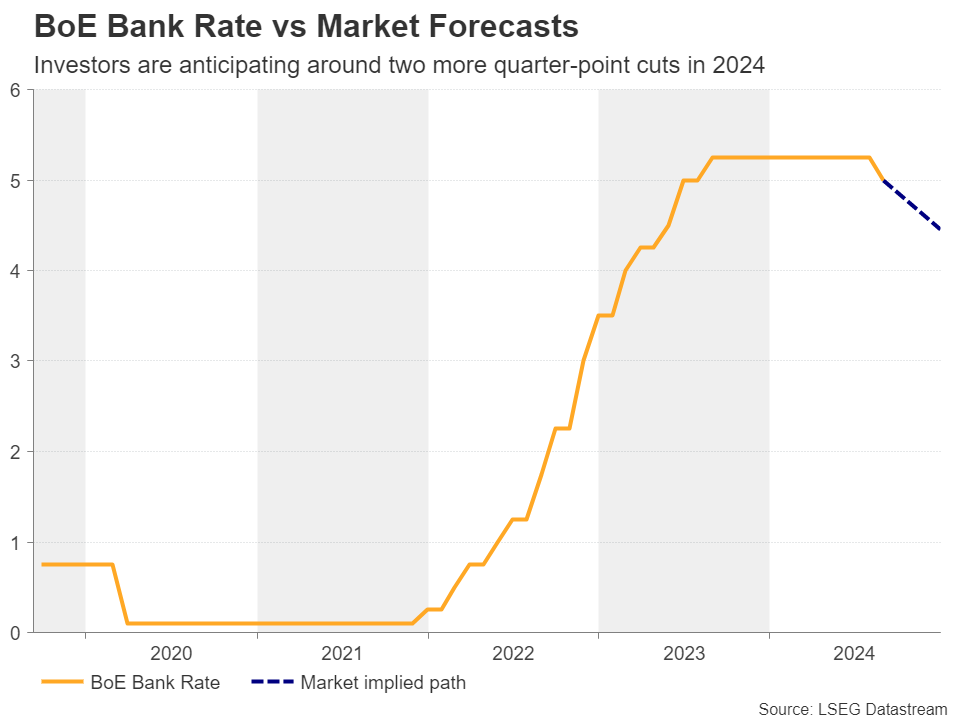

Will the BoE confirm November cut bets?

On Thursday, the central bank torch will be passed to the BoE. At its latest decision, this Bank cut interest rates by 25bps, but the decision was a close call, with officials signaling that they will be careful about future reductions.

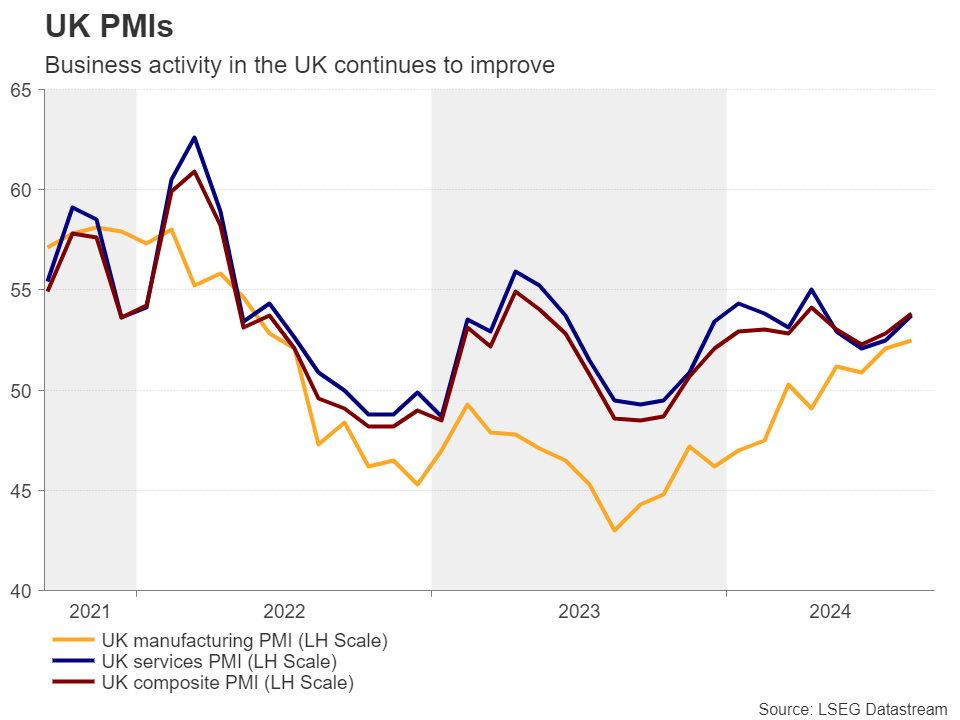

Since then, data has been mostly corroborating the officials’ stance. The PMIs beat expectations in both July and August, while the labor market continued to improve. Although average weekly earnings continued to slow, they’ve been proving stickier than expected, with the y/y rate for July resting at an elevated 5.1%. What’s more, the headline CPI rebounded somewhat in July, with services inflation remaining stubbornly high. The August inflation numbers are coming out on Wednesday, while on Friday, retail sales are scheduled to be released.

