The forex market was subdued through Asian session, mirroring the quiet tone in regional equities. With a major event risk just hours away, traders showed little appetite to adjust positioning, opting instead to wait for tonight’s high-profile FOMC rate decision.

A 25bps cut is fully priced and universally expected, leaving no suspense around the headline move. The real uncertainty lies in how the Fed shapes expectations for 2026 through its updated dot plot, the vote split, the statement, and Chair Jerome Powell’s press conference. With so many moving parts, the stakes are high and volatility is almost certain.

Adding to the broader policy backdrop is continuous attention on the next Fed Chair. The Financial Times reports that President Donald Trump will begin his final round of interviews this week, with senior administration officials indicating Kevin Hassett remains the leading candidate. The prospect of Hassett, viewed as more politically aligned and more dovish-leaning on growth risks, is seeping into market conversations.

A separate CNBC survey shows 84% of respondents believe Trump will choose Hassett, who currently heads the National Economic Council. Yet only 11% believe he should be the pick. Fed Governor Christopher Waller is the top choice among surveyed economists, with 47% support, followed by Kevin Warsh at 23%. Still, just 5% think Trump will select either of them, highlighting how little confidence markets have in an apolitical appointment.

Before the Fed lands, the BoC will deliver its own decision, with a steady hold at 2.25% widely expected. Markets now assume the BoC has entered a long pause following Governor Tiff Macklem’s October comments and the subsequent run of stronger-than-expected data. Any explicit confirmation of this stance today could lift the Loonie further, especially in crosses.

In weekly FX performance, Aussie remains the best performer so far. Kiwi follows as the second strongest, while Dollar sits in third place as traders hedge cautiously ahead of the FOMC. Yen is the weakest currency this week, followed by Loonie and then Swiss Franc, with Euro and Sterling holding mid-table positions.

In Asia, Nikkei fell -0.10%. Hong Kong HSI is up 0.21%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield fell -0.008 to 1.957. Overnight, DOW fell -0.38%. S&P 500 fell -0.09%. NASDAQ rose 0.13%. 10-year yield rose 0.014 to 4.186.

Fed Preview: If March cut odds fall tonight, Santa rally is done

FOMC rate decision is the clear centerpiece of today’s sessions, with markets fully convinced the Fed will deliver a 25bps cut to 3.50–3.75%. The probability of anything else is effectively zero, and policymakers have little incentive to risk unsettling sentiment by defying expectations at this stage of the cycle. The real debate is not about tonight’s move, but about what the Committee signals for 2026 and the broader path ahead.

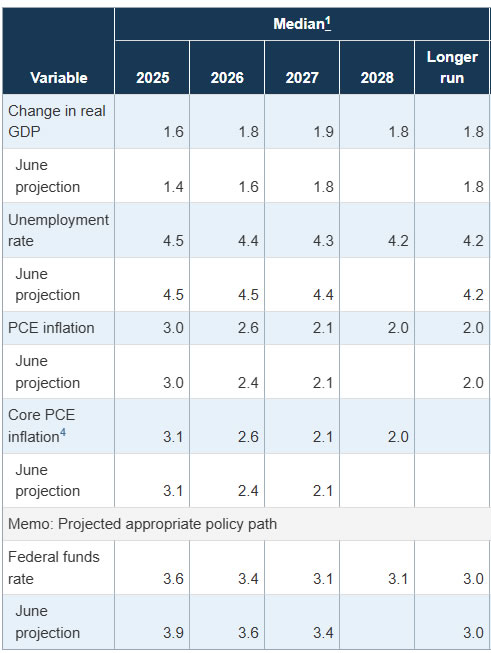

Turning back to September’s meeting, the median dot plot penciled in only one additional cut in 2026, taking the policy rate to 3.25–3.50%. A key question now is whether the Fed keeps that projection unchanged. While, that is the most likely outcome, but the dot plot itself will not reveal when that single cut is expected—whether early in the year or toward year-end. That ambiguity will shape how markets interpret tonight’s guidance.

