Sterling edged lower after the UK GDP release disappointed again, a adding to a run of soft growth signals and left the Pound mildly on the defensive into European session. The pre-Budget weakness is strengthening the case for the BoE to resume rate cuts at next week’s meeting. While the MPC remains clearly divided, resistance to a measured easing pace looks limited. The delay from October to December was only driven by November’s Budget timing rather than a fundamental shift in the policy outlook.

A quarterly pace of cuts remains the path of least resistance for now, but beyond that the outlook is uncertain. The policy debate inside the MPC polarized, particularly around how restrictive current settings really are and how persistent inflation risks might prove in 2026. On the hawkish side, Deputy Governor Clare Lombardelli has warned this week about upside inflation risks and suggested the BoE may be nearing the end of its cutting cycle. She has also questioned how restrictive policy actually is, hinting that the room for further easing could be more limited than markets assume.

In contrast, dovish voices remain active. Deputy Governor Dave Ramsden, who argued for a rate cut in November, said he sees no evidence that inflation will fail to fall as the BoE expects. He reiterated that a gradual removal of policy restraint remains appropriate, allowing the MPC to reassess risks as new data arrive.

Elsewhere, Dollar remains broadly weak as post-FOMC softness persists, particularly against Euro and Swiss Franc. Investors appear comfortable with the Fed’s easing trajectory, a stance that has helped propel traditional stocks to fresh record highs even as debate over AI valuations lingers. Underlying risk-on sentiment continues to cap any meaningful Dollar rebound.

For the week so far, Yen sits at the bottom of the FX performance table, followed by Dollar and then Loonie. Swiss Franc leads, followed by Euro and Kiwi, while Sterling and Aussie trade in the middle of the pack.

In Asia, Nikkei rose 1.37%. Hong Kong HSI is up 1.58%. Shanghai SSE rose 0.41%. Singapore Strait Times is up 1.27%. Japan 10-year JGB yield rose 0.021 to 1.952. Overnight, DOW rose 1.34%. S&P 500 rose 0.21%. NASDAQ fell -0.25%. 10-year yield fell -0.023 to 4.141.

UK GDP contracts -0.1% mom in October as services drag deepens

UK GDP contracted by -0.1% mom in October, undershooting expectations for a 0.1% gain and marking a third consecutive month of stagnation or contraction. The economy had already shrunk by -0.1% in September after flat growth in August, reinforcing concerns that momentum is fading as the year draws to a close.

The monthly breakdown was weak across key domestic sectors. Services output fell -0.3% mom and construction declined -0.6%, offsetting a 1.1% rise in production. The continued softness in services is particularly concerning given its dominant share of UK economic activity.

On a three-month basis, GDP fell -0.1% in the period to October compared with the previous three months. Services recorded no growth, extending the recent trend of slowing activity, while production output dropped -0.5% due largely to weaker motor vehicle manufacturing. Construction also declined by -0.3%.

New Zealand BNZ manufacturing improves to 51.1, but momentum still modest

New Zealand’s BNZ Performance of Manufacturing Index edged up from 51.2 to 51.4 in November, remaining in expansionary territory but still below the long-run average of 52.4.

Production strengthened from 52.0 to 52.8, while employment rebounded sharply from contractionary 48.3 to 52.4, suggesting manufacturers are becoming more confident about staffing needs. That said, new orders softened notably, slipping from 54.5 to 51.9, highlighting lingering caution about the sustainability of demand beyond the seasonal boost.

Survey commentary was more encouraging. The share of negative comments fell to 45.6% from 54.1% in October and 60.2% in September. Respondents cited stronger Christmas-related demand, improving economic conditions, rising customer confidence, and a pickup in both domestic and overseas orders, alongside firmer construction activity and new product launches.

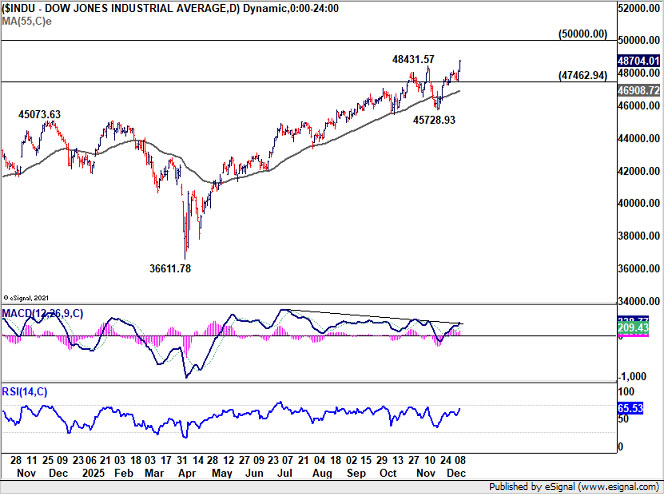

DOW eyes 50k as Fed easing fuels broad-based equity breakout, except tech

DOW decisively to a new record high yesterday, reinforcing the view that the Santa rally is firmly in force after clearly this week’s FOMC risk. With momentum accelerating, the index is now on track to challenge the 50,000 psychological level before year-end, a milestone that reflects renewed confidence in the outlook for growth and monetary policy.

