Sample Category Title

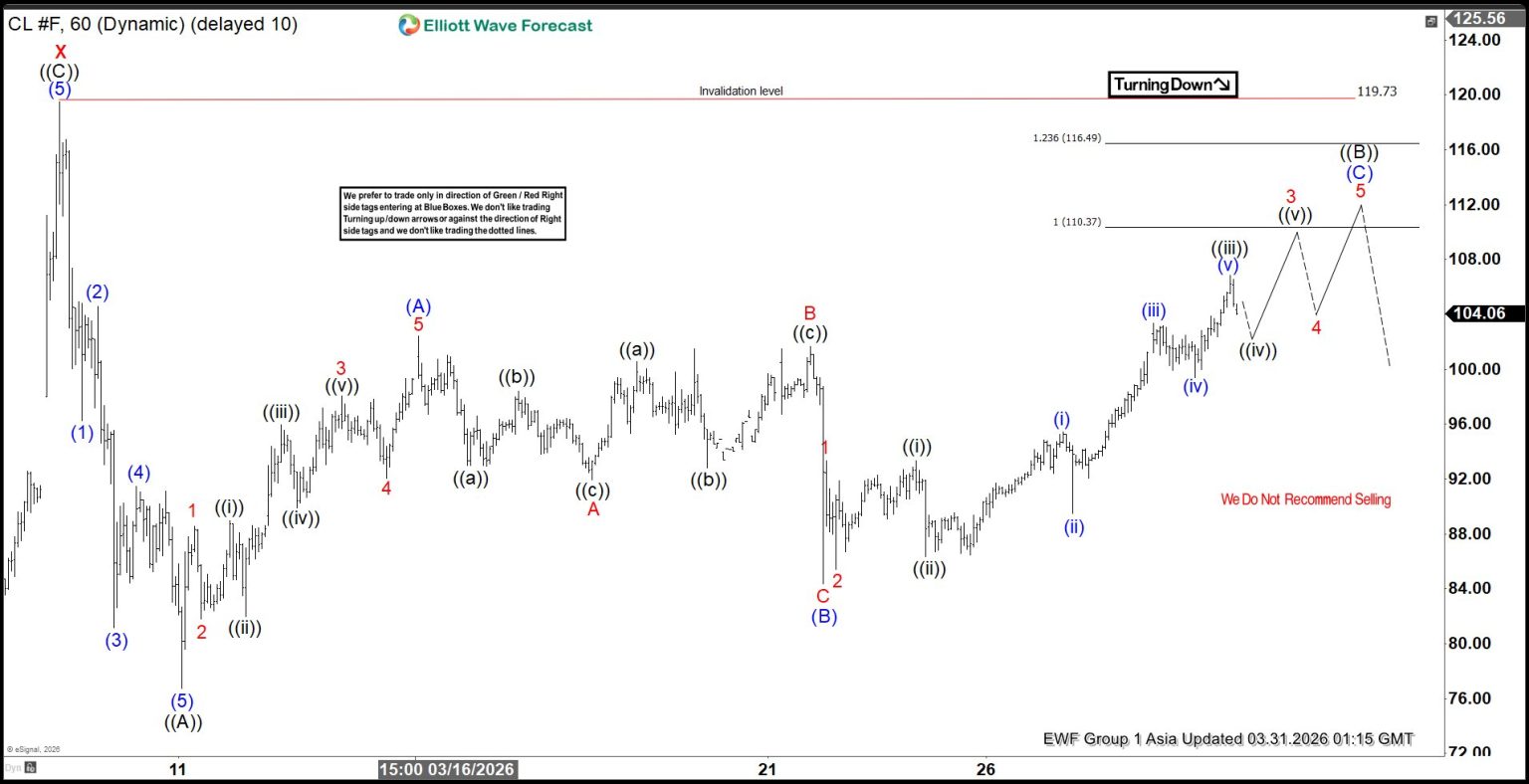

Elliott Wave Outlook: Oil (CL) Zigzag Rally Targets $110 Area

After surging to $119.7 on March 9, crude oil experienced a sharp decline, reaching $76.73 by March 11. This retreat unfolded in the form of a five-wave impulsive Elliott Wave structure, marking a decisive corrective phase. From the March 9 peak, wave (1) concluded at $96.25, followed by a rebound in wave (2) that terminated at $104.57. The subsequent decline in wave (3) reached $81.19, while wave (4) produced a modest recovery to $91.48. The final leg, wave (5), extended lower to $76.73, thereby completing wave ((A)) at a higher degree.

Currently, a corrective rally in wave ((B)) is underway, developing internally as a zigzag formation. From the termination of wave ((A)), the initial advance in wave (A) ended at $102.44. A subsequent pullback in wave (B) found support at $84.37. The ongoing rise in wave (C) carries potential to extend further, targeting the 100% to 123.6% Fibonacci extension of wave (A). This critical zone lies between $110.3 and $116.5, where renewed selling pressure may emerge. Should sellers reassert control in this region, oil prices could resume their decline in wave ((C)), provided the pivot at the $119.7 high remains intact.

Oil (CL) 60-Minute Elliott Wave Chart

CL Elliott Wave Video

https://www.youtube.com/watch?v=gjcZlPwIGvc

Spotlight on Euro Area March Inflation Figures

In focus today

In the euro area, we receive the flash March inflation print. We expect HICP inflation will rise to 2.6% y/y (from 1.9%) while core inflation should fall slightly to 2.3% y/y (from 2.4%). The headline rise is driven by energy inflation, adding an estimated 0.9 p.p., with petrol prices up 15% m/m and diesel 28% m/m. Core inflation is expected to decline as the spike in Italian services inflation from the Winter Olympics reverses. The data is a key input for the ECB's April meeting, but we note that it only captures part of the first-round effects of the war and no second-round effects. Hence, the April inflation print on April 30 will likely be more important for the ECB's decision.

EU energy ministers will hold an informal video conference to coordinate their response to oil and gas market disruptions from the Iran war, amid heightened market uncertainty and national measures like Poland's petrol price cap and Spain's EUR5bn energy package.

In the central bank space, we have a string of ECB speeches as well as Federal Reserve speeches. There are four from ECB officials and three from Federal Reserve Officials. The market will as always be looking for comments on inflation, but also the negative impact on growth from the rise in oil prices.

In the US, the February JOLTS job openings report is due, offering the first labour market figure of the week. The stronger-than-expected January report reflected improved labour demand and fewer layoffs, supported by positive signals from online job postings.

In Sweden, Riksbank speeches are scheduled from Erik Thedéen at 8.00am and Per Jansson at 12.00pm, with the latter hosted by Danske Bank. Thedéen and Seim leaned hawkish at the last meeting, while Jansson, Hjelm, and Bunge remained dovish. Although it may be early for clear signals on the May meeting, with markets pricing a 50% chance of a May hike, we look forward to insights on their reaction function to supply shocks.

Overnight, China releases the private PMI manufacturing report from Rating Dog. Unlike the official NBS PMI, February's Rating Dog PMI was strong at 52.1. The Yicai high-frequency indicator suggests further strength in March, though the Iran war adds uncertainty.

In Japan, the Q1 Tankan business survey, due overnight, will provide key insights for the Bank of Japan ahead of its policy meeting. Rising energy prices and a weaker yen threaten to erode consumers' purchasing power, jeopardising a recovery.