This leads to the second major issue: whether the Fed is effectively entering a pause after today’s cut. One of the first clues will come from the vote split. A tight or divided vote would reinforce the view that the bar for further reductions is rising, and that January is likely to be another hold. The follow-through will come from the statement and Chair Jerome Powell’s press conference, where the tone will be scrutinized closely.

While all of this will ultimately be re-priced once next week’s November CPI and NFP data arrive, tonight’s communication is still critical for setting the base case for early-2026 policy expectations. Markets will be particularly sensitive to any shift in how the Fed describes labor market resilience, wage cooling, and tariff-related inflation risks.

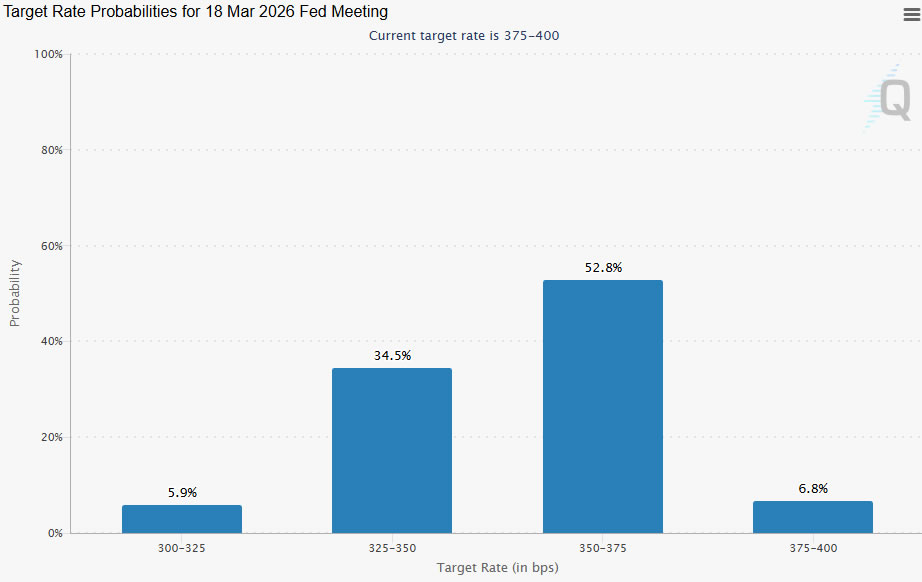

In terms of market reaction, the most important gauge is pricing for a March rate cut. Fed fund futures currently assign roughly a 40% probability of a 25bps cut in March and about a 60% probability of a hold. Any move in those probabilities—driven by dots, tone, or vote split—will dictate how equities, yields, and Dollar respond.

In stocks, a key to watch is 477560.29 support in DOW. Firm break there should indicate rejection by 48431.47 high, and the corrective pattern from there should be starting a third leg. In this case, deeper pullback would be seen to 55 D EMA (now at 46797.21) and below. Effectively, the Santa rally is killed in this case before it starts. But of course, decisive break of 48431.57 will bring another record run through to year-end.

China CPI hits 21-month high, but weak demand keeps PPI in deep negative

China’s November inflation data paint a picture of an economy showing modest signs of surface-level improvement while still grappling with entrenched deflationary pressures.

CPI accelerated from 0.2% yoy to 0.7% yoy, matching expectations and marking a 21-month high. The gain was driven primarily by food prices, which rose 0.2% yoy after a -2.9% yoy drop in October. Core inflation held steady at 1.2% yoy, while energy prices slid -3.4% yoy—an even deeper decline than the prior month.

On a monthly basis, CPI fell -0.1% mom after October’s 0.2% mom increase, contrary to expectations for another rise.

PPI slipped from –2.1% yoy to –2.2% yoy, extending China’s factory-gate deflation streak into a fourth year. Manufacturers continue to cut prices aggressively to clear excess supply, a sign that domestic and external demand remain too weak to absorb output.

