Dollar is under broad pressure today as markets return from Monday’s U.S. holiday with persistent focus on geopolitical risk. The move comes along with sharp rise in 10-year Treasury yield, which pushed above 4.27%, extending last week’s decisive break above the 4.2% threshold after nearly a month of failed attempts. Momentum now looks firmly skewed toward a test of 4.3%. At the same time, U.S. equity futures are broadly lower, pointing to a sharp downside open later in the session.

The combination of higher yields and falling stocks is not providing any support to Dollar, reinforcing the view that the market is questioning U.S. policy credibility rather than simply repricing rates. The selloff in the greenback has indeed accelerated through Asian and early European sessions. The combination revived talks that “Sell America” trade is finally gaining traction, reviving memories of the post-“Liberation Day” selloff last April.

At the center, US President Donald Trump has reignited trade tensions with Europe amid the Greenland dispute. The renewed tariff threats have reopened the debate over whether global investors should reduce U.S. exposure. The European Union has several response options. Beyond traditional retaliation, Brussels could activate the Anti-Coercion Instrument, an untested but far-reaching framework that allows restrictions on public tenders, investment access, banking activity, and trade in services. Its potential use is seen as a major escalation risk.

This matters because Europe is the United States’ largest external creditor, holding roughly US 8 trillion in U.S. equities and bonds, nearly twice the rest of the world combined. The key question is not whether Europe can sell, but what would push large institutional investors to start reducing U.S. exposure in size.

Tensions escalated further on Tuesday when Trump threatened 200% tariffs on French wines and champagne after President Emmanuel Macron was reported to be unwilling to join a proposed “Board of Peace” on Gaza. The remarks added a personal dimension to the dispute. Macron’s term runs until May 2027, with no option for re-election, but markets focused less on French domestic politics and more on the precedent of tariffs used as political coercion between allies.

At the same time, Yen selling is accelerating again, driven by a sharp repricing in Japan’s bond market. The 40-year JGB yield hit a record 4%, while the 10-year yield jumped above 2.3%, hitting the highest level since 1999. The moves followed Japanese Prime Minister Sanae Takaichi’s announcement of a February 8 snap election, reigniting fiscal concerns. Ultra-long yields are being pushed higher by both structural supply-demand imbalances and a renewed rise in term and risk premium as markets absorb a more expansionary fiscal stance alongside persistent inflation. This has revived the classic “Takaichi trade”.

On the FX scoreboard so far today, Yen is the worst performer, followed closely by Dollar, with both under heavy pressure. Loonie is the third weakest. At the other end, Kiwi leads gains, followed by Aussie and Euro, while Sterling and Swiss Franc sit in the middle of the pack.

In Asia, Nikkei fell -1.11%. Hong Kong HSI is down -0.25%. China Shanghai SSE fell -0.01%. Singapore Strait Times is down -0.12%. Japan 10-year JGB yield rose 0.082 to 2.353.

UK payrolled employment falls -43k, wage growth gradually eases

UK labor market data showed further signs of cooling in December, led by outright job losses. Payrolled employment fell by -43k (-0.1% m/m), while the claimant count rose by 17.9k, pointing to softening hiring demand as growth momentum slows.

Wage dynamics were mixed but continued to ease on a broader trend basis. Median monthly pay growth rose to 4.0% yoy from yoy, though this follows a sharp deceleration from levels well above 5% seen through mid-2025.

In the three months to November, unemployment rate was unchanged at 5.1%, suggesting labour slack is building only gradually. Meanwhile, average earnings including bonuses slowed to 4.7% yoy from 4.8%, while earnings excluding bonuses eased to 4.5% from 4.6%.

China keeps LPRs steady as policy shifts to structural support

The PBoC kept its benchmark lending rates unchanged, leaving the 1-year loan prime rate at 3.0% and the 5-year LPR at 3.5%. The decision was widely expected and reinforces the view that Beijing remains reluctant to deploy broad-based monetary easing despite slowing growth.

The policy stance reflects a clear preference for targeted support over headline rate cuts. The 1-year LPR continues to guide most corporate and household loans, while the 5-year rate anchors mortgage pricing. By holding both steady, authorities are signaling concern over financial stability and capital outflows, while relying on alternative tools to stimulate demand where needed.