Markets have looked past persistent debate over AI valuations, focusing instead on the Fed’s less-hawkish-than-expected rate cut earlier this week. The shift has favored cyclical and traditional sectors. Russell 2000’s surge to a record close adds further confirmation. Smaller companies are typically more sensitive to changes in borrowing costs, and their leadership highlights expectations that easing financial conditions will filter through to the real economy.

Technically, near-term outlook for DOW remains bullish as long as 47,462.94 support holds. The current uptrend is targeting 78.6% projection of 28,660.94 to 45,071.29 from 36,611.78 at 49,510.32, with scope to stretch above 50,000 handle. Attention now turns to whether S&P 500 joins the breakout to confirm momentum, even as NASDAQ’s participation remains less certain.

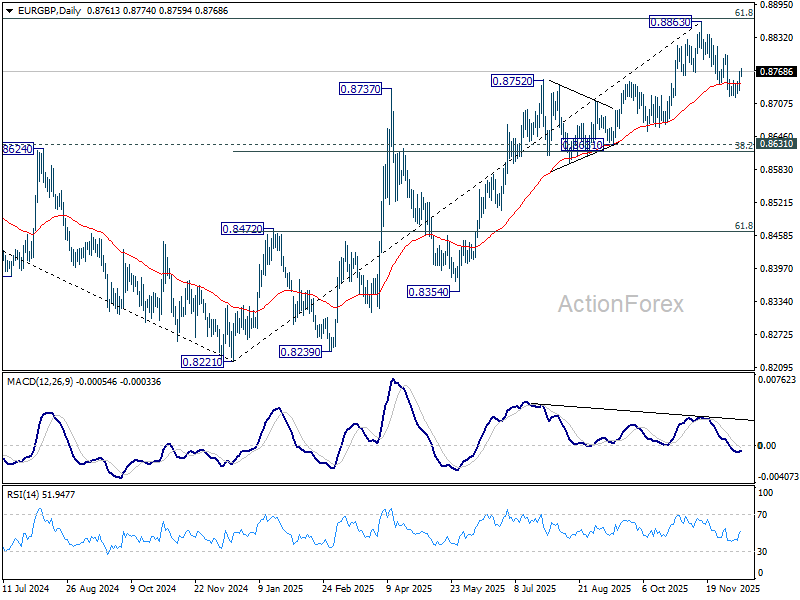

EUR/GBP Daily Outlook

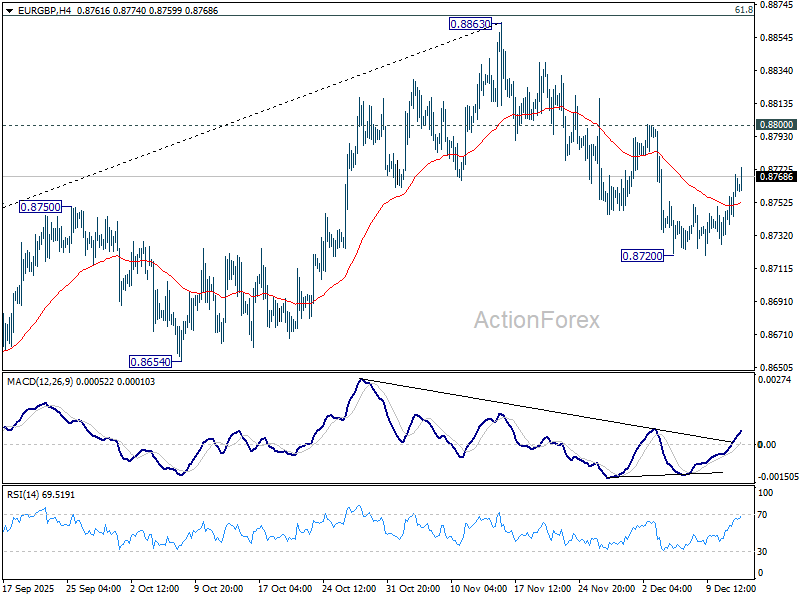

Daily Pivots: (S1) 0.8745; (P) 0.8759; (R1) 0.8783; More…

EUR/GBP’s recovery from 0.8720 extends higher today but stays below 0.8800 resistance. Intraday bias remains neutral for the moment, and further decline is still expected. Fall from 0.8863 should at least be a correction to the up trend from 0.8221, with risk of bearish reversal. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8800 will turn bias back to the upside for retesting 0.8863.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

{kind=link}