Yen is firmly back in its traditional inverse relationship with global risk sentiment. Today’s broad-based selloff in the currency moved in tandem with a powerful equity rally stretching from Asia to Europe. In Asia, the Nikkei 225 surged past 58,000 for the first time, while the KOSPI smashed through the 6,000 level in a decisive breakout. The move reflects strong tech momentum and persistent dip-buying behavior.

The strength extended into Europe. The FTSE 100, CAC 40, and Euro Stoxx 50 all hit fresh record highs, underscoring the breadth of the rally. Strong 2025 earnings from HSBC Holdings helped lift the broader European banking sector. At the same time, AI remains a tailwind. European technology stocks are benefiting from global capex optimism, with markets positioning ahead of Nvidia’s earnings due late Wednesday, seen as a key catalyst for the next leg.

Markets also appear to be shrugging off recent US tariff turbulence. While policy direction remains fluid, investors are treating trade tensions as a manageable structural factor rather than a trigger for de-risking.

For Yen, however, domestic factors are compounding the external pressure. Japan’s government nominated two academics viewed as strong stimulus advocates to the BoJ board. Toichiro Asada, a known reflationist, will replace Asahi Noguchi at the end of March, while Ayano Sato will succeed Junko Nakagawa later this year.

The shift in board composition could influence discussions around the pace and timing of further tightening. Although the BoJ is expected to continue gradual normalization, the probability of a hike in March or April has diminished. The central bank is likely to maintain its broader tightening path, but caution around timing now dominates expectations.

In FX markets, Yen is the weakest performer of the day so far, followed by Swiss Franc and Dollar. Australian Dollar leads gains on stronger CPI, though momentum was tempered by cautious remarks from RBA Governor Michele Bullock. Sterling and Kiwi follow, while Euro and Loonie sit mid-pack.

In Europe, at the time of writing, FTSE is up 1.00%. DAX is up 0.41%. CAC is up 0.42%. UK 10-year yield is up 0.031 at 4.335. Germany 10-year yield is up 0.011 at 2.721. Earlier in Asia, Nikkei rose 2.20%. Hong Kong HSI rose 0.66%. China Shanghai SSE rose 0.72%. Singapore Strait Times fell -0.26%. Japan 10-year JGB yield rose 0.034 to 2.147.

Eurozone CPI finalized at 1.7% in January, disinflation trend continues

Eurozone CPI was finalized at 1.7% year-on-year in January, down from 2.0% in December. Core CPI, which excludes energy, food, alcohol and tobacco, was also finalized at 2.2% year-on-year, slipping from 2.3% previously.

The breakdown shows services remained the primary driver in Eurozone inflation, contributing 1.45 percentage points to the annual rate. Food, alcohol and tobacco added 0.51 percentage points, while non-energy industrial goods contributed 0.09. Energy continued to act as a drag, subtracting -0.39 percentage points from overall inflation.

Across the broader EU, CPI slowed to 2.0% from 2.3%. Inflation declined in 23 member states compared with December. France (0.4%), Denmark (0.6%), Finland and Italy (both 1.0%) recorded the lowest rates. Romania (8.5%), Slovakia (4.3%) and Estonia (3.8%) were at the top of the range. The data reinforce the narrative of broad-based disinflation, though services inflation remains relatively sticky.

RBA’s Bullock tempers post-CPI tightening bets

RBA Governor Michele Bullock struck a measured tone in a fireside chat today, saying the Australian economy and labor market remain “a little bit tight,” while inflation is “a little bit elevated” but not “taking off again”. The comments came after stronger-than-expected CPI data earlier in the day had fueled a sharp rise in rate hike expectations.

Bullock emphasized that it would take time for the RBA to determine its next move, adding that policymakers would “have to be patient” . Her remarks contrasted with the market’s earlier reaction, which had pushed the probability of a May hike from 84% to 95%, and lifted expectations of a third increase by year-end from 40% to 60%.

Following her speech, rate-sensitive markets pared gains, with traders dialing back expectations of rapid tightening.

Australia trimmed mean CPI climbs to 3.4%, RBA hike seen inevitable

Australia’s monthly CPI for January came in hotter than expected, reinforcing expectations of further tightening from the RBA. Headline inflation held unchanged at 3.8% yoy, above the 3.7% consensus and marking the joint highest reading since mid-2024.

