The New Zealand Dollar fell across the board after the RBNZ surprised some with a 50bps rate cut and adopted an even more dovish tone than markets anticipated. The cut itself was not a shock—markets had speculated for weeks that a half-point move was possible—but positioning in the lead-up helped amplify the reaction.

Some traders had pared back expectations earlier in the week after the NZIER shadow board recommended only a 25bps reduction. The mismatch between those softer expectations and the RBNZ’s decision sparked a knee-jerk selloff in the Kiwi, pushing NZD/USD to new multi-month lows.

Several major banks quickly shifted expectations. Westpac now forecasts a follow-up 25 bps cut in November, taking the OCR to 2.25%, and ANZ echoed that view.

Despite the Kiwi’s sharp losses, the Japanese Yen remained the weakest performer for the week, still weighed down by optimism surrounding Sanae Takaichi’s victory to become Japan’s next prime minister. Traders increasingly believe her preference for monetary accommodation will encourage the BoJ to delay any further rate hikes until next year.

Euro also stayed under pressure, hurt by the deepening political crisis in France. Outgoing prime minister Sébastien Lecornu is making a last-minute attempt to forge cross-party cooperation after his short-lived government collapsed. He is due to meet with the socialists, greens, and communists on Wednesday in an effort to break the deadlock.

Meanwhile, President Emmanuel Macron faces growing pressure even from former allies to resolve the crisis quickly. Calls for him to resign or call early elections are mounting after his first prime minister urged him to step down for the good of the country.

The currency leaderboard now shows Yen, Kiwi, and Euro as the week’s weakest performers. By contrast, Dollar leads gains, extending its advance with stronger momentum. Loonie ranks second-strongest, helped by a more constructive trade backdrop, while is also firm. Sterling and Swiss Franc are mid-range.

On the trade front, U.S. President Donald Trump struck a conciliatory tone toward Canada, promising to “treat Canada fairly” in ongoing negotiations over U.S. tariffs. After meeting Prime Minister Mark Carney, both sides described the discussions as positive and substantive, though Canadian Trade Minister Dominic LeBlanc said a final deal remained out of reach. “We have momentum now that we didn’t have this morning,” he told reporters, signaling cautious optimism without declaring victory.

In Asia, at the time of writing, Nikkei is down -0.30%. Hong Kong HSI is down -0.86%. China is still on holiday. Singapore Strait Times is down -0.47%. Japan 10-year JGB yield is up 0.019 at 1.700. Overnight, DOW fell -0.20%. S&P 500 fell -0.38%. NASDAQ fell -0.67%. 10-year yield fell -0.035 to 4.127.

RBNZ delivers 50bps cut, signals readiness to ease further if needed

RBNZ delivered a larger 50 bps rate cut, lowering the Official Cash Rate (OCR) to 2.50% at today’s meeting. The central bank maintained its easing bias, saying it “remains open to further reductions in the OCR” to ensure inflation returns sustainably to 2% over the medium term.

Minutes of the meeting showed the Monetary Policy Committee debated between a 25bps and 50bps move, with the majority favoring a bolder step to mitigate downside risks to medium-term growth and inflation. The Committee judged that prolonged spare capacity warranted a “clear signal” to support consumption and investment, helping anchor expectations amid a slowing economy.

While the Q2 GDP contraction was “considerably larger than expected,” the RBNZ attributed much of the weakness to temporary seasonal factors. It expects the distortion to reverse later in the year and said it does not see the short-term softness as materially altering the broader policy outlook.

The central bank noted that it had only marginally revised down its assessment of spare capacity but acknowledged “some downside risk” to activity. Inflation is projected to converge toward the 2% midpoint in the first half of next year, supported by easing tradables inflation and gradually moderating domestic cost pressures.

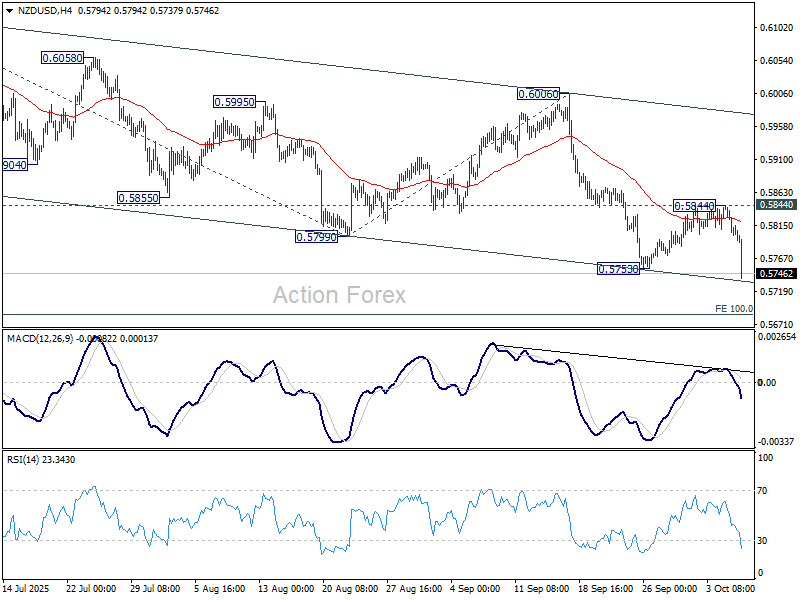

NZD/USD plunges after dovish RBNZ cut; Break below 0.5686 may accelerate losses

NZD/USD tumbled sharply after the RBNZ’s 50bps rate cut to 2.50%, with policymakers retaining an easing bias that signaled scope for further reductions ahead. The policy shift reignited downside momentum in NZD/USD, which broke through 0.5753 support, signaling a renewed leg lower in the ongoing decline from 0.6119.