Economic and market news

What happened overnight

In Japan, Tokyo's March core CPI rose to 1.7% y/y, below expected, as fuel subsidies offset rising costs. An index excl. fresh food and fuel rose 2.3% after a 2.5% gain in February. Analysts expect inflation to pick up due to surging oil prices and a weak yen, with markets pricing a 70% chance of an April rate hike. BOJ Governor Ueda hinted at potential action. Separate February data, including a 2.1% m/m drop in factory output and a 0.2% y/y decline in retail sales, offers largely outdated insights

In China, the official March manufacturing PMI rose to 50.4, the highest in a year, up from February's 49.0, signalling improved demand. Non-manufacturing PMI also increased to 50.1. While the stronger reading eases pressure on policymakers, analysts warn that surging energy prices from the Middle East war and global supply chain disruptions pose risks to sustained growth.

What happened yesterday

In the Middle East, Iran's parliamentary Security Commission has approved a plan to impose tolls on ships passing through the critical Strait of Hormuz (SOH). The plan includes measures to enhance security, regulate maritime navigation, and charge rial-denominated tolls, with a prohibition on vessels from the US and Israel. This development adds to tensions in the ongoing conflict, which has already disrupted oil shipments and intensified global market volatility. Amid these rising tensions, President Trump warned that the US would obliterate Iran's energy plants and oil wells if the SOH is not reopened to international shipping.

In the US, Fed Chair Powell signalled that higher energy prices resulting from the Iran war have not yet required immediate policy action, as the Fed can afford to wait and assess the war's economic and inflationary impacts. While inflation remains above the 2% target, longer-term inflation expectations remaining anchored. Markets reacted by removing rate hike bets for this year. Fed's Williams echoed Powell, noting the current rate setting allows flexibility to monitor inflation pressures before acting.

In the euro area, the EU Commission's business sentiment survey indicates a sharp rise in selling price expectations for the next months in the industry for March, while services remained unchanged. The increase in industry expectations mirrors trends from 2021-2022 but remains below peak levels. Services, which typically lag industry, offer some reassurance for the ECB. Overall, the data aligns with PMI price trends and does not strongly point toward an April rate hike.

German CPI inflation rose in March, as expected, to 2.7% from 1.9% in February. The HICP measure rose marginally less than expected to 2.8% y/y (cons: 2.9%). German inflation rose to the highest level since January 2024, driven entirely by a 7.6% m/m surge in energy prices due to the Iran war. This increase is half the size of the March 2022 spike during Russia's invasion of Ukraine. Core inflation remained stable at 2.5% y/y, with no impact beyond energy.

In Sweden, retail sales declined by 0.6% m/m in February 2026 compared with January. On a year-on-year basis, the calendar-adjusted retail trade volume grew by 2.4% in February. Sales of durables fell by 0.9%, while sales of consumables (excluding Systembolaget, the state-owned liquor store chain) remained flat.

Equities: Global equities had a steady run in European hours with "everything" in green. Upon US hours that sentiment shifted, leaving the MSCI world down 0.4%. S&P500 declined 0.4%, Nasdaq 0.7%, Russell2000 -1.5%. Stoxx600 was up 0.9%. Overnight, Asian equities are down, amid higher US futures, which up about 0.9%.

FI and FX: With no imminent signs of deescalation in the Middle East, asset vols remain at or close to year highs. That said, we have seen a notable change in price action this week with yields - both nominal and real yields - coming lower. This marks an important difference to recent weeks amid markets increasingly becoming concerned about the negative impact on growth from the war and the rising likelihood of central banks hiking into slowing economies. In FX markets, it has been a relatively calm start to the week albeit SEK has been a prominent underperformer amid renewed USD strength which has returned EUR/USD down below the 1.15 support level.

Bonds Rebound as Yields Become Attractive

Yesterday was marked by a rebound in sovereign bonds on expectation that rising oil prices—which will send inflation soaring in the coming months—would also hit economic growth and, in turn, limit central banks’ ability to raise rates to the extent currently priced by markets. In other words, higher energy prices—and possible energy scarcity—could slow global economies enough to prevent central banks from tightening as aggressively.

A benchmark European 10-year yield moved lower after rising to its highest levels since 2011, the British 10-year gilt yield fell back below the 5% psychological mark, while the US 2-year yield—which best captures Federal Reserve (Fed) rate expectations—retreated to 3.80%, as Fed Chair Jerome Powell also said that longer-term US inflation expectations remained ‘in check’ despite the energy-led inflation wave already hitting the economy. ‘By the time the effects of a tightening monetary policy take effect, the oil price shock is probably long gone, and you’re weighing on the economy at a time when it’s not appropriate’, he said.

In summary, bond investors—including large institutional players—considered that yields had risen enough to become attractive.

And that’s fair: slowing growth will likely be the consequence of this energy shock, alongside tighter monetary policy to address the resulting inflation spike. But first, central banks – at least some of them - will adjust their rates to fight inflation. Depending on the impact on growth, they may later have to ease policy again. However, jumping directly to the conclusion that central banks will soon loosen policy—and that lower yields are good news for equities—is far-fetched.

The Stoxx 600 rebounded nearly 1% yesterday, while the FTSE 100 gained 1.61%. In the case of the FTSE 100, the rally in energy and mining stocks made sense, but for European companies facing another energy shock and higher rates, I found yesterday’s optimism weakly supported as a basis for a sustainable rebound.

In fact, early CPI figures for March confirm that inflation in Germany jumped from 1.9% to 2.7% y-o-y, and 1.2% over the month. Unsurprisingly, rising oil prices were the main driver.

A separate survey from the European Commission suggested a notable increase in selling price expectations, undoubtedly linked to soaring energy costs.

Other euro area countries will release their CPI updates in the coming hours and will likely confirm energy-driven price pressures.

For those still in doubt, European Central Bank (ECB) officials have been insisting that they will act to rein in inflation—and they are not necessarily looking past the short-term spike (like Powell does). This means rate hikes could be on the table this year for the euro area.

So I can’t help but think that there could be more pain ahead for global businesses—pain from higher energy prices and tighter financial conditions—before any relief.

In the US, falling yields failed to help the S&P 500 consolidate earlier gains, and the index quickly came under selling pressure, and closed the session 0.39% down.

US and European are better bid and oil is coming down from an early-session peak at the time of writing on news that Trump told his aids that he wants to end the war even if the Strait of Hormuz remains closed. But just before, mood was ugly on an Iranian struck on a Kuwaiti oil carrier near Dubai...

What’s interesting is that periods of economic slowdown don’t necessarily lead to a one-way market meltdown. Typically, market selloffs deepen into a recession and during its early months, after which looser central bank policies help markets recover. However, I feel that today’s uncertainty and negative developments have not yet been fully priced in to justify that conclusion. The Nasdaq 100 entered correction territory on Friday, while the S&P 500 is near 10% lower, hovering near correction levels. Rising energy prices are supportive for energy companies, but most other industries are facing higher operating costs and margin pressure—something that is not yet fully reflected in prices.

A FactSet chart shows that forward EPS continues to rise, driven by AI-related upgrades, resilient margins and strength in the energy sector—suggesting that markets are still pricing current earnings momentum while pushing the potential profit squeeze from higher costs further into the future.

