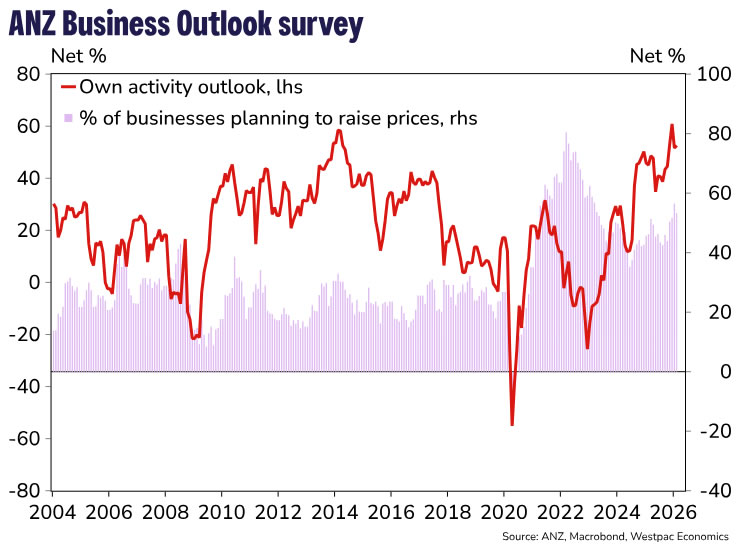

Business confidence dipped in February, though it remains at high levels. The recent signs of improvement in the economy have also come with the spectre of inflation and higher interest rates.

Key results, February 2026

- Business confidence: 59.2 (Prev: 64.1)

- Expectations for own trading activity: 52.6 (Prev: 51.6)

- Activity vs same month one year ago: 23.4 (Prev: 26.2)

- Inflation expectations: 2.93% (Prev: 2.77%)

- Pricing intentions: 53.3 (Prev: 56.5)

The ANZ business outlook survey for February showed a softening in confidence among New Zealand businesses. Given that confidence had already been running at a high level throughout 2025, the developments in the economy so far in 2026 have in a sense been unwelcome ones: signs that inflation pressures are re-emerging, and an increasingly clear message that the next move in interest rates will be up.

Confidence in the general outlook fell from 64 in January to 59 in February. Firms’ own-activity expectations did rise slightly, but the more detailed activity indicators (employment, investment, profits) were generally a bit lower.

A net 23% of firms reported that their activity was up on the same time last year. While this measure was also lower compared to February, it has largely held on to the gains that we saw in late 2025.

Perceptions about the ease of credit have fallen sharply in the last two months, and are at their lowest since July 2024. The RBNZ’s November Monetary Policy Statement, which signalled that OCR cuts were likely at an end, was followed by a sharp rise in term interest rates as the market began to consider the likely timing of rate hikes.

The inflation gauges in the survey were mixed. Expectations for inflation in the year ahead rose from 2.77% to 2.93%, the highest since July 2024. This measure typically responds to the last quarterly inflation print – in this case a higher-than-expected 3.1%yr, taking it outside the RBNZ’s target range. In contrast, firms’ own pricing intentions dropped back a little, albeit having reached a three-year high in January.

Interestingly, expected wage growth for the year ahead rose from 2.8% to 3.0%, the highest since April 2024. However, reported wage growth over the past year slowed from 2.8% to 2.5%. The wage questions are a relatively recent addition to the survey (from March 2022), so we don’t have a clear sense yet of how well they predict the official wages data. However, any evidence of rising wage pressures would be concerning for the RBNZ at this point, given its view that there will be a significant amount of slack in the labour market for some time to come.

{kind=link}