Yen recovered mildly today following hawkish comments from BoJ Governor Kazuo Ueda, who signaled that the bank will “scrutinize data” at the March and April meetings before making a rate decision. However, gains remain capped as Yen remains the week’s laggard. While Ueda explicitly put a March hike on the table, markets suspect this is a verbal intervention to prevent a swift slide toward 160, rather than a definitive policy signal. Two factors support this skepticism:

- Political Friction: The Mainichi reported that PM Sanae Takaichi personally expressed disapproval of immediate hikes to Ueda last week.

- Reflationist Reinforcements: Takaichi has nominated Toichiro Asada and Ayano Sato—both staunch reflationists—to join the board on April 1 and June 30.

Pushing a hike in March would be a massive political gamble. It would be viewed as “front-running” the new board—a preemptive strike to lock in higher rates before Takaichi’s “dovish reinforcements” can take their seats. This would set Ueda on a collision course with a PM who just secured a historic landslide mandate.

Nevertheless, Ueda’s comments still put April back as a more “diplomatic” window for the next hike. By then, Ueda can incorporate “Shunto” wage data and involve the first new member, Asada, framing the move as a data-driven consensus rather than a central bank coup.

Meanwhile, Dollar is also soft, weighed down by risk-on mood fueled by Nvidia’s blowout earnings. CEO Jensen Huang pushed back on the “AI cannibalization” narrative, arguing that AI agents will not replace enterprise software but will instead use those tools to drive a “new industrial revolution.” Equities responded positively, with focus now on whether the strong rebound in NASDAQ Composite and S&P 500 can extend into a range breakout.

Overall for the week so far, Yen remains the worst performer, following by Dollar, and then Loonie. Aussie is staying as the strongest, followed by Sterling, and then Swiss Franc. Euro and Kiwi are positioning in the middle. Overnight, DOW rose 0.63%. S&P 500 rose 0.81%. NASDAQ rose 1.26%. 10-year yield rose 0.015 to 4.048.

BoJ’s Ueda signals hike still possible in spring

BoJ Governor Kazuo Ueda signaled that a March or April rate hike remains on the table, stating in a Yomiuri interview that the central bank will continue raising interest rates if economic and price projections evolve as expected. “We will hold a policy meeting in March and April, so we would like to reach a decision by scrutinising data available by then,” he said.

Additionally, Ueda noted that the BOJ does not necessarily need to wait for the quarterly Tankan survey release on April 1 to act, as it relies on a range of business and economic indicators. He also also rejected suggestions that the BOJ is behind the curve on inflation, arguing that underlying price pressures have yet to fully reach the 2% target.

Markets had earlier pared back expectations for a near-term hike after reports that Prime Minister Sanae Takaichi expressed reservations about further rate increases. Ueda’s remarks appear to have recalibrated those bets, bringing March and April back into active consideration as the BoJ weighs the impact of December’s hike on lending, investment, and consumption.

Takata says BoJ should consider another “gear shift”

BoJ Board member Hajime Takata said in a speech that overseas risks, particularly around tariff policy, had been a key consideration when evaluating the timing of another rate increase. However, he said initial concerns over those external factors “have abated”, clearing part of the uncertainty that had previously restrained policy action.

Domestically, Takata emphasized that Japan’s long-standing “the norm of prices not increasing easily has already been dispelled”. Medium- to long-term inflation expectations have risen. Price increases now “have a greater tendency to generate second-round effects”. He also cautioned that external shocks could produce greater-than-expected price surges.

Looking ahead, Takata highlighted expectations of a fourth consecutive round of wage increases in 2026, driven largely by base pay gains. In that context, he said the BOJ should prepare for another “gear shift” in policy and communicate under the assumption that the 2% price stability target is nearly achieved.

NZ business confidence falls, wage and price expectations rise

New Zealand’s ANZ Bank Business Confidence index eased from 64.1 to 59.2 in February. However, the Own Activity Outlook edged higher from 51.6 to 52.6, suggesting firms remain broadly optimistic about their near-term operating conditions.

Beneath the surface, inflation pressures appear to be building again. The net percentage of firms expecting to raise prices over the next three months fell 4 points to 53%, partially reversing last month’s surge. Yet cost expectations remain elevated, with 79% of firms anticipating higher costs — the highest level since July 2023.

