BoJ’s June meeting minutes, released today, confirmed that several policymakers were open to resuming rate hikes once trade uncertainty subsides. While the minutes are somewhat dated — the meeting took place before the announcement of the US–Japan trade agreement — they reveal a growing consensus that the central bank may return to a normalization path sooner than previously expected. Markets are now turning to Friday’s Summary of Opinions from the more recent July meeting, which should reflect a more upbeat outlook following the tariff deal.

Some BoJ members noted that as wages remain firm and inflation slightly exceeds expectations, the Bank would likely “shift away from the current wait-and-see approach and consider resuming rate hikes, if trade friction de-escalates” Others emphasized that while the BoJ should pause rate hikes for now due to uncertainty, it must stay “flexible and nimble,” ready to resume hikes depending on US policy and global developments.

Yen continues to strengthen this week, underpinned by falling US Treasury yields and a pickup in BoJ tightening expectations. In contrast, the Australian Dollar is under pressure as markets increasingly price in another RBA rate cut next week. The shift follows last week’s soft Q2 CPI data, which undercut arguments for extended policy pauses and revived dovish speculation.

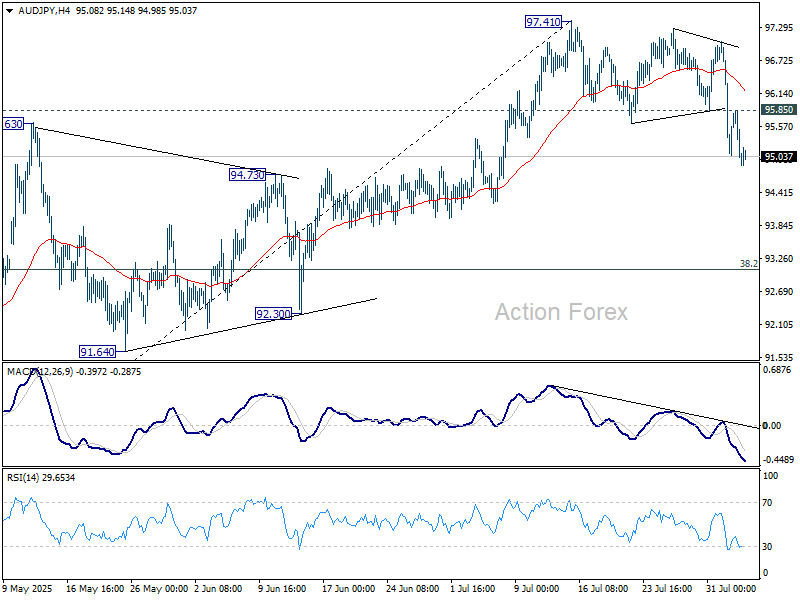

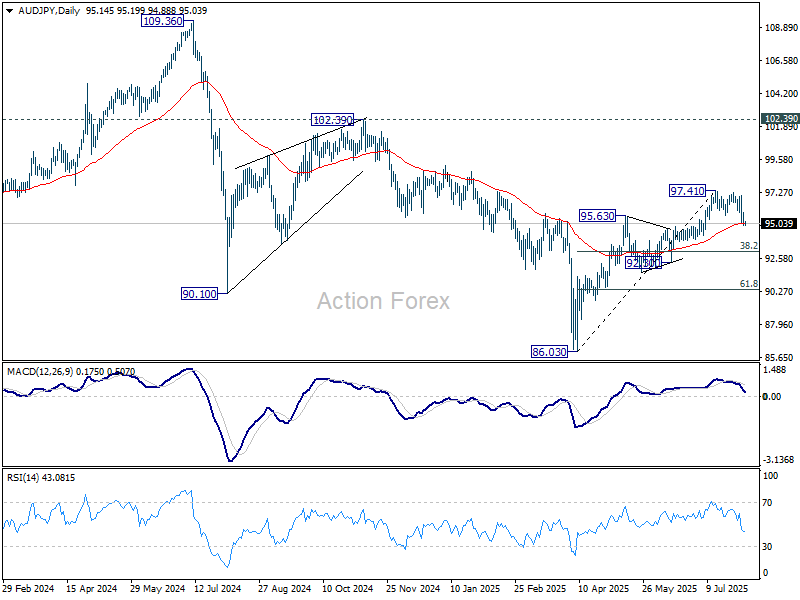

Technically, a short term top should be in place at 97.41 in AUD/JPY with breach of 55 D EMA (now at 95.08). Sustained trading below the EMA will bring AUD/JPY further lower to 38.2% retracement of 86.03 to 97.41 at 93.06, as a correction to the rise from 86.03. Nevertheless, break of 95.85 minor resistance will dampen this bearish view and turn intraday bias neutral first.

{kind=link}