Instead, the PBOC has intensified the use of structural monetary policy instruments. Last week, it cut rates on key relending facilities by 25bp, lowering the 1-year relending rate for agriculture and small businesses to 1.25%, effective Monday. By reducing the cost of central bank funding to banks, the PBOC aims to encourage cheaper credit for targeted sectors without reopening the door to broad leverage expansion.

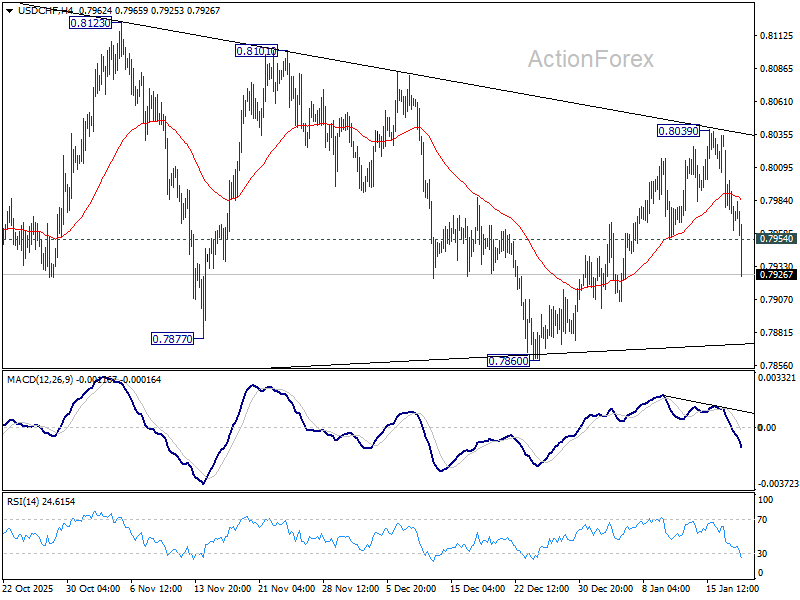

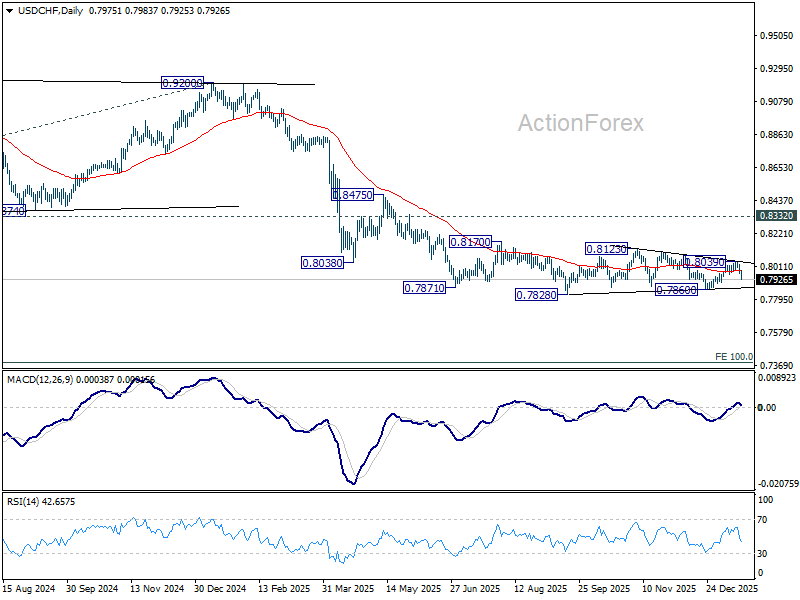

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7951; (P) 0.7987; (R1) 0.8012; More….

USD/CHF’s fall from 0.8039 accelerates lower today and the break of 0.7954 support confirms that rebound from 0.7860 has completed. Intraday bias is back on the downside for 0.7860 support. Firm break there will argue that larger down trend is ready to resume through 0.7828 low. For now, risk will stay on the downside as long as 55 4H EMA (now at 0.7984) holds, in case of recovery.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

{kind=link}