The risk, therefore, is that markets are still buying today’s earnings story while choosing to worry about the oil shock tomorrow.

Meanwhile, oil prices continue to surge. WTI is trading near $104 per barrel, while Brent crude flirts with $110pb. US gasoline prices have rebounded to $3.38 per gallon yesterday – the highest since the Iran war began. Donald Trump may have told his aids that he wants to stop the war, but a few hours before he had threatened to destroy Iran’s energy infrastructure, and Houthi forces are now targeting alternative routes used to export oil from the Gulf amid disruptions in the Strait of Hormuz.

Higher oil prices continue to support a stronger US dollar. Major currencies remained under pressure yesterday despite relatively dovish comments from Jerome Powell—confirming that divergence between the Fed and other, relatively more hawkish, central banks does not necessarily drive short-term FX moves. The EURUSD slipped below 1.15 despite the rebound in German CPI and Powell’s balanced remarks on long-term US inflation expectations. Softer oil prices could eventually reverse the dollar’s strength, but as long as oil prices remain elevated, the dollar is likely to benefit.

Gold rebounds on the back of falling sovereign yields after testing technical support last week—the 38.2% Fibonacci retracement of the 2023 to January rally, which typically separates a continuation of the uptrend from a medium-term consolidation phase. Lower yields reduce the opportunity cost of holding non-interest-bearing gold.

The question now is whether gold can regain its safe-haven status and inflation-hedging appeal if equity market losses accelerate.

This will likely depend on a combination of factors, including oil prices, the US dollar and bond yields. For now, selling pressure appears to be easing, but the risk of further downside remains.

Markets will therefore continue to be driven by headlines and oil price dynamics, and until there is meaningful progress toward peace, any rebound in equities, bonds or gold is likely to remain fragile.

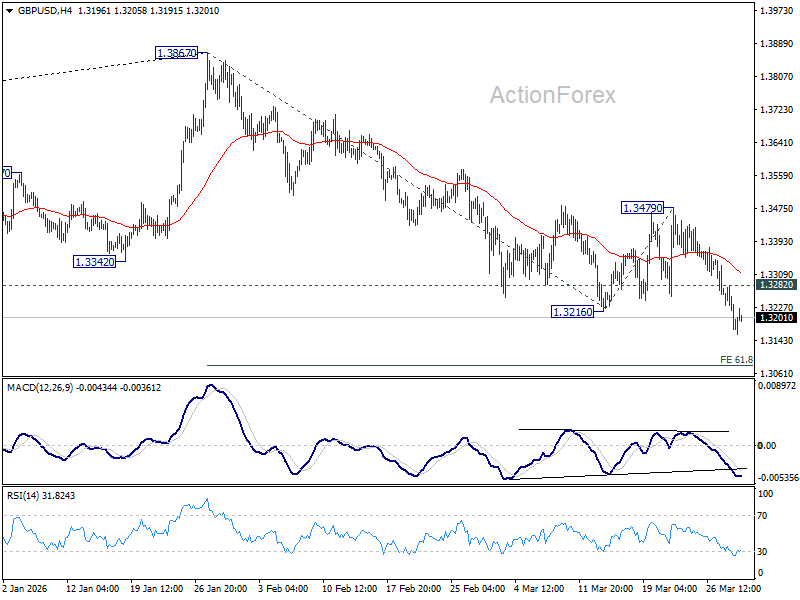

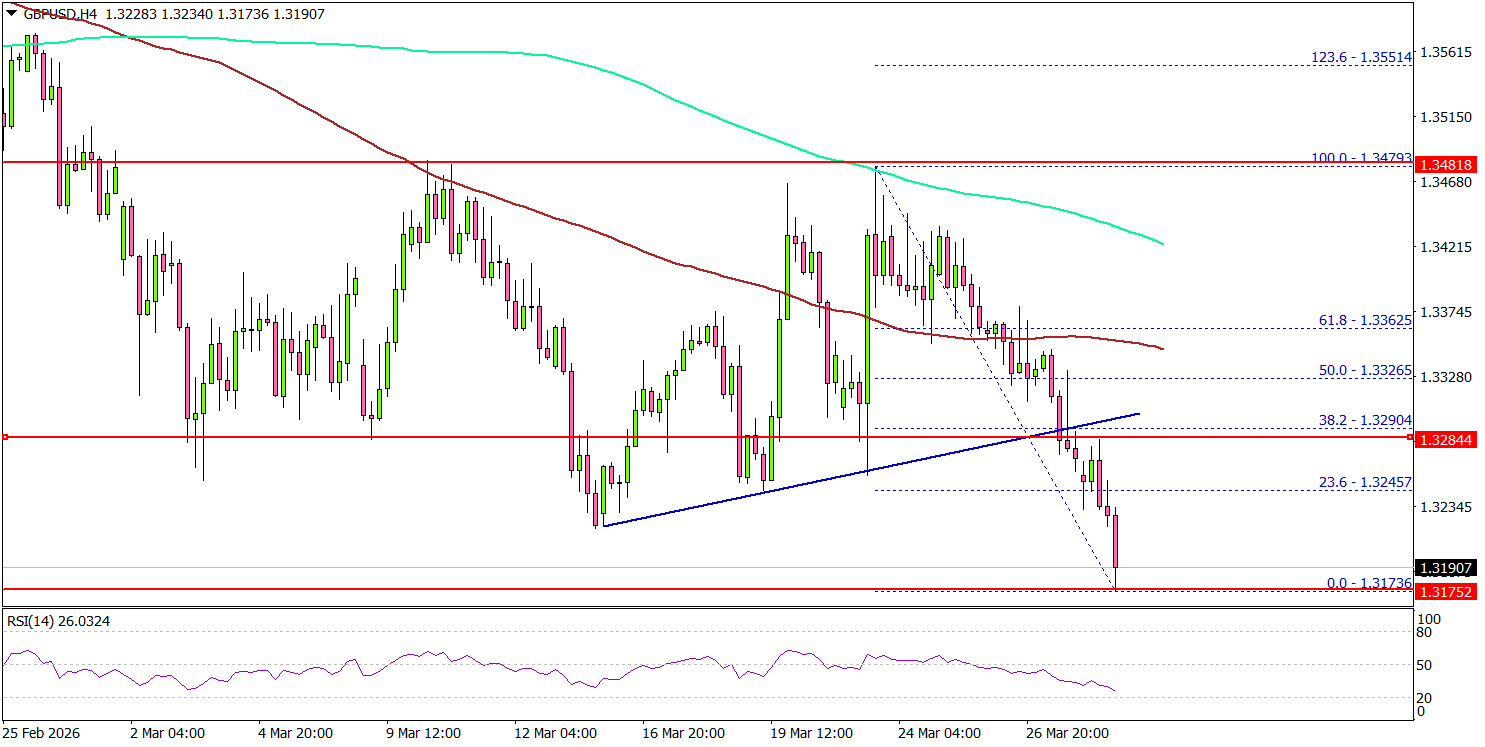

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3144; (P) 1.3213; (R1) 1.3253; More...