Coal mining prices tumbled -11.8% yoy, while the oil and gas extraction sector saw a -10.3% yoy decline—deep drops that suggest little improvement in industrial profitability.

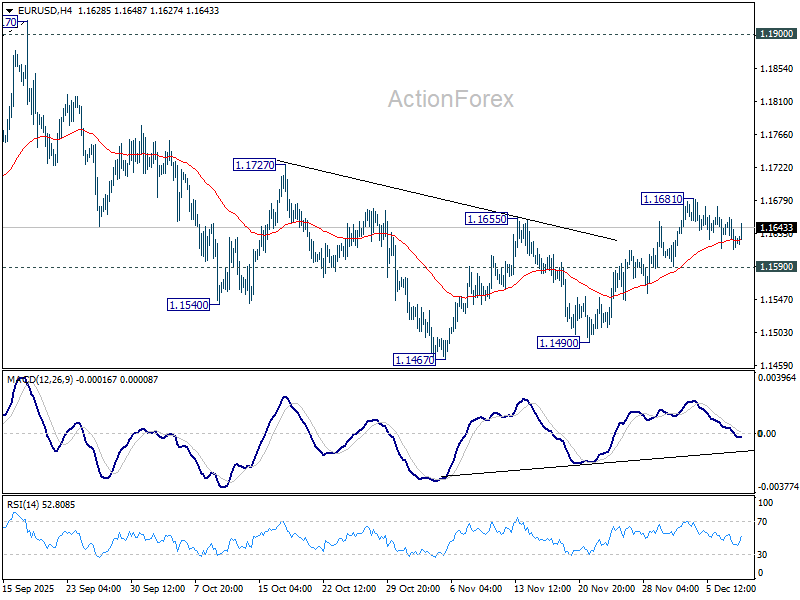

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1608; (P) 1.1633; (R1) 1.1650; More….

EUR/USD recovered after hitting 55 4H EMA but stays below 1.1681 temporary top. Intraday bias stays neutral at this point. Further rally is in favor with 1.1590 minor support intact. Corrective fall from 1.1917 could have completed at 1.1467. Above 1.1681 will target 1.1727 resistance first. Firm break there will solidify this case and bring retest of 1.1917 high. However, break of 1.1590 will revive near term bearishness, and bring retest of 1.1467 low.

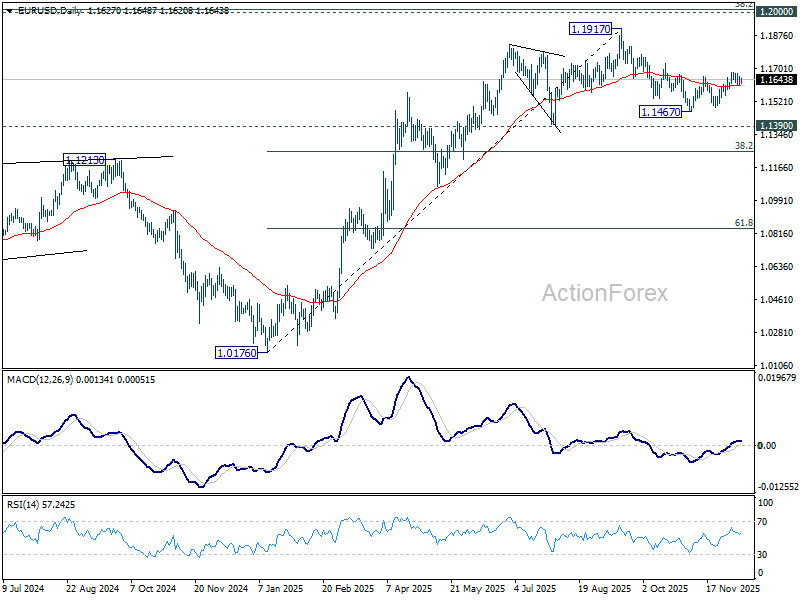

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}