Even BoE Governor Bailey himself said at Jackson Hole that they are not in a rush to cut again, prompting market participants to factor in a strong 80% chance for no action at this meeting. The remaining 20% favoring a rate cut may be the result of some concerns after the monthly GDP for July pointed to stagnation.

Should officials indeed keep their hands off the rate cut button, investors will turn their attention to the Bank’s communication about their future plans. According to the UK Overnight Index Swaps (OIS), investors expect another two quarter-point reductions at the November and December gatherings. Thus, if policymakers maintain a no-rush mindset, the pound may extend its latest rebound.

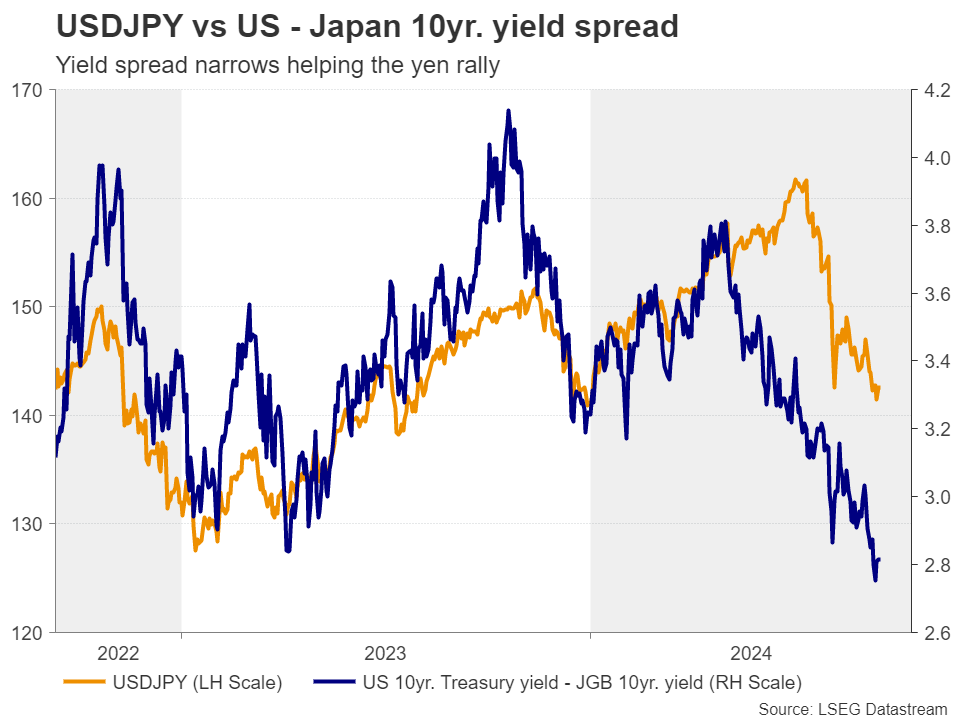

Strong yen awaits BoJ decision

On Friday, it will be the turn of the BoJ. In July, Japanese policymakers raised interest rates by 15bps and have been since signaling that more hikes are looming. This allowed investors to pencil in an 85% chance for another 10bps worth of increase by the end of the year.

Although BoJ officials have been repeatedly noting that the pace of rate hikes will be slow, the divergence in monetary policy strategies between this Bank and the rest of the world has led to a surging yen as traders decided to abandon a previously overcrowded carry trade.

Yet, no policy action is expected at this gathering and thus, the focus will be on whether Ueda and his colleagues will continue to signal more hikes down the road. Anything corroborating the market’s view that another increase could be delivered before year-end, may allow the yen to continue marching north.

A few hours ahead of the decision, the Nationwide CPI numbers for August will be published.

