Dollar edged modestly higher into the final US session of the week, though follow-through remains limited. The rebound looks more like position adjustment than conviction, with markets reluctant to chase the greenback ahead of next week’s key data.

Attention briefly turned to fresh remarks from two Fed officials who dissented against this week’s 25bps rate cut. Chicago Fed President Austan Goolsbee struck a relatively measured tone, stressing a preference to wait for more inflation data before easing further rather than opposing cuts outright. By contrast, Kansas City Fed President Jeffrey Schmid reiterated a firmer stance, arguing policy before the cut was already appropriate and not overly restrictive.

Despite the hawkish pushback, market reaction was muted. Investors appear comfortable with the Fed’s current trajectory, seeing the dissent as part of an ongoing internal debate rather than a signal of an imminent policy shift. A January pause remains the base case, while pricing for a March cut still sits close to a coin toss.

In weekly FX performance, Yen remains pinned to the bottom, followed by Dollar. Sterling slipped to third weakest after today’s UK GDP disappointment. Swiss Franc leads after the SNB signaled earlier in the week no urgency to return to negative rates, with Euro second-best and Kiwi following. Loonie and Aussie remain stuck in the middle.

That distribution reflects a mixed but balanced risk backdrop. Traditional US stocks continue to draw support from expectations of extended Fed easing into next year, while tech shares remain capped by lingering AI valuation concerns, keeping overall sentiment from tilting decisively in either direction.

In Europe, at the time of writing, FTSE is down -0.06%. DAX is up 0.24%. CAC is up 0.62%. UK 10-year yield is up 0.002 at 4.514. Germany 10-year yield is up 0.021 at 2.868. Earlier in Asia, Nikkei rose 1.37%. Hong Kong HSI rose 1.75%. China Shanghai SSE rose 0.41%. Singapore Strait Times rose 1.45%. Japan 10-year JGB yield rose 0.024 to 1.955.

Fed’s Schmid: Policy not overly restrictive before rate cut

Kansas City Fed President Jeffrey Schmid explained his dissent at this week’s FOMC meeting, where he voted to keep rates unchanged. He said in a statement his assessment of the economy has not shifted meaningfully since October, citing “continued momentum” in activity and inflation that remains above comfort levels.

Schmid described inflation as “too high” and the labor market as cooling but still “largely in balance.” In that context, his preference is to maintain monetary policy in a “modestly restrictive” setting rather than ease prematurely.

Addressing debate around policy restrictiveness, Schmid downplayed reliance on theoretical estimates of the neutral rate, calling r* an academic concept without a real-world equivalent. Instead, he said policy should be judged by “how the economy actually evolves”. From both incoming data and business contacts, he sees an economy that is “showing momentum and inflation that is too hot”, suggesting that policy is “not overly restrictive”.

Fed’s Goolsbee: Waiting for more data the “wiser choice”

Chicago Fed President Austan Goolsbee explained his dissent at this week’s FOMC meeting, where he voted to hold rates rather than support the 25bps cut. He said policymakers should have waited for more incoming data, particularly on inflation, arguing that delaying the decision into the new year “would not have entailed much additional risk” and would have allowed the Fed to assess a more complete set of economic readings.

In a statement, Goolsbee noted that feedback from businesses and consumers in his district consistently points to prices as “a main concern”. At the same time, he described the broader economy as showing stable growth, with a labor market that is “only moderately cooling”. He characterized the current environment as one of “low hiring, low firing,” suggesting firms are responding to uncertainty rather than a traditional cyclical slowdown.

While acknowledging that recent inflation pressures may be linked largely to tariffs and could ultimately prove “transitory”, Goolsbee cautioned against assuming that outcome too quickly. He reiterated optimism that interest rates can fall meaningfully over the coming year, but stressed discomfort with heavily front-loading cuts.

UK GDP contracts -0.1% mom in October as services drag deepens

UK GDP contracted by -0.1% mom in October, undershooting expectations for a 0.1% gain and marking a third consecutive month of stagnation or contraction. The economy had already shrunk by -0.1% in September after flat growth in August, reinforcing concerns that momentum is fading as the year draws to a close.

The monthly breakdown was weak across key domestic sectors. Services output fell -0.3% mom and construction declined -0.6%, offsetting a 1.1% rise in production. The continued softness in services is particularly concerning given its dominant share of UK economic activity.

On a three-month basis, GDP fell -0.1% in the period to October compared with the previous three months. Services recorded no growth, extending the recent trend of slowing activity, while production output dropped -0.5% due largely to weaker motor vehicle manufacturing. Construction also declined by -0.3%.

New Zealand BNZ manufacturing improves to 51.1, but momentum still modest

New Zealand’s BNZ Performance of Manufacturing Index edged up from 51.2 to 51.4 in November, remaining in expansionary territory but still below the long-run average of 52.4.

Production strengthened from 52.0 to 52.8, while employment rebounded sharply from contractionary 48.3 to 52.4, suggesting manufacturers are becoming more confident about staffing needs. That said, new orders softened notably, slipping from 54.5 to 51.9, highlighting lingering caution about the sustainability of demand beyond the seasonal boost.

Survey commentary was more encouraging. The share of negative comments fell to 45.6% from 54.1% in October and 60.2% in September. Respondents cited stronger Christmas-related demand, improving economic conditions, rising customer confidence, and a pickup in both domestic and overseas orders, alongside firmer construction activity and new product launches.

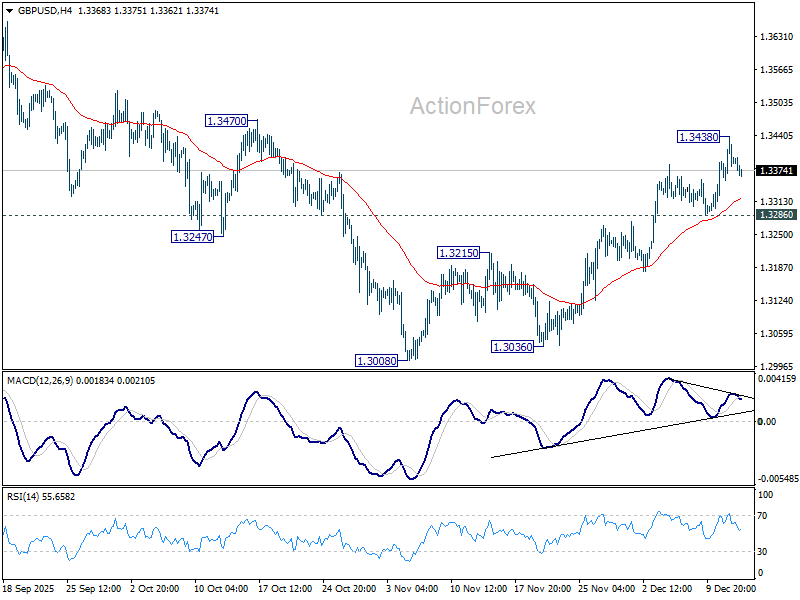

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3349; (P) 1.3393; (R1) 1.3432; More…

Intraday bias in GBP/USD is turned neutral with current retreat, and some consolidations would be seen below 1.3438 temporary top. But further rally is expected with 1.3286 support intact. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3438 will target 1.3470 resistance. Firm break there will pave the way to retest 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

{kind=link}