Today’s high-profile events turned out to be something of a letdown for traders. Euro dipped after the ECB held its deposit rate steady at 2.00% and published new staff projections, but the move was shallow and short-lived. Markets took note that both headline and core inflation are now projected slightly below the 2% target by 2026 and 2027, hinting at a possible need for further easing down the road.

For now, however, there is no urgency for additional cuts. ECB reiterated the Governing Council’s commitment to a data-dependent stance, and unless incoming figures deteriorate notably, traders see little chance of a near-term move. That kept the euro relatively stable after its initial dip.

In the U.S., CPI data were broadly in line with expectations. Headline inflation’s 0.4% monthly rise was a touch stronger than forecast, but the annual rate of 2.9% and steady core at 3.1% highlights that inflation is not worsening much under tariff pressures.

The bigger surprise came from the weekly jobless claims report. Initial claims jumped to 263k, the highest since 2021, showing a clear softening in the U.S. labor market. With employment one half of the Fed’s dual mandate, the data reinforced expectations that policymakers will have to expedite easing to cushion the economy.

Market pricing for next week’s FOMC remains anchored to a 25bps cut, with odds for a larger 50bps move still low at about 10%. But expectations for a consecutive cut in October have surged to around 95%, showing traders are becoming more convinced of back-to-back easing.

Despite the data, currency markets remain locked in yesterday’s ranges. Swiss Franc, Euro, and Sterling are modestly firmer, while Yen and Loonie are weaker alongside Kiwi. Dollar and Aussie sit in the middle of the pack. For now, the highly anticipated breakout in FX markets has yet to materialize.

In Europe, at the time of writing, FTSE is up 0.37%. DAX is up 0.08%. CAC is up 0.67%. UK 10-year yield is down -0.008 at 4.625. Germany 10-year yield is down -0.006 at 2.650. Earlier in Asia, Nikkei rose 1.22%. Hong Kong HSI fell -0.43%. China Shanghai SSE rose 1.65%. Singapore Strait Times rose 0.22%. Japan 10-year JGB yield rose 0.01 to 1.578.

US CPI rises to 2.9% in August, core CPI unchanged at 3.1%

U.S. consumer prices rose more than expected on the month in August, with CPI up 0.4% mom versus forecasts of 0.3% mom. Core CPI rose 0.3% mom, matching expectations. Shelter costs climbed 0.4% mom and were the largest contributor to the monthly increase, while food prices rose 0.5% mom and energy gained 0.7% mom.

On a year-over-year basis, headline CPI accelerated to 2.9% from 2.7% in July, in line with forecasts. Core inflation held steady at 3.1%, also as expected. The data show underlying price pressures remain stable even as headline measures edge higher. Food inflation rose 3.2% over the past year, while energy prices were up a modest 0.2%. Overall, the report points to steady but not accelerating inflation.

US initial jobless claims spike to 263k, highest since 2021

U.S. initial jobless claims surged by 27k to 263k in the week ending September 6, well above expectations of 240k and marking the highest level since October 2021. The four-week moving average rose 10k to 241k, pointing to a clear softening trend in labor market conditions.

Continuing claims were steady at 1.939 million for the week ending August 30, with the four-week average slipping slightly to 1.936 million. Still, the rise in new claims highlights a labor market that is starting to cool more decisively, adding pressure on the Fed as it weighs the pace of policy easing.

ECB holds at 2.00% Again, upgrades 2025 growth outlook

The ECB left its deposit rate unchanged at 2.00% as widely expected, marking a second consecutive hold. The Governing Council reiterated its commitment to stabilizing inflation at 2% over the medium term and stressed a “data-dependent and meeting-by-meeting” approach. Policymakers emphasized they are “not pre-committing to a particular rate path”, leaving flexibility to respond to incoming data.

Fresh staff projections showed little change from June, with headline inflation expected to average 2.1% (prior 2.0%) in 2025, 1.7% (1.6) in 2026, and 1.9% (2.0%) in 2027.

Core inflation, excluding food and energy, is projected at 2.4% in 2025 before easing to 1.9% in 2026 and 1.8% in 2027. The figures reinforce the view that price pressures are gradually converging toward target.

On growth, the ECB revised up its 2025 forecast to 1.2% from 0.9%, but cut its 2026 estimate slightly to 1.0% (prior 1.1%). The 2027 projection was left unchanged at 1.3%.

Japan CGPI accelerates to 2.7% yoy, import price declines ease

Japan’s producer prices rose modestly in August, with CGPI climbing 2.7% yoy from 2.5% yoy in July, matching market forecasts. The pickup was driven mainly by food and beverage costs, which rose 5.0% yoy versus 4.7% yoy previously. In contrast, utility bills fell -2.9% yoy due to government subsidies, softening the overall inflation impact.