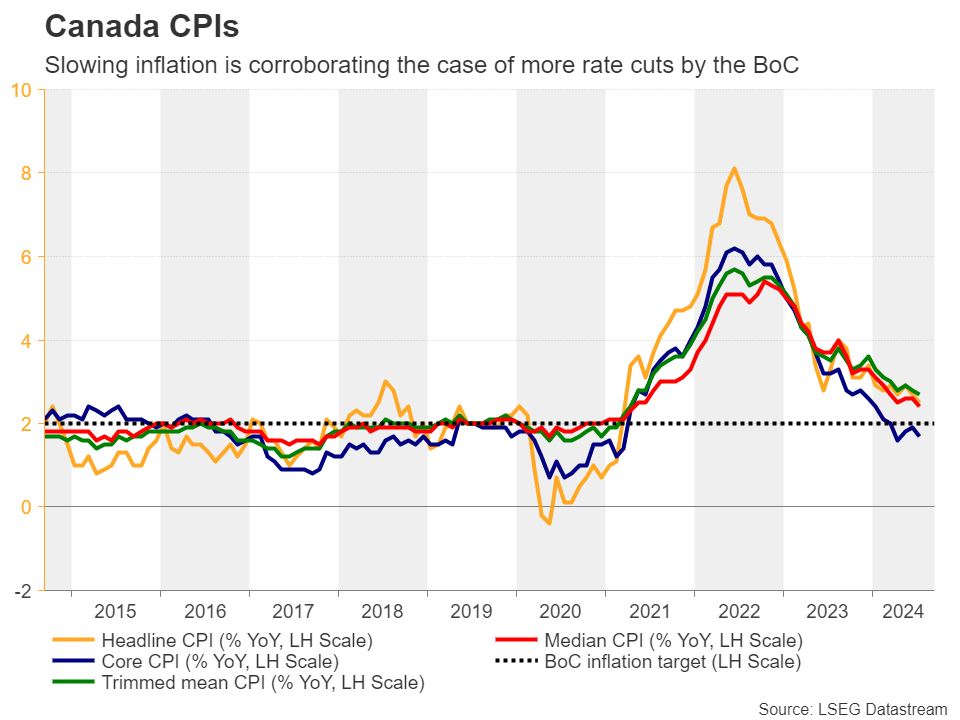

Canadian inflation and BoC Summary of Deliberations

Canada is also releasing its CPI inflation data for August on Tuesday. At last week’s meeting, the BoC cut interest rates for a third time in a row, opening the door to bigger cuts if the economy slows more sharply ahead. On Wednesday, the Bank’s Summary of Deliberations may provide more clarity on that front, but further cooling in consumer prices the day before could very well encourage market participants to add to their rate cut bets. Currently, they are expecting another 60bps worth of cuts by the end of the year. The nation’s retail sales are on Friday’s agenda.

In Australia, the employment report for August is due out on Thursday.

Weekly Focus – Enter Fed Cutting Cycle

Markets started off the week lingering at the fear of recession after the August US jobs report failed to shake off those fears. Chinese core inflation dropping further to 0.3% as a symptom of weak Chinese demand only added further to the sour risk sentiment. We saw it in FX markets, with further slides in Swedish and Norwegian kroner, the latter also weighed down by cheaper oil. Sentiment turned around a bit on Thursday, though, with equities higher and a rebound in industrial metals and oil prices.

The ECB cut rates by 25bp as widely expected. President Lagarde provided no guidance on the timing of the next policy move yet given that she did not see the need to impact the market pricing, we believe that the ECB is overall content with the current market pricing of 25bp/quarter through the end of next year, as domestic inflation pressure remains elevated due to high wage growth. Lagarde also highlighted the further confidence of the 2% inflation target being met in the medium-term, while the accompanying staff projections only saw cosmetic changes. On the data front, July industrial production data from the euro area confirmed what PMIs have already shown, namely that the manufacturing sector will weigh on Q3 GDP growth.

In the US, Kamala Harris came out of the presidential debate on top and markets reacted by sending the USD and yields slightly lower, suggesting that expectations of Trump pursuing more expansionary fiscal policies and protectionist measures remain intact. This is probably also a good gauge for how markets may react to election news going forward.

With a big question mark still hanging over the US labour market, inflation data once again took markets' focus this week on the hopes of getting some clarity on the next Fed move. 0.3% m/m core inflation was a bit more than expected, mostly driven by shelter prices. On the one hand, it is a comforting sign that businesses still see room to hike prices, and a low inflation print would have added to recession concerns. On the other hand, it forces the Fed to keep an eye on the inflation mandate and probably deprives them from the opportunity to cut rates by more than 25bp next week. Ahead of the FOMC meeting, August retail sales are released but we think the bar for changing the rate outlook is high. We see a 25bp cut as the clear base case.

We also have several other central bank meetings on the schedule next week. We expect rates unchanged at all of them. The Bank of England meeting on Thursday will be focused on the inflation data, which is released the day ahead. On Friday, inflation data released during the Bank of Japan's two-day policy meeting will probably show price pressures picking up. Even so, the bond market rally since the late July meeting and cheaper oil prices has been a boon to the yen, which makes the initial motive for hiking rates less acute. We expect the next BoJ hike in December. We will also zoom in on the final euro area inflation data, which will allow us to gauge domestic inflation. It has remained high and is a key reason we expect only a gradual cutting approach from the ECB.