GBP/USD's fall from 1.3867 resumed by breaking through 1.3216 support. Intraday bias is back on the downside for 61.8% projection of 1.3867 to 1.3216 from 1.3479 at 1.3077 first. Decisive break there could prompt downward acceleration through 1.3008 support to 100% projection at 1.2828. On the upside, above 1.3282 minor resistance will turn intraday bias neutral. But outlook will remain bearish as long as 1.3479 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

Markets Shrug Trump Iran Exit Report as Oil Prices Hold Firm on Supply Risks

The global energy market has effectively shrugged off a Wall Street Journal report suggesting US President Donald Trump is exploring an Iran exit strategy. Brent oil stays above $110 after a remarkably shallow dip. Asian stocks also turned red after a brief relief bounce. With the Strait of Hormuz still effectively blocked and the April 6 deadline for "complete obliteration" approaching, the current "skeptical hope" is being overwhelmed concerns over Oil supply risks.

The Wall Street Journal reported that Trump is willing to wind down the military campaign even if the Strait is not fully reopened, aiming to avoid a prolonged conflict beyond his preferred four-to-six-week timeline. The administration is said to be pivoting toward a “containment” strategy, relying on prior damage to Iran’s naval and missile capabilities while shifting the burden of reopening maritime routes to diplomatic efforts and regional allies.

However, markets are showing clear skepticism toward this narrative. Brent continues to hold above 110, with the recent rally still on track to retest the 120 psychological level. The limited downside response reflects the fact that core risks remain unchanged—military operations continue and the Strait of Hormuz is still largely closed, leaving global supply conditions tight.

More importantly, the downside scenario remains asymmetric. If no agreement is reached by the April 6 deadline to reopen the Strait, the U.S. could escalate by targeting critical infrastructure, including desalination plants, oil refineries, and the power grid. Such a move would likely force the IRGC to "go for broke," attempting to sink remaining tankers to physically block the Strait with wreckage. Oil prices would than very likely shoot through the roof in this worst case scenario.

In currency markets, safe-haven demand remains evident. Yen is currently the strongest performers for the week so far, reflecting persistent risk aversion. Yen gains have been supported by intensified verbal intervention from Japanese authorities, reinforcing the 160 level in USD/JPY as a "Red Line". Swiss Franc is also regaining traction as a defensive asset, benefiting from broader uncertainty. Dollar remains firm overall, supported by both safe-haven demand and elevated energy-driven inflation expectations.

On the other hand, risk-sensitive currencies are under pressure. Kiwi is the weakest performer, followed by Sterling and Aussie. In the case of the Australian Dollar, risk-off sentiment is outweighing expectations for further RBA tightening with multiple hikes in the months ahead. Euro and Loonie are trading in the middle of the pack.

In Asia, at the time of writing, Nikkei is down -1.01%. Hong Kong HSI is down -0.53%. China Shanghai SSE is down -0.25%. Singapore Strait Times is down -0.02%. Japan 10-year JGB yield is down -0.011 at 2.349. Overnight, DOW rose 0.11%. S&P 500 fell -0.39%. NASDAQ fell -0.73%. 10-year yield fell -0.098 to 4.342.

RBA Minutes Highlight Excess Demand and Oil Shock as Case for Further Tightening

RBA raised rates to 4.10% in a split 5–4 decision, with minutes showing growing concern over oil-driven inflation risks. The Board signaled more tightening may be needed, despite uncertainty around growth and the Middle East conflict. Read More.

China PMIs Return to Expansion as Output and Orders Rebound, but Cost Pressures Surge

China’s Manufacturing PMI rose to 50.4 in March, signaling a return to expansion as production and new orders improved. However, input costs surged sharply, while output prices lagged, pointing to growing margin pressure. Non-manufacturing activity also edged back into expansion. Read More.

NZ ANZ Business Confidence Tumbles to 32.5 as Cost Pressures Surge to Highest Since 2023

New Zealand business confidence tumbled in March as cost pressures surged to the highest since 2023, with more firms expecting to raise prices. Inflation expectations also climbed while activity outlook weakened, pointing to a growing stagflation risk. Read More.

Japan Tokyo CPI Core Weakens to 1.7% as Energy Subsidies Drag Inflation Lower

Tokyo CPI slowed to 1.7% in March, marking a second month below the BoJ’s 2% target as energy subsidies continued to suppress prices. However, the sharp slowdown in gasoline declines points to rising oil pressures beginning to offset policy support. The data highlight a fragile balance between near-term disinflation and emerging upside risks. Read More.

Japan Factory Output Contracts as Auto Weakness Weighs, Outlook Remains Uncertain

Japan industrial production fell -2.1% in February after a 4.3% rise in January, with weakness across most sectors led by autos. Retail sales also disappointed, pointing to soft demand, while unemployment edged lower to 2.6%. The data highlight a mixed outlook with fragile growth but stable labor conditions. Read More.

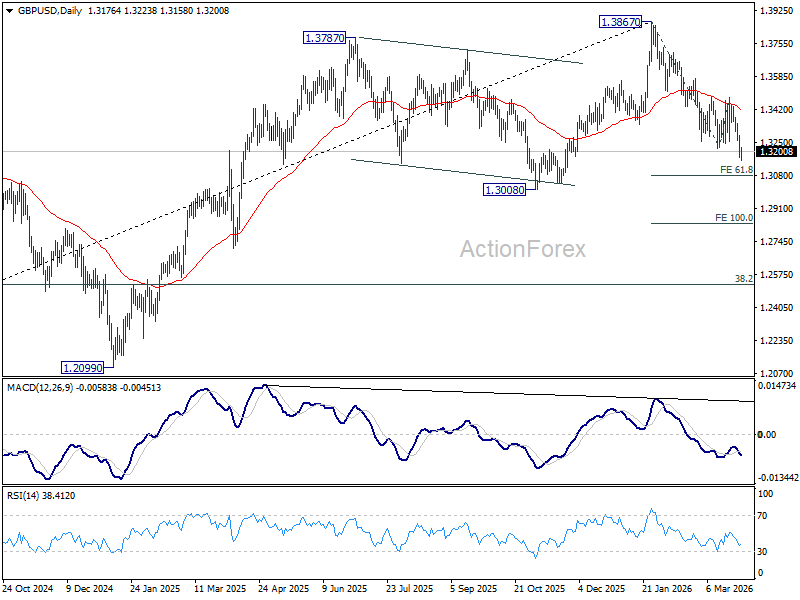

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3144; (P) 1.3213; (R1) 1.3253; More...

GBP/USD's fall from 1.3867 resumed by breaking through 1.3216 support. Intraday bias is back on the downside for 61.8% projection of 1.3867 to 1.3216 from 1.3479 at 1.3077 first. Decisive break there could prompt downward acceleration through 1.3008 support to 100% projection at 1.2828. On the upside, above 1.3282 minor resistance will turn intraday bias neutral. But outlook will remain bearish as long as 1.3479 resistance holds, in case of recovery.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

China PMIs Return to Expansion as Output and Orders Rebound, but Cost Pressures Surge

China’s official PMIs showed a return to expansion in March, with Manufacturing PMI rising from 49.0 to 50.4, beating expectations of 50.3 and marking the strongest reading in a year. The rebound snapped two months of contraction, driven by a pickup in production and a sharp improvement in new orders, with export demand showing notable momentum.

Underlying details point to a partial recovery. The production index rose by 1.8 51.4. New orders climbed by 3.0 to 51.6. However, the recovery remains uneven, with sub-indices for employment, raw material inventories, and delivery times still in contraction.