More notably, one-year inflation expectations rose from 2.77% to 2.93%, their highest level since July 2024. Wage expectations climbed above 3% for the first time since April 2024.

ANZ noted that pricing intentions are not consistent with widespread expectations of a steady decline in headline inflation this year. Although inflation is projected to return to the target band in Q1 and the RBNZ has expressed confidence in the disinflation path, the survey highlights ongoing upside risks.

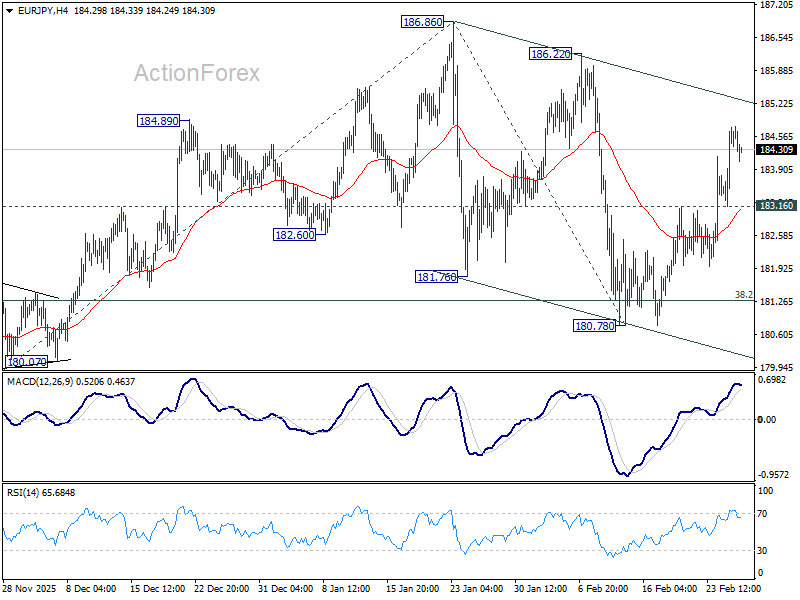

EUR/JPY Daily Outlook

Daily Pivots: (S1) 183.66; (P) 184.22; (R1) 185.24; More…

EUR/JPY’s rally from 180.78 is still in progress and intraday bias remains on the upside for 186.22/86 resistance zone. Decisive break there will confirm larger up trend resumption. Next target is 61.8% projection of 172.24 to 186.86 from 180.78 at 189.81. On the downside, below 183.16 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 38.2% retracement of 172.24 to 186.86 at 181.27, in case of deep retreat.

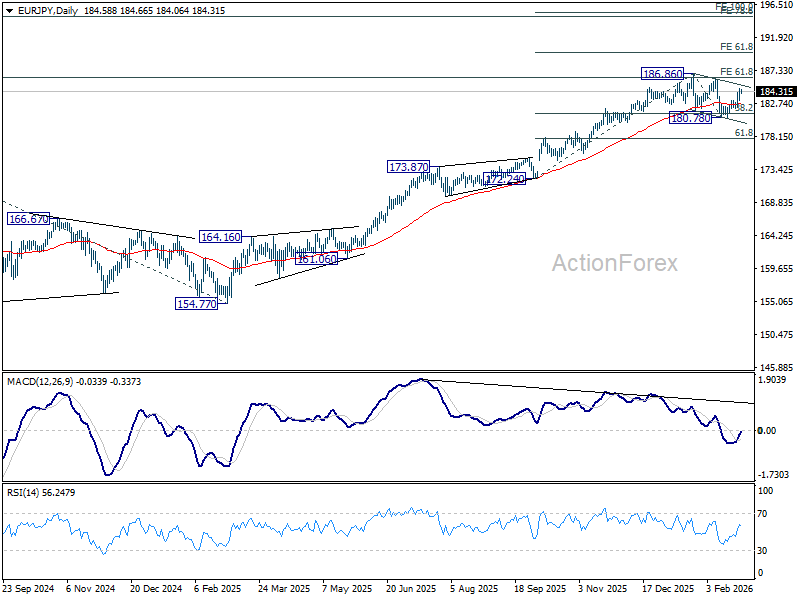

In the bigger picture, current development suggests that price actions from 186.86 are merely a near term corrective pattern. In other words, the long term up trend is still in progress. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. This will now remain the favored case as long as 180.78 support holds.

{kind=link}