Dollar’s broad-based selloff resumed today, with Sterling and the Euro leading gains. Investors are positioning ahead of this week’s pivotal FOMC meeting, where debate has intensified over whether the central bank could move more aggressively than expected. Dollar was the weakest major on the day, with the Kiwi also under pressure, while other currencies traded mixed.

Market chatter intensified after Societe Generale joined Standard Chartered in forecasting a 50bps Fed cut at this week’s meeting. That view contrasts with the futures market, which is pricing only around a 4% chance of such a jumbo move. More modestly, traders still see near certainty of consecutive 25bps cuts through year-end. Economists, however, broadly agree that the Fed has ground to make up, and that an aggressive easing cycle is firmly underway.

That theme is overshadowing regional developments in Europe, where Fitch downgraded France’s sovereign rating to AA- last Friday. The move, prompted by a rising debt burden, had little impact on sentiment as the Euro shrugged off the news and extended gains.

On the trade front, U.S.–China negotiations entered a second day in Spain, with Treasury Secretary Scott Bessent noting “good progress” on technical details and saying the sides were close to an agreement on TikTok. But he stressed Washington would not sacrifice national security for the sake of a social media app. Chinese officials, for their part, offered little detail.

Yet, tensions flared as Beijing launched a preliminary anti-monopoly probe into U.S. chipmaker Nvidia and denounced Trump’s push for the EU to impose secondary tariffs on China over Russian oil. China’s Commerce Ministry called the request “unilateral bullying” and vowed to take “any necessary measure” to defend its interests.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is up 0.59%. CAC is up 1.35%. UK 10-year yield is down -0.032 at 4.644. Germany 10-year yield is down -0.012 at 2.704. Earlier in Asia, Nikkei rose 0.89%. Hong Kong HSI rose 0.22%. China Shanghai SSE fell -0.26%. Singapore Strait Times fell -0.13%. Japan 10-year JGB yield closed flat at 1.602.

ECB’s Schnabel: Rates in a good place, policy should keep steady hand

ECB Executive Board member Isabel Schnabel said today that interest rates are “in a good place” as inflation stabilizes near the 2% target and the Eurozone economy shows resilience at full employment. She cited strong household and corporate balance sheets, reduced uncertainty, and fiscal expansion as key supports to domestic demand, offsetting the drag from weaker net exports.

Schnabel downplayed concerns over Chinese export dumping, noting little evidence so far, and argued that the inflationary pass-through from a stronger Euro is likely to remain “limited”.

In her view, “upside risks to inflation dominate”, with tariffs, sticky services and food prices, and expansionary fiscal policy among the potential drivers.

Given these conditions, Schnabel said monetary policy should “keep a steady hand,” tolerating moderate deviations from target while guarding against persistent upside risks.

Eurozone posts EUR 12.4B trade surplus, EU faces export weakness to US, China

Eurozone trade data were stable in July, with exports edging up 0.4% yoy to EUR 251.5B while imports rose 3.1% yoy to EUR 239.1B. That produced a EUR 12.4B surplus. Intra-Eurozone trade grew 1.9% yoy to EUR 226.1B. The numbers reflect the bloc’s continued reliance on internal demand to cushion against weaker global flows.

The EU as a whole painted a softer picture, with exports down -0.5% yoy to EUR 227.7B against imports up 1.2% yoy to EUR 215.6B. The resulting EUR 12.1B surplus was still positive but underscored the relative drag from external markets. Intra-EU trade proved firmer, rising 2.9% yoy to EUR 349.2B.

Bilateral trends showed notable divergences. EU exports to the US fell -4.4% yoy and to China -6.6% yoy, underscoring pressure from global trade frictions. By contrast, exports to the UK rose 2.9% yoy and to Switzerland surged 9.4% yoy. On the import side, flows to the EU from the US jumped 10.7% yoy, from China rose 3.9% yoy, from Switzerland 6.8% yoy, and from the UK a modest 0.6% yoy.

NZ services PMI slumps to 47.5, 18th month contraction

New Zealand’s services sector deteriorated further in August, with BusinessNZ Performance of Services Index slipping from 48.9 to 47.5, well below the long-run average of 52.9. The reading also marks the 18th consecutive month of contraction. Both

Activity/Sales (46.2) and New Orders/Business (47.8) weakened, suggesting demand remains fragile. Employment improved slightly to 48.3 but remains in contraction territory, reflecting businesses’ reluctance to expand payrolls in the face of subdued activity.

The survey showed 59.6% of respondents made negative comments in August, an increase from July but still less pessimistic than June’s tally. Firms cited multiple pressures, including high interest rates, sticky inflation, and the cost-of-living squeeze eroding household spending. Rising operating costs, seasonal slowdowns, supply chain disruptions, and uncertainty over government policy also weighed on sentiment.