At the same time, inflation pressures are building. The purchase price index surged from 54.8 to 63.9. Output prices also increased but at a more modest pace, indicating limited pricing power for firms.

Meanwhile, Non-Manufacturing PMI rose from 49.5 to 50.1, returning to expansion. The data point to a tentative recovery in activity, but one increasingly challenged by rising input costs and margin pressure.

RBA Minutes Highlight Excess Demand and Oil Shock as Case for Further Tightening

RBA minutes at the Mrach meeting revealed a clear bias toward further near-term tightening, as policymakers judged that inflation remains too high and risks have increased following the recent surge in oil prices. Members noted that “inflation remained too high” and that the economy was still operating with "excess demand", with labour market conditions tightening slightly further beyond levels consistent with full employment.

A key shift in the discussion was the impact of the Middle East conflict on inflation dynamics. Members agreed that the rise in oil prices would “increase inflation significantly in March,” while also acknowledging that higher energy costs would likely weigh on activity. However, they emphasized that monetary policy cannot offset the initial price shock, but must act to prevent it from becoming entrenched. In particular, tighter policy could “reduce the extent to which higher costs would be passed on to final prices.”

This underpinned the case for further tightening, with members agreeing that “further tightening in monetary policy would likely be required in the near term” and that it was “not clear that [financial conditions] were sufficiently restrictive.” The persistence of excess demand, combined with rising short-term inflation expectations, strengthened the argument for acting sooner rather than later.

At the same time, the Board acknowledged significant uncertainty, particularly around the evolution of the Middle East conflict and its implications for growth. Some members argued for holding rates steady to gather more information, citing risks that consumption could weaken and that labour market tightness may ease. However, the majority concluded that the upside risks to inflation warranted action, while emphasizing that future policy decisions would remain data-dependent.

RBA raised interest rate by 25bps to 4.10%, with 5-4 vote, at that meeting.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 16 and 17 March 2026

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker AM, Renée Fry-McKibbin, Ian Harper AO, Carolyn Hewson AO, Bruce Preston, Iain Ross AO, Jenny Wilkinson PSM

Others participating

Sarah Hunter (Assistant Governor, Economic), Brad Jones (Assistant Governor, Financial System), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Andrea Brischetto (Head, Financial Stability Department), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Financial conditions

Members commenced their discussion of financial conditions by considering the impact on markets of the current conflict in the Middle East. Global prices for oil and other forms of energy had risen sharply, short-term inflation expectations had picked up and financial market volatility had increased. The conflict was likely to pose a material adverse supply shock to the global economy, though members agreed that the eventual scale and persistence of the shock was highly uncertain at the time of the meeting. Consistent with that, market prices had continued to be volatile as market participants revised their assessment of the potential implications in response to the flow of information. Members noted that, despite the pronounced volatility, financial markets had so far continued to function effectively.

Market expectations for future central bank policy rates had risen materially in almost all economies since the onset of the current conflict, in anticipation of increased near-term inflationary pressures. This included some central banks that had previously been expected by market participants to lower rates over 2026, such as the US Federal Reserve and the Bank of England, which, at the time of the meeting, were expected to hold rates steady or possibly raise them. Members discussed why markets did not expect most central banks to look through the supply shock emanating from the conflict. They noted that this was more difficult to do when the shock was expected to be large and inflation had been above target for some time (as was the case in many economies).

Government bond yields had increased since the start of the current conflict in the Middle East, including in Australia. The largest increases had occurred in countries where near-term expectations for policy rates or inflation had increased most sharply in response to the outlook for higher energy prices or inflation. Market-implied measures of longer term inflation expectations were still well anchored in most countries, including in Australia, as markets expected central banks to adjust monetary policy as required.

Risk premia in equity and corporate bond markets had risen a little since the onset of the current conflict, including in Australia, but remained low overall. The largest falls in equity prices had been in economies that were large net energy importers, such as the euro area, the United Kingdom, Japan and Korea. In some Asian markets, these declines had merely offset strong gains earlier in the year. By contrast, the decline in US equity prices since the onset of the conflict had followed their earlier underperformance arising from concerns about the effect of artificial intelligence (AI) on corporate profitability and vulnerabilities in private credit markets.

Members turned to assessing the stance of financial conditions in Australia. While financial conditions had tightened in prior months, and particularly since the start of the current conflict in the Middle East, incoming data continued to suggest that this had occurred from a less restrictive position in the second half of 2025 than previously assessed. Accordingly, the extent to which overall financial conditions were restrictive at that time remained a matter of some uncertainty.

The tightening in financial conditions over prior months had been driven primarily by higher market interest rates. Banks had passed on the increase in the cash rate in February to borrowers and market prices implied that expectations for the future path of the cash rate had shifted up further since the previous meeting. There were tentative signs that the earlier rise in cash rate expectations had weighed a little on credit demand.

Members considered a range of recent indicators that suggested financial conditions were not especially restrictive. Spreads between bank lending rates and the cash rate remained low compared with most of the preceding 20 years, even though risk premia had widened a little since the start of the current conflict in the Middle East. Growth in credit had exceeded growth in GDP in the December quarter, despite having since slowed a little; both household and business credit were rising at the time of the meeting relative to the relevant measures of income, with growth in business credit particularly strong. However, members also noted that households had continued to make relatively large extra mortgage payments, which could be consistent with more restrictive monetary policy encouraging a higher saving rate.

Members noted that several other metrics also suggested that policy might be somewhat less restrictive than previously assessed. The cash rate sat within the range of model-based central estimates of the neutral rate. These had generally moved a little higher over 2025, suggesting that any given cash rate might be somewhat less restrictive than previously. Members noted that such estimates are subject to considerable estimation error and do not provide a direct guide to the appropriate stance of monetary policy. Nevertheless, they were consistent with the staff’s February inflation forecasts, which did not have inflation fully returning to the midpoint of the target range over the forecast period even with a technical assumption of at least one more increase in the cash rate. Members also observed that the real short-term interest rate had fallen in preceding months, given the rise in actual and expected near-term inflation.

Members explored the rise in market expectations for the cash rate since the previous meeting. The rise had reflected stronger-than-expected data, recent increases in energy prices and RBA communication. Market pricing indicated a 70 per cent probability of a 25 basis point rate increase at the current meeting and a greater than 100 per cent probability of a rate rise by May, with a further increase fully priced by August. Overall, the expected market path was around 35 basis points higher at the end of 2026 compared with the path assumed in the February forecasts. The median of market economists’ expectations was for an increase in the cash rate in March and another by August.

The Australian dollar had appreciated a little further over February. The current conflict in the Middle East had modestly increased volatility in foreign exchange markets, but the direct effect on the Australian dollar had so far been limited; the depressing effect of weaker global risk sentiment had been offset by a boost from wider yield differentials (reflecting increased cash rate expectations in Australia) and higher commodity prices. Members noted that the appreciation of the Australian dollar had been broadly based across major currencies and trading partners and had contributed to a further modest tightening in financial conditions. However, members reiterated their observation from the previous meeting that this response is consistent with the standard transmission of monetary policy, not additional to it.