Import price declines eased significantly in the past two months, with yen-based import prices down -3.9% yoy compared with a revised -10.3% fall in July. The data suggest external cost pressures are stabilizing, even as domestic food inflation remains sticky.

RBNZ’s Hawkesby: OCR seen at 2.5% by year-end, data dependent

RBNZ Governor Christian Hawkesby said today the central bank still projects the Official Cash Rate to fall to around 2.50% by year-end, down from current 3.00%. Though, the pace could be “faster or slower” depending on incoming data. He emphasized that the path of policy easing will hinge on the “speed of New Zealand’s economic recovery”.

Hawkesby noted the August Monetary Policy Statement highlighted the sharp blow to household and business confidence, with the economy stalling mid-year and creating more slack. He attributed much of the “confidence shock” to uncertainty over U.S. tariff policies, compounded by cost-of-living pressures and a weak housing market.

Still, leading indicators for July were “better” and aligned with the RBNZ’s outlook for a rebound in the second half of the year. Hawkesby said policymakers will keep monitoring spillovers from U.S. tariffs on both global growth and New Zealand firms. The RBNZ resumed rate cuts last month after a July pause.

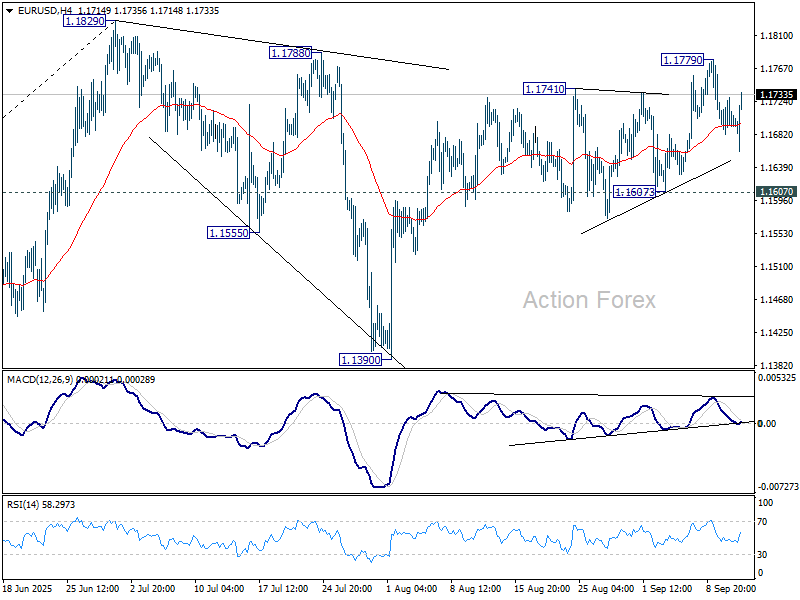

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1703; (R1) 1.1722; More…

EUR/USD is staying in range below 1.1779 temporary top despite today’s volatility. Intraday bias remains neutral for the moment. Further rise is expected with 1.1607 support intact. Above 1.1779 will bring retest of 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level.

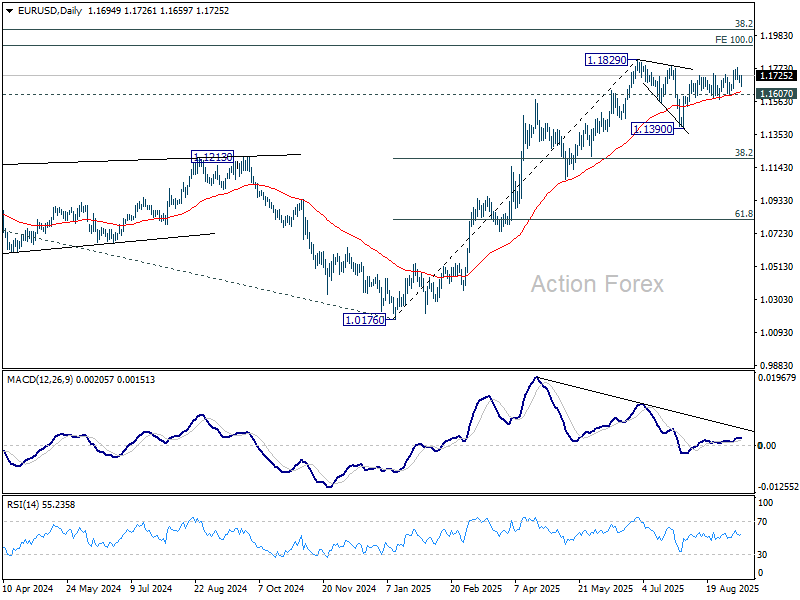

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

{kind=link}