Technically, near term outlook will stay bearish as long as 0.5844 resistance holds, in case of recovery. The immediate focus is on the bottom of the descending channel near 0.5730, where sustained break would likely drive NZD/USD pair through 100% projection of 0.6119 to 0.5799 from 0.6006 at 0.5686.

Should sellers push beyond 0.5686, NZD/USD could see downside acceleration toward 0.5484 cluster zone, with 161.8% projection at 0.5488. That area is expected to attract strong buying interest to bring rebound. But until then, the path of least resistance remains to the downside.

Fed’s Miran says drop in neutral rate increases tightness of policy

Fed Governor Stephen Miran said overnight that the neutral rate of interest has likely declined relative to a year ago, making current policy settings “more restrictive than a couple quarters ago.”

Speaking at a conference, Miran warned that such “additional tightness” could pose risks ahead, as the lagged effects of monetary policy start to feed through the economy. While he remained upbeat about near-term conditions, he cautioned that if policy isn’t adjusted appropriately, “I do see some risks lurking there.”

He also highlighted the challenge of the ongoing U.S. government shutdown, which has deprived policymakers of critical economic data. Miran noted that private-sector indicators are not a “sufficient replacement” and expressed hope that the government will reopen before the October 28–29 FOMC meeting, allowing the Fed to make a data-informed decision.

Meanwhile, Minneapolis Fed President Neel Kashkari voiced concern that incoming data show stagflationary signals, with a slowing labor market and inflation still near 3%. He said the key uncertainty lies in whether tariff-induced price pressures will fade quickly or prove persistent, adding that it is “too soon to reach a firm conclusion.”

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1632; (P) 1.1675; (R1) 1.1701; More…

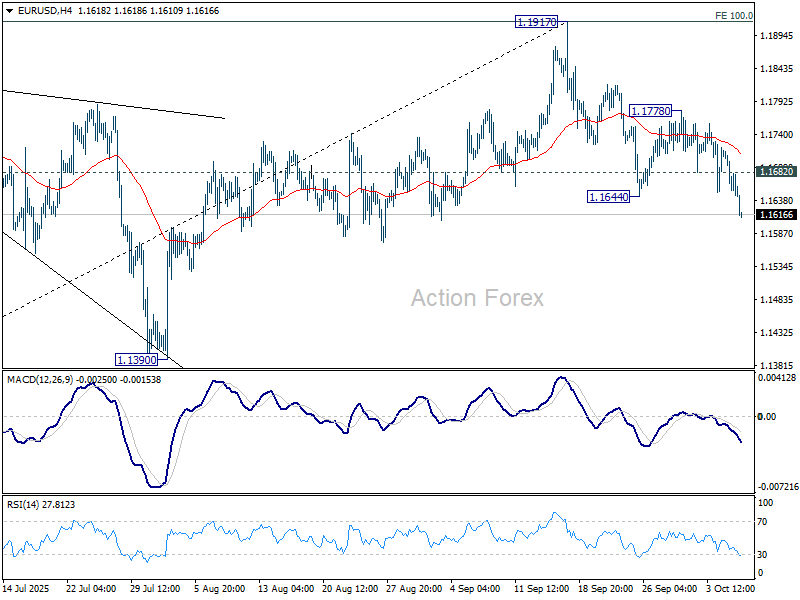

EUR/USD’s fall from 1.1917 resumed by breaking through 1.1644 and intraday bias is back on the downside. Also, the break of 55 D EMA (now at 1.1679) suggests that a medium term top was already formed on bearish divergence condition D MACD. Deeper fall should be seen to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, above 1.1682 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1778 resistance holds, in case of recovery.

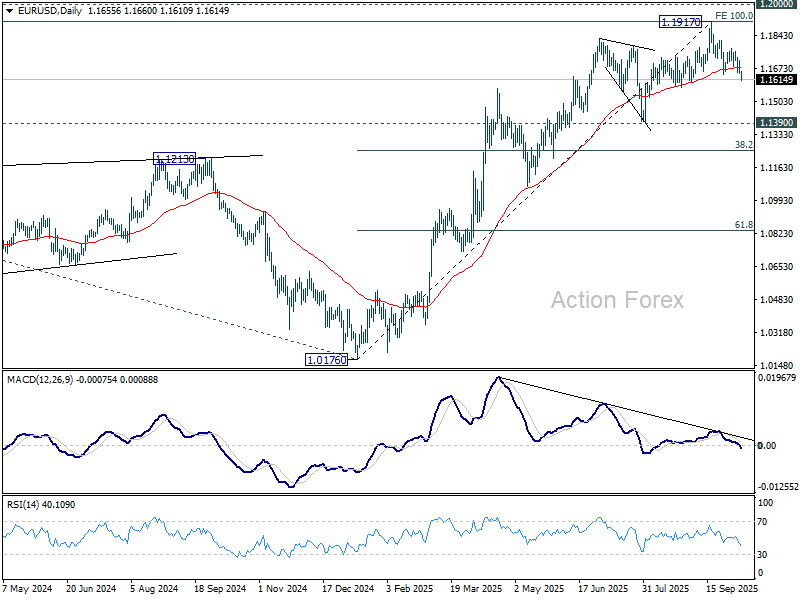

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1265) and below.

{kind=link}