Economic conditions

Members noted that the economic data received since the previous meeting had, on balance, been broadly aligned with the forecasts in the February Statement on Monetary Policy, but that their composition pointed to slightly higher domestic capacity pressures than previously assessed. In particular, labour market conditions were judged to be slightly tighter than expected and, consistent with that, model-based estimates of the output gap – which had already indicated excess demand – had been revised slightly higher. Survey measures of firms’ capacity utilisation had also remained above average.

GDP growth in Australia had picked up strongly in the December quarter, exceeding the staff’s estimate of the potential growth rate and adding to existing capacity pressures. Overall growth in the quarter had been as expected but the composition of spending had showed stronger-than-expected exports, inventory accumulation and business investment, offset by significantly weaker-than-expected household consumption (with public demand broadly as expected). Over 2025, there had been strong growth in total private demand, with consumption, business investment and dwelling investment all contributing. Labour productivity growth had increased over 2025 to around the staff’s assumption for its medium-term trend.

Members noted that the staff’s expectation for overall GDP growth in the March quarter was broadly unchanged (with most of the potential impacts on growth from the current conflict in the Middle East likely to take longer to become apparent). The weaker-than-expected outcome for consumption in the December quarter, coupled with more recent monthly indicators (including timely but volatile private bank data on household spending) had suggested some downside risk to the level of household spending in the March quarter. But strong growth in real household disposable incomes and wealth had continued to support a solid near-term outlook. The near-term outlook for business investment and exports had also strengthened; the staff’s assessment was that investment would continue to be supported by spending related to technology and the energy transition, and that exports would be supported by resilient trading partner growth (underpinned by the global AI boom).

Members noted that several indicators suggested that labour market conditions in Australia may have tightened a little since the previous meeting. The unemployment rate was unchanged in January, against expectations for some unwinding of the decline in December 2025. Average hours worked, job advertisements and employment intentions from liaison information had all ticked up over preceding months and the rate of layoffs had trended slightly lower in late 2025. Growth in the private sector wage price index in the December quarter had also been marginally stronger than expected, and revisions to historical data no longer implied that it had slowed over 2025. By contrast, growth in the national accounts measures of average earnings and unit labour costs had eased by more than expected in the December quarter. Members noted that this might be a sign that the labour market had been somewhat looser in late 2025 than assessed, but that it was too early to take much signal from these measures in view of their volatility.

On inflation, the staff judged that the monthly CPI data for January were consistent with the forecast at the previous meeting that underlying inflation would remain high in the March quarter, before easing somewhat as less persistent drivers unwound. Members noted that Australia was not unique in experiencing ongoing inflationary pressures – other countries were also seeing underlying inflation remaining somewhat above their central banks’ targets.

Members considered the various components of the January CPI data. Market services inflation had increased in January by a little more than expected and the staff judged it was likely to remain above its long-run average in the March quarter. By contrast, consumer durables inflation was still expected to ease in the March quarter, with the weaker-than-expected outcome for household consumption in the December quarter 2025 supporting this judgement. Housing inflation in January was slightly below expectations but was expected by the staff to remain firm in the March quarter before easing thereafter. Members noted that this profile of slowing housing inflation was consistent with growing expectations from the second half of 2025 that financial conditions would tighten.

Having considered the domestic data, members discussed how the current conflict in the Middle East could affect future economic activity and inflation in Australia. While the situation was highly uncertain, it was already clear that global energy production and distribution had been disrupted significantly and that there had been considerable increases in the global prices of oil and natural gas. Higher petrol prices would flow through directly to headline inflation in Australia (and globally) in the near term. While a full update of the forecasts had not yet been prepared, the staff shared a simple estimate that the direct effect (via petrol prices) of oil prices remaining around US$100 per barrel would on its own lift headline inflation in Australia to around 5 per cent over the year to the June quarter, around ¾ of a percentage point higher than had been expected in February. Sustained higher oil prices would also boost inflation more broadly over time as input costs for firms rose and some of this effect was passed onto consumers. Members noted that, consistent with this analysis, short-term inflation expectations had increased further following the onset of the current conflict. They discussed the importance of ensuring that longer term inflation expectations remain consistent with the inflation target.

Members noted that a full assessment of the impact of the current conflict in the Middle East on inflation over the medium term also needed to take account of the impact on domestic economic activity. The immediate effect of higher energy prices would be to constrain the economy’s productive capacity, depressing output. However, there are offsetting effects that could potentially cushion that initial impact. For example, members noted that while Australia is a net importer of oil, it is a net exporter of energy. As a result, higher petrol prices would tighten household budgets and reduce real consumer spending, but higher liquified natural gas (LNG) prices would lift export revenue and could raise national income in aggregate if Australia’s overall terms of trade were to increase as a result. Members noted that the net effect of these opposing forces depends on how different sectors respond to the reallocation of real incomes, but that this could not be known with certainty at this early stage.

Members discussed other risks to the global economic outlook from the current conflict, including that disruptions to global supply chains could become more pronounced, uncertainty could weigh on business and household spending and that rising global risk premia could cause financial conditions to tighten sharply. The reaction of the Australian dollar exchange rate to developments would also be a key factor in determining the overall effects on domestic economic activity and inflation.

Financial stability assessment

Members turned to their semi-annual consideration of financial stability risks. They noted that while global financial stability risks had been high and rising, Australia’s financial system had established a good degree of resilience to absorb shocks. At the same time, the RBA and other agencies of the Council of Financial Regulators had continued to stress the importance of ongoing work by industry to strengthen its ability to respond to liquidity, operational and geopolitical shocks, and to safeguard lending standards amid an upswing in credit growth.

A key risk identified by the staff was the increasing potential for a disruptive repricing in global financial markets. This risk had been amplified by a material increase in leverage and concentration in key global capital markets over preceding years, while risk premia had remained low. Members noted that advanced economy sovereign debt markets abroad could become more prone to shocks. This reflected the large and growing stock of sovereign debt (which could lead to concerns over debt sustainability) combined with the growing role in these markets of leveraged, price-sensitive investors. Members noted that a period of severe global market stress – whatever its source – could increase financing costs sharply and restrict access to funding and liquidity both globally and domestically, although Australian banks had become less reliant on overseas funding over time.

Growing operational complexity and interconnectedness of financial systems had also increased the risk that operational and cyber incidents might have systemic consequences for the financial system. The geopolitical environment – including recent developments in the Middle East – had further heightened this risk.

In considering the resilience of the Australian financial system, members noted that housing-related vulnerabilities had so far remained contained. Investor housing credit growth had picked up strongly, but investors tended to have higher incomes and historically had been less likely to default than other borrowers. Investor activity could nonetheless contribute to unsustainable increases in housing prices and leverage, and potentially erode lending standards as other borrowers attempted to enter a rising market (though this had not been apparent to date). Members noted that the Australian Prudential Regulation Authority (APRA) had activated limits on high debt-to-income (DTI) lending to protect against a material build-up of vulnerabilities. They observed that high DTI lending to investors had increased but remained well below the new limits.

For owner-occupier borrowers, higher interest rates and inflation would be likely to increase budgetary pressures. However, mortgagors across the income distribution had continued to build up their saving buffers over the prior year or so and most maintained solid cash flow positions.

Most Australian businesses had also remained resilient over the preceding year, although conditions had been challenging for some industries even prior to the recent energy price rises. Credit had been readily available and competition among lenders had remained strong. There had been a slight easing in lending standards for some businesses, particularly those involved in commercial real estate, but there had been little evidence of a broader decline in business lending standards.