China industrial output, retail sales miss forecasts, fixed asset investment slumps

China’s economy slowed in August, with key indicators falling short of expectations. Industrial output grew 5.2% yoy, down from 5.7% yoy in July and short of forecasts for 5.8% yoy, marking its weakest pace since August 2024. Retail sales also slowed, rising just 3.4% yoy versus 3.7% yoy previously and expectations of 3.8% yoy, signaling soft household demand despite ongoing government measures to support spending.

Investment activity showed the sharpest loss of momentum. Year-to-date fixed asset investment rose only 0.5%, far weaker than consensus 1.4% and July’s 1.6%. The drag came primarily from the property sector, where real estate investment plunged -12.9% in the first eight months. Excluding real estate, investment rose 4.2%.

The National Bureau of Statistics highlighted “many unstable and uncertain factors” in the global environment and warned that the economy still faces “multiple risks and challenges.” It urged stronger policy implementation to stabilize employment, businesses, and expectations, but the latest figures suggest momentum remains fragile, with property weakness continuing to weigh heavily on growth prospects.

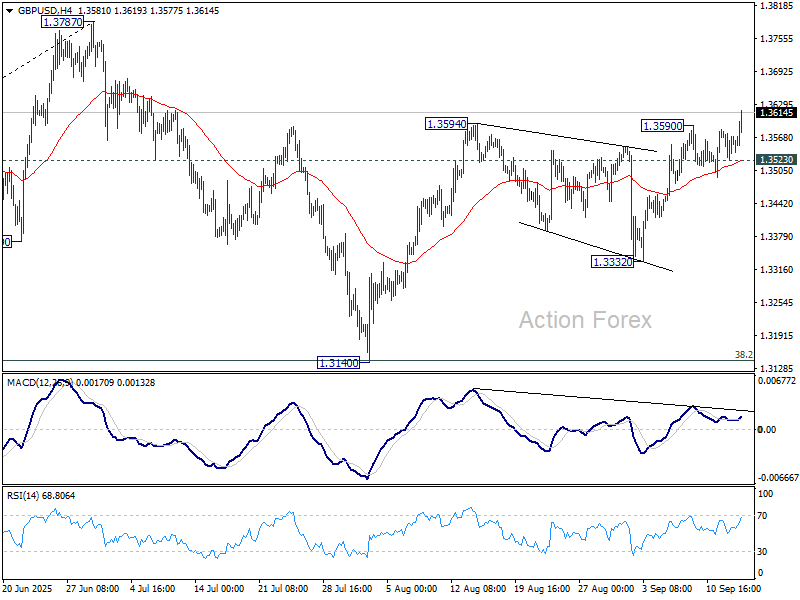

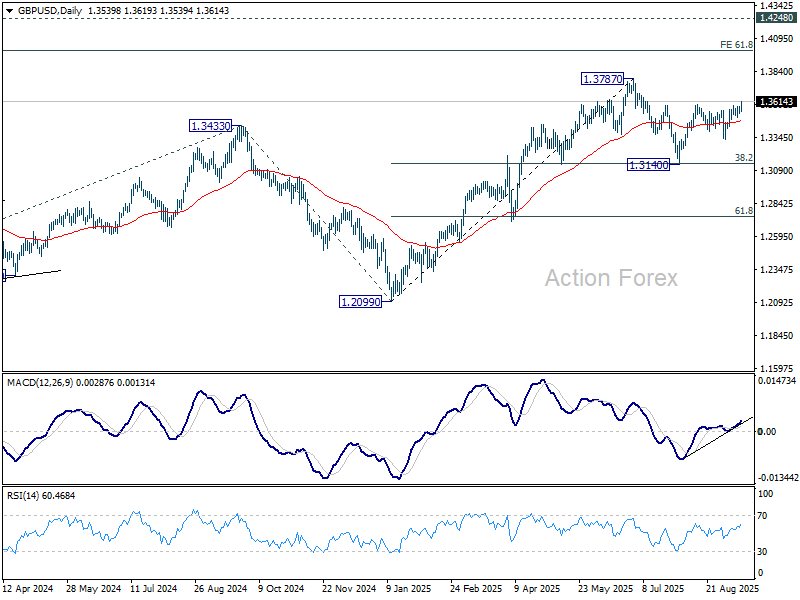

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3556; (R1) 1.3587; More…

GBP/USD’s rally from 1.3140 resumed by breaking through 1.3594 and intraday bias is back on the upside. Further rise should be seen to retest 1.3787 high. Decisive break there will resume larger up trend to 1.4004 projection level. On the downside, below 1.3523 support will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

{kind=link}