The forex market has finally slipped into a period of stabilization, with Dollar shifting into consolidation after several volatile sessions. All major pairs and crosses are trading within yesterday’s ranges, signaling a collective pause. Part of the calm reflects a temporary cooling in geopolitical and trade-war rhetoric. Recent fears of an imminent joint US–Japan intervention to support the Yen have faded. At the same time, broader trade tensions appear contained for now.

Attention is also shifting to tomorrow’s FOMC rate decision. With little fresh macro impetus elsewhere, markets appear content to wait on guidance from policymakers rather than force directional moves prematurely. There is little doubt about the outcome itself. The Fed is universally expected to keep rates unchanged at 3.50–3.75%, making this meeting more about communication than action.

As such, focus will fall on the policy statement and Chair Jerome Powell’s press conference. With the outlook still clouded by political and trade uncertainty, expectations for dramatic shifts in tone remain low. The most likely outcome is a reaffirmation of a wait-and-see approach, emphasizing data dependence and flexibility. Policymakers have little incentive to pre-commit in an environment where fiscal, trade, and geopolitical risks remain fluid.

Still, subtle nuances could matter. The Fed may seek to reassure markets that the current hold is merely a pause within an easing cycle, awaiting clearer confirmation before delivering another cut. Alternatively, though less likely, the messaging could evolve toward a more open-ended pause, dropping any implicit bias toward future easing. The distinction is small on paper, but meaningful for market expectations and forward pricing.

On the trade front, fresh headlines reminded markets that policy risk has not disappeared. US President Donald Trump threatened to raise tariffs on South Korean exports to 25% from 15%, citing delays in Seoul’s parliament approving a bilateral trade framework agreed last year. South Korea moved quickly to respond. A spokesperson for the ruling Democratic Party said Trump was likely referring to legislation linked to the USD 350 billion investment commitment to the US, adding that multiple related bills are already under review and likely to pass with bipartisan support.

Elsewhere, trade developments offered a more constructive signal. Prime Minister Narendra Modi announced that India and the EU had finalized a “landmark” free trade agreement, with details expected to be unveiled later alongside President Ursula von der Leyen. The deal would link economies representing roughly a quarter of global GDP.

In currency markets, Yen remains the strongest performer for the week, though momentum has started to fade. Swiss Franc follows, with Aussie also holding firm. Loonie is the weakest, weighed down by trade concerns, followed by Dollar and Sterling, while Euro and Kiwi sit in the middle.

Australia NAB business survey reinforces solid backdrop for RBA

Australia’s NAB business survey showed a modest but broad-based improvement in December, pointing to resilient momentum into year-end. Business Confidence edged up from 2 to 3, while Business Conditions rose from 7 to 9.

The details underline that improvement. Trading conditions climbed from 13 to 16, while profitability rose from 4 to 7. Employment conditions were unchanged at 4, suggesting hiring demand remains steady rather than accelerating. Capacity utilisation eased slightly to 83.2%, down from its recent peak but still well above its long-run average.

Cost pressures also edged higher, with purchase costs rising from 1.3% to 1.4% in quarterly equivalent terms, labour costs from 1.5% to 1.8%, and product prices from 0.6% to 0.9%, even as retail price growth slowed to 0.4% from 0.8% in November.

Overall, the survey suggests the economy ended the year on a firm footing, with most indicators sitting modestly above late-Q3 levels. Meanwhile, NAB noted that for the RBA, the small pullback in capacity utilisation is unlikely to materially ease concerns that the economy remains close to capacity.

AUD/CAD rises to 0.95, waits on Ausssie CPI verdict for next surge

Aussie has steadied after last week’s strong advance, entering consolidation as markets brace for Q4 inflation data that could prove pivotal for RBA’s policy in the near term. With expectations firmly skewed toward a firm print, traders appear to wait for confirmation before extending long positions.

Consensus forecasts point to a renewed pickup in inflation. Headline CPI is expected to rise to 3.6%, while trimmed mean CPI is forecast at 3.2%, pushing both measures further above the RBA’s target band. The upcoming release is likely to reinforce concerns that inflation pressures remain sticky. That would make it harder for the RBA to justify an extended pause, particularly with labor market conditions showing renewed strength.

Market opinion remains divided on timing. Some see scope for a 25bp hike as early as next week, while others argue the RBA may prefer to wait another quarter to avoid premature action. Ultimately, the decision will hinge on the size and composition of the inflation print, alongside the bank’s assessment of broader economic conditions.

Technically, AUD/CAD edged higher this week and remains on upward acceleration mode as seen in D MACD. With current momentum, AUD/CAD should be on track to 161.8% projection of 0.l8902 to 0.9225 from 0.9055 at 0.9578, or even further to 200% projection at 0.9701. Outlook wil stay bullish as long as 0.9344 resistance turned support holds, in case of retreat.

In the bigger picture, last week’s strong break of 0.9375 key resistance (2024 high) should confirm that whole down trend from 0.9991 (2020 high) has completed as a correction to 0.8440 (2025 low). There is prospect for the current up trend to extend in the medium term to have a test on 0.9991 at least.

How far and how fast AUD/CAD extends will ultimately depend two factors: The pace and extent of RBA tightening; and the depth of deterioration in Canada–US trade relations.

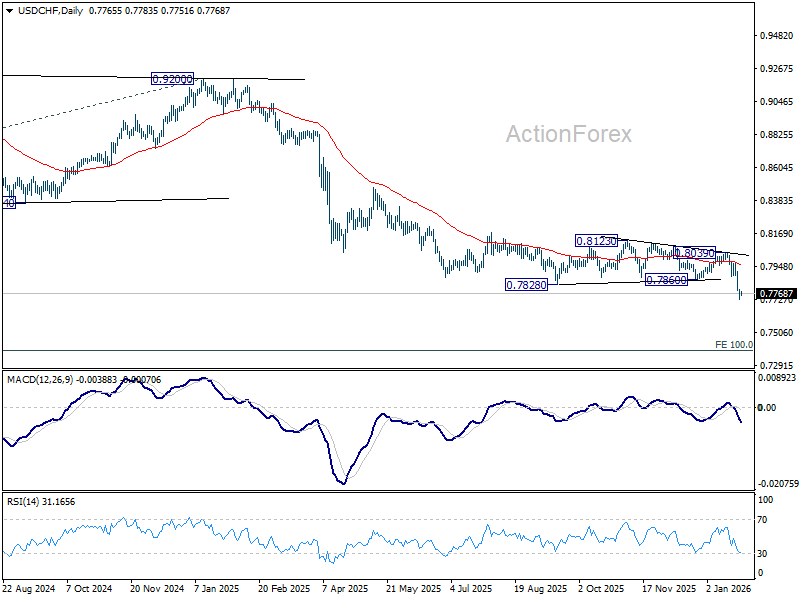

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7736; (P) 0.7765; (R1) 0.7799; More….

Intraday bias in USD/CHF is turned neutral with 4H MACD crossed above signal line, and some consolidations would be seen. But upside of recovery should be limited by 0.7860 support turned resistance. On the downside, break of 0.7729 will resume larger down trend to 0.7382 projection level.

In the bigger picture, larger down trend from 1.0342 (2017 high) is still in progress and resuming. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8184) holds.

{kind=link}