Members noted that Australian banks remained in a strong position to continue supporting the economy, even if there were an economic downturn. Banks were well capitalised and provisioned and their holdings of liquid assets exceeded regulatory requirements. However, regulators around the world – including APRA –continued to consider whether prevailing liquidity risk frameworks remain appropriate given the speed with which liquidity stress can now materialise.

Members discussed the risks from rapid private credit growth internationally. They noted the opaqueness of lightly regulated activities and linkages with the banking system in some countries. In Australia, growth in non-bank lending had also been strong and had the potential to result in increased loan losses in the future. However, members noted that the direct financial stability risks from this activity in Australia were limited by the relatively small size and structure of the non-bank sector.

Members concluded their consideration of financial stability risks by discussing the risks posed by the large and growing superannuation sector. They recognised that this sector historically had been a stabilising force in the financial system but had the potential to amplify stress in the future. These risks will be heightened by an increasing number of Australians drawing retirement income streams from the system. Members noted that this warranted a further strengthening of superannuation funds’ governance, liquidity and operational risk management practices, which would remain a key focus for regulators.

In light of this analysis, members judged domestic financial stability considerations posed no immediate issues for monetary policy. Close monitoring was nevertheless required given the rapidly evolving risk environment.

Considerations for monetary policy

Members noted that inflation remained too high, the economy was operating with excess demand and the staff’s assessment was that the extent of excess demand had increased slightly since the previous meeting. Labour market conditions were assessed to have tightened a little further relative to the level consistent with full employment, notwithstanding an easing in growth in unit labour costs. Forward-looking indicators suggested that the labour market was likely to remain resilient in the near term.

Members agreed that the rise in oil prices would increase inflation significantly in March. Short-term inflation expectations had risen in response, but measures of long-term inflation expectations had been stable to date (including because investors remained confident that monetary policy would respond appropriately). Members agreed that the reduction in oil supply and associated higher prices would probably also reduce economic activity domestically and internationally. However, this would depend on the evolution of the current conflict in the Middle East, how various sectors responded to the resulting reallocation of income and how the conflict affected domestic sentiment and global demand. Members agreed that it was not possible to be confident about either the future evolution of the conflict or how these various factors would play out over the longer term.

Although financial conditions had tightened a little since the previous meeting, members acknowledged that the extent to which monetary policy was restrictive was still uncertain. They agreed that financial stability considerations held no immediate implications for monetary policy.

In light of these observations, members considered the arguments for and against raising the cash rate target.

Members agreed that further tightening in monetary policy would likely be required in the near term to bring inflation back to target within a reasonable timeframe. They observed that the forecast at the previous meeting had been for inflation to remain above target for some time and still to be slightly above the midpoint of the target range at the end of the forecast period, even under a technical assumption that incorporated a further increase in the cash rate. The rise in oil prices had further increased the risk that inflation would remain above target for a prolonged period. Members also noted that downside risks to the outlook for the labour market had abated over prior months. Given these observations, members agreed that financial conditions needed to be restrictive and that it was not clear that they were sufficiently so at present.

Having agreed that some near-term tightening was likely required, members then considered whether that should begin at this meeting or in the near future.

The case to increase the cash rate target at the current meeting was founded on a view that the risk that inflation may not return to target within a reasonable timeframe had increased enough to warrant an immediate response. Members noted that this view could be supported by the presence of widespread capacity pressures, an assessment that there was a little more excess demand in the economy than had been judged previously, and the scale of the likely inflationary effect of the rise in global oil prices. Members agreed that monetary policy could not prevent a near-term increase in inflation induced by sharply higher petrol prices, but that it could reduce the risk that this would flow into persistent inflationary pressures (in an economy that was already in a position of excess demand). In particular, members noted that tighter monetary policy could constrain future price rises by curtailing any upward pressure on inflation expectations and reducing the extent to which higher costs would be passed on to final prices.

The case to raise the cash rate target at this meeting could be further strengthened if members judged that the labour market remained tighter than was consistent with full employment and that the risk of this unwinding quickly had declined. Members noted that such a judgement could be supported by the staff’s assessment of conditions in the labour market and the signal from a range of indicators that near-term labour demand remained firm. It could be further strengthened if members concluded, based on trends in the unemployment rate and other indicators, that the labour market may have tightened a little since mid-to-late 2025. Members acknowledged that these indicators pre-dated the onset of the current conflict in the Middle East, which, if it persisted, could lead to a reduction in labour demand. However, they noted that the immediate effect of higher oil prices is to reduce aggregate supply, further exacerbating existing capacity pressures, with aggregate demand subsequently responding to a rise in prices. They recognised that the conflict could subsequently also result in an additional contraction in aggregate demand as sentiment and global demand weakened, but this would depend on how the conflict evolved, the willingness of households to adjust their saving rate and the potential cushioning effect on aggregate national income of higher LNG prices.

Finally, the case to raise the cash rate target at this meeting would be further strengthened if members formed the view that financial conditions were insufficiently restrictive or even accommodative. Members discussed the extent to which such a judgement could be supported by the February forecasts, trends in credit growth, developments in market risk premia and model estimates of the neutral interest rate. This judgement would also be strengthened if members concluded that higher short-term inflation expectations, including as the result of the current conflict in the Middle East, had depressed short-term real interest rates.

The case to keep the cash rate target unchanged at the current meeting centred on concerns about the effect of heightened uncertainty on the outlook for the economy. This uncertainty, stemming especially from the current conflict in the Middle East, could mean that the potential benefits of waiting for a little more information outweighed the potential costs, even with the presumption that the cash rate target would probably need to be increased further at some point.

One source of uncertainty centred on the outlook for domestic economic growth. Members noted that while private demand growth had picked up as expected in the December quarter 2025, the outcome for consumption had been weaker than expected. Taken together with the signal from indicators of household spending in the March quarter, the dampening effect of higher petrol prices on real household disposable income and subdued consumer confidence, there was a risk that consumption growth would be weaker than forecast in February. Given the possibility that this could lead to weaker GDP growth, there was a case to wait for a little more data to assess the degree of inflationary pressure coming from excess demand.

A second source of uncertainty surrounded the extent of tightness in the labour market. Members noted that the monthly labour force survey data are volatile and need to be considered over a span of months. They highlighted the significant slowing in the national accounts measures of average earnings and unit labour costs, which might be a signal that the labour market was less tight than had been assumed (while recognising these indicators are also volatile). And members hypothesised that a rise in the cost of living could prompt workers to enter the labour market, as had been the case two years earlier, reducing labour market tightness.

A final source of uncertainty related to how the current conflict in the Middle East would evolve. There was considerable uncertainty about almost every aspect of the conflict at this early stage and therefore its impact on global and domestic economic conditions. While a near-term increase in inflation was almost inevitable, a persistent or greater disruption could result in weaker growth in aggregate demand as well as supply, with uncertain implications for medium term inflationary pressures. Members noted that, given these uncertainties, leaving the cash rate on hold at the current meeting and monitoring developments over subsequent weeks may help to calibrate the monetary policy reaction more effectively.