More concerning for policymakers, trimmed mean CPI rose from 3.3% yoy to 3.4%, also exceeding forecasts and standing at its highest level since Q3 2024. Core inflation has now been at or above 3% since July 2025, remaining clearly outside the RBA’s 2–3% target band.

Housing (+6.8%), food and non-alcoholic beverages (+3.1%), recreation and culture (+3.7%), were the largest contributors to annual price pressures.

Markets had already leaned toward a May rate hike, and today’s data does little to challenge that view. Some economists argue the RBA may be “a little bit behind the curve,” risking a scenario where inflation becomes entrenched and requires more forceful tightening later. With price pressures proving persistent, another rate increase is increasingly viewed as close to inevitable.

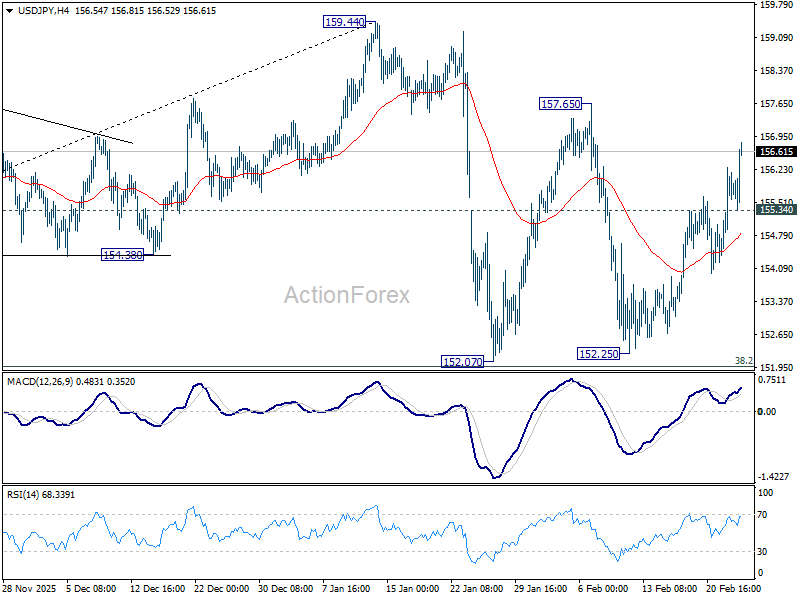

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.86; (P) 155.57; (R1) 156.61; More…

Intraday bias in USD/JPY stays on the upside as rise form 152.25 extends higher today. Firm break of 157.65 resistance will target a retest on 159.44 high. On the downside, below 155.34 minor support will turn intraday bias neutral again first. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

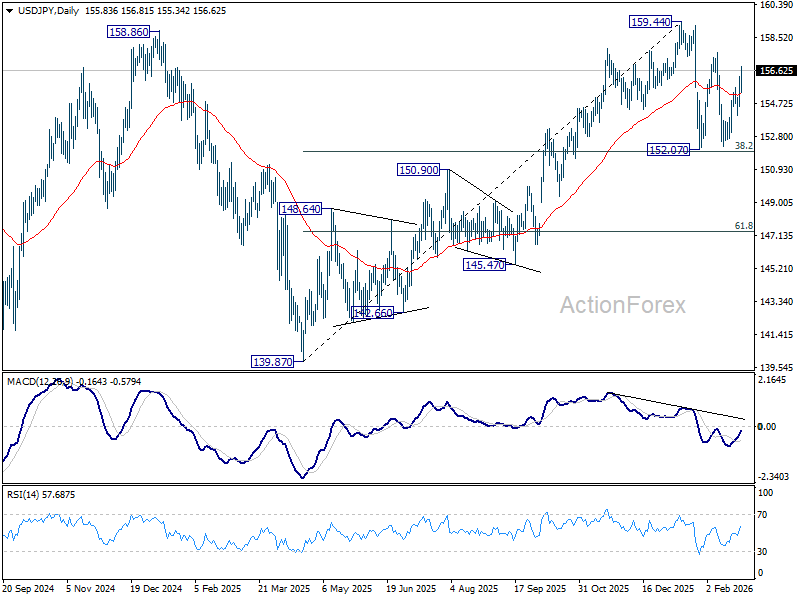

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

{kind=link}