Canadian Dollar climbed sharply after a blockbuster November jobs report, which easily surpassed expectations and reinforced the view that the BoC will leave policy unchanged next week. The strength of the data has effectively shut the door on the prospect of another near-term rate cut.

The BoC has already delivered 275bps of easing—one of the most aggressive responses in the G10—before signaling a pause in October. With growth likely to accelerate into year-end and the economy gradually shaking off the impact of US tariffs, markets now broadly expect the BoC to remain on hold through 2026, provided inflation remains contained.

While CAD strengthened, Dollar stayed sluggish. Although losses have moderated against European currencies and the Yen, Dollar continues to underperform as markets look past backward-looking data and focus on next week’s FOMC decision.

September PCE offered little fresh insight. The numbers came in largely as expected and did nothing to alter the dominant view that the Fed will deliver a 25bps cut in a risk-management move. The data simply confirmed the slow cooling pattern already well understood by policymakers.

The University of Michigan survey provided a clearer signal, with short- and long-term inflation expectations declining again. This four-month easing trend should help soften resistance from Fed hawks and further anchor expectations for imminent policy easing.

In currency markets, AUD leads the performance board, supported additionally by improved risk sentiment. Kiwi follows, while Sterling also trades firmer. Swiss Franc is the weakest, followed by Dollar and Euro. Yen and Loonie are positioned mid-table.

In Europe, at the time of writing, FTSE is down -0.03%. DAX is up 0.95%. CAC is up 0.11%. UK 10-year yield is up 0.12 at 4.453. Germany 10-year yield is up 0.017 at 2.793. Earlier in Asia, Nikkei fell -1.05%. Hong Kong HSI rose 0.58%. China Shanghai SSE rose 0.70%. Singapore Strait Times feel -0.08%. Japan 10-year JGB yield rose 0.011 to 1.952.

US UoM consumer sentiment jumps to 53.3, inflation expectations ease further

US consumer sentiment improved in December, with the University of Michigan headline index rising to 53.3 from 51.0, beating expectations of 52.0. The gain was driven by a sharp rise in Expectations Index, which climbed to 55.0 from 51.0. However, views on current conditions deteriorated slightly from 51.1 to 50.7.

A key development came from inflation expectations. Year-ahead inflation expectations fell for a fourth consecutive month, dropping from 4.5% to 4.1%, the lowest since January 2025—though still above the 3.3% level seen at the start of the year. Long-run inflation expectations edged down from 3.4% to 3.2%, matching the January reading.

US PCE mixed, spending softens slightly as core inflation eases

US personal income rose 0.4% mom in September, in line with expectations, while personal spending increased 0.3%, a touch below the 0.4% consensus. The combination suggests consumer demand remains resilient but is moderating gradually.

Inflation readings were broadly stable. Headline PCE rose 0.3% mom, keeping the annual rate at 2.8% yoy, slightly above August’s 2.7% but exactly matching forecasts.

Core PCE increased 0.2% mom, while the annual measure eased from 2.9% yoy to 2.8%, undershooting expectations for no change. The drop in core PCE is a mild but welcome sign for policymakers looking for continued disinflation.

Overall, the data reinforce expectations for a Fed rate cut next week, as consumption growth cools and inflation edges lower.

Canada employment jumps 53.6k in October, unemployment rate falls sharply to 6.5%

Canada’s labor market delivered a major upside surprise in November, adding 53.6k jobs versus expectations of a small -1.5k decline. The strength came almost entirely from part-time positions, which rose by 63k, offsetting a modest dip in full-time work. The gain pushed the employment rate up 0.1% to 60.9%, marking a notable stabilization after a year of softening labour momentum.

The unemployment rate dropped sharply from 6.9% to 6.5%, defying expectations for a rise to 7.0%. This reverses part of the labor market deterioration seen through most of 2025, when unemployment climbed to 7.1% in September—its highest level since 2016. The improvement suggests that labor demand remains healthier than previously believed, even in a slowing economic environment.

Wage data also supported the stronger labor picture. Average hourly earnings rose 3.6% yoy in November, up slightly from October’s 3.5% yoy, reaching CAD 37.00.

Japan household spending slumps -3.0% yoy in October, casting doubt over strength of recovery

Japan’s household spending fell sharply by -3.0% yoy in October, far below expectations for 1.1% yoy increase, and marking the steepest decline since January 2024. It was also the first annual drop in six months.