Having considered these arguments, a majority of members judged that the case to raise the cash rate target at the current meeting was the stronger one. These members judged that inflation had already been projected to remain above target for some time in the February Statement and that the risks around this assessment had tilted further to the upside, given both domestic and international developments. These members recognised the pervasive uncertainties over the current conflict in the Middle East. But they noted that developments in the Middle East would further reduce the already constrained supply capacity of the Australian economy, increasing inflationary pressures for any given level of aggregate demand. Indeed, developments in the Middle East would add to global and domestic inflation under a wide range of scenarios.

These members also noted that the impact of the current conflict on the outlook for aggregate demand remains uncertain, given Australia’s position as a net energy exporter and households’ generally healthy balance sheets. Moreover, these members judged that financial conditions were not sufficiently restrictive to reduce the margin of excess capacity. They therefore judged it important to demonstrate a clear commitment to returning inflation to target, noting that if medium- and long-term inflation expectations increased, it would ultimately require significantly more contractionary monetary policy to achieve the Board’s objectives. These members conceded that it would be important to monitor downside risks to future demand closely, but if growth were slightly slower than expected this could contribute to the Board achieving its objectives sooner, given the starting point of excess demand. They noted that the Board’s ability to respond effectively to a more material contraction in aggregate demand, should it occur, would not be impaired by raising the cash rate target by 25 basis points at this meeting.

A minority of members judged that the case to leave monetary policy unchanged at the current meeting was the stronger one. These members reiterated that inflation was too high and that a further tightening in monetary policy would probably be required. However, they assessed that the domestic data received since the previous meeting had not unambiguously signalled that excess demand was greater than the Board had previously assessed. They also placed more weight on the weaker-than-expected consumption outcome and slowing in the growth in unit labour costs in the December quarter 2025, and were less convinced that the labour market may have tightened further. And, while they agreed that financial conditions would probably need to become more restrictive, they felt there was merit in delaying any tightening of monetary policy until the potential effects of the current conflict in the Middle East become clearer. Given these factors, these members judged that there was merit in waiting a little longer before making the decision to raise the cash rate target. They noted that doing so would allow the Board time to gather more information that could prove helpful in informing future responses.

Having decided by majority to raise the cash rate target at this meeting, members considered the implications of their deliberation for upcoming decisions. They agreed that it was not possible to predict the future path for the cash rate target with any confidence, given the high degree of uncertainty around the breadth and duration of the current conflict in the Middle East. A longer conflict could have a material bearing on both inflation and economic activity. Members therefore acknowledged that future policy decisions would require the Board to balance its two objectives carefully.

In finalising its statement, the Board agreed to remain attentive to the data and the evolving assessment of the outlook and risks when making its decisions. The Board will remain focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

The decision

The Board resolved by majority to raise the cash rate to 4.10 per cent. Five members voted in favour; four members voted to leave the cash rate target unchanged at 3.85 per cent.

GBP/USD Continues Slide, Momentum Turns Firmly Bearish

Key Highlights

- GBP/USD started a fresh decline and traded below 1.3320.

- It traded below a bullish trend line with support at 1.3290 on the 4-hour chart.

- EUR/USD remained in a bearish zone below 1.1580.

- WTI Crude Oil prices are again moving higher above $98.00.

GBP/USD Technical Analysis

The British Pound faced rejection near 1.3480 against the US Dollar. GBP/USD started a fresh decline and traded below the 1.3320 support.

Looking at the 4-hour chart, the pair traded below a bullish trend line with support at 1.3290. It settled below the 1.3300 zone, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour).

The pair is now consolidating losses below 1.3280. Immediate support is seen near 1.3160. The first key support sits at 1.3120. A close below 1.3120 might call for heavy losses. In the stated case, it could even revisit 1.3000 in the coming days.

On the upside, the pair is now facing sellers near 1.3290. The first major resistance sits at 1.3320. A close above 1.3320 could open the doors for gains above 1.3250. In the stated case, the bulls could aim for a move to 1.3320.

Looking at Oil, the price is again moving higher, and the bulls could aim for more gains above the $105 level in the near term.

Upcoming Key Economic Events:

- UK GDP for Q4 2025 (QoQ) - Forecast +0.1%, versus +0.1% previous.

- UK GDP for Q4 2025 (YoY) - Forecast +1.0%, versus +1.0% previous.

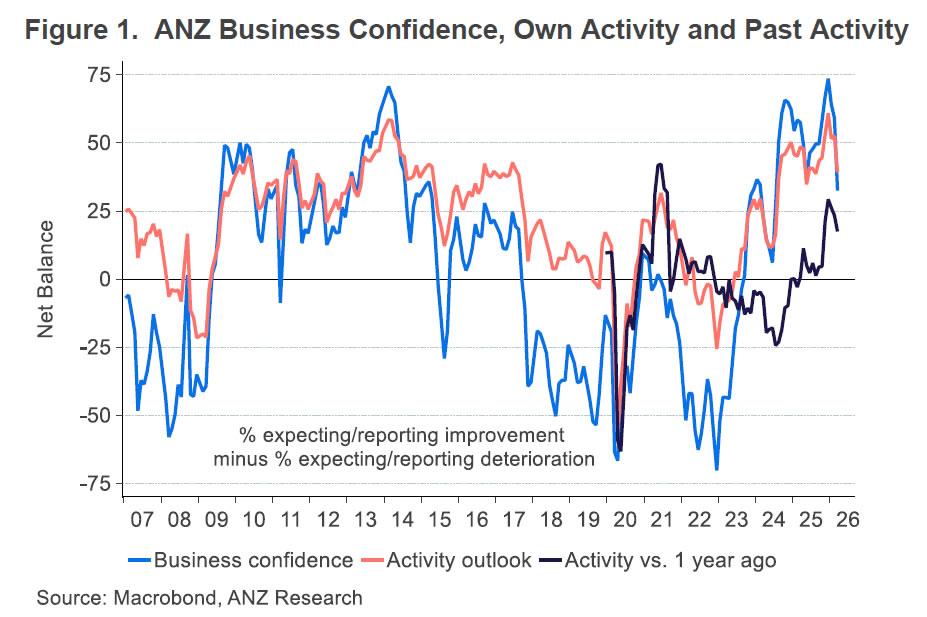

NZ ANZ Business Confidence Tumbles to 32.5 as Cost Pressures Surge to Highest Since 2023

New Zealand’s business confidence deteriorated sharply in March, with ANZ Business Confidence falling from 59.2 to 32.5 as geopolitical tensions disrupted the recovery narrative. The decline was even more pronounced in late-month responses, which averaged -23, highlighting how sentiment worsened as uncertainty intensified following the escalation in the Middle East.

The hit to sentiment was matched by a slowdown in activity expectations. Own Activity Outlook dropped from 52.6 to 39.3, suggesting firms are already seeing a pullback in demand as decision-making is deferred. ANZ noted that while recovery had begun to take hold earlier in the year, conditions shifted quickly, with businesses reporting a direct impact on activity as uncertainty increased.

At the same time, inflation pressures moved in the opposite direction. Inflation expectations rose from 2.93% to 3.08%, while the share of firms expecting to raise prices climbed 7 points to 60%, and even higher to 67% in late responses. The average expected price increase also accelerated from 2.0% to 2.4%, or 3.3% in the late-month sample, pointing to growing pricing power despite weakening demand.

Cost pressures are also intensifying, with 85% of firms expecting higher costs, up from 79% and the highest since early 2023. The late-month reading of 93% marks the strongest since mid-2022.