On a monthly, seasonally adjusted basis, spending plunged -3.5% mom, defying forecasts of a 0.7% mom growth. Lower outlays on food, leisure and automobile-related expenses drove the weakness, though officials said it remains unclear whether the decline represents a one-off setback, noting consumption is still perceived to be in a recovery phase.

The data arrive at a delicate moment for the BoJ. Markets have ramped up bets on a rate hike this month following recent comments from Governor Kazuo Ueda that the Bank would weigh the “pros and cons” of further tightening. The slump in spending, however, introduces fresh uncertainty around the durability of domestic demand—one of the BoJ’s key criteria for normalizing policy continuously.

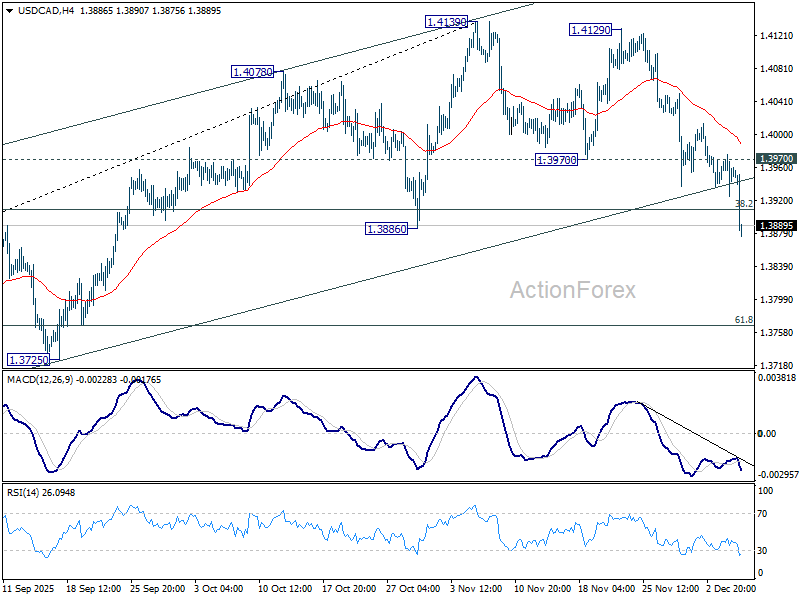

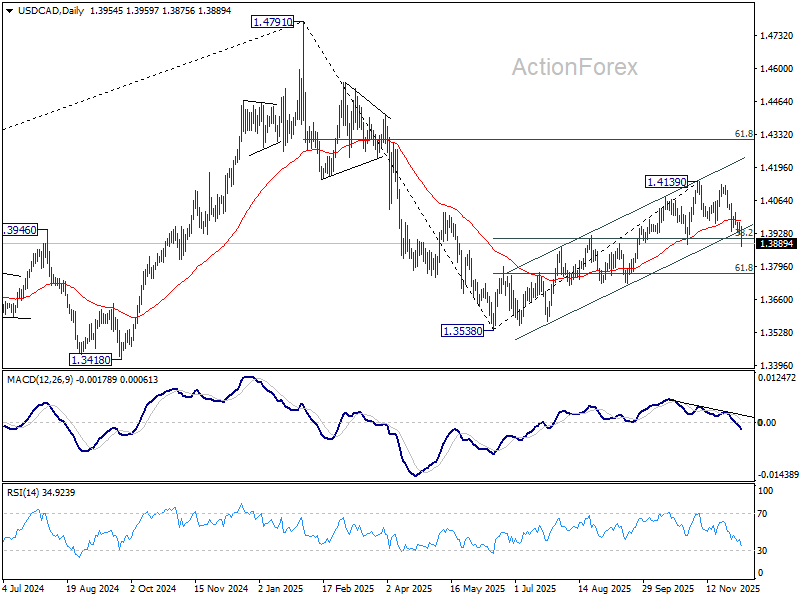

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3931; (P) 1.3954; (R1) 1.3982; More…

USD/CAD’s fall accelerate lower today and intraday bias stays on the downside. Current development argues that rise from 1.3538 has completed at 1.4139, on bearish divergence condition in D MACD. Deeper fall should be seen to 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low. For now, risk will stay on the downside as long as 1.3970 support turned resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

{kind=link}