The U.S. labor market remains soft with the “low fire, low hire” environment continuing. We expect payroll growth to step down to around 70K in April, with a rebound in labor force participation pushing the unemployment rate back up to 4.4%. Globally, central banks are diverging. The Fed is firmly on hold in the wake of the continued conflict in Iran. But we now expect the Reserve Bank of Australia to deliver a third consecutive rate hike, prolonging their hiking cycle, and Canada’s labor market to stabilize, supporting a July rate hike as inflation pressures return to focus. In emerging markets, we expect Banxico to cut the policy rate by 25 bps next week to 6.50%, likely in a split decision, even as inflation risks remain tilted to the upside.

United States:

- Employment (Friday)

G10 Economies:

- Reserve Bank of Australia Policy Rate (Wednesday), Canada Labor Force Survey (Friday)

Emerging Markets:

- Banxico Policy Rate (Thursday)

U.S. Week Ahead

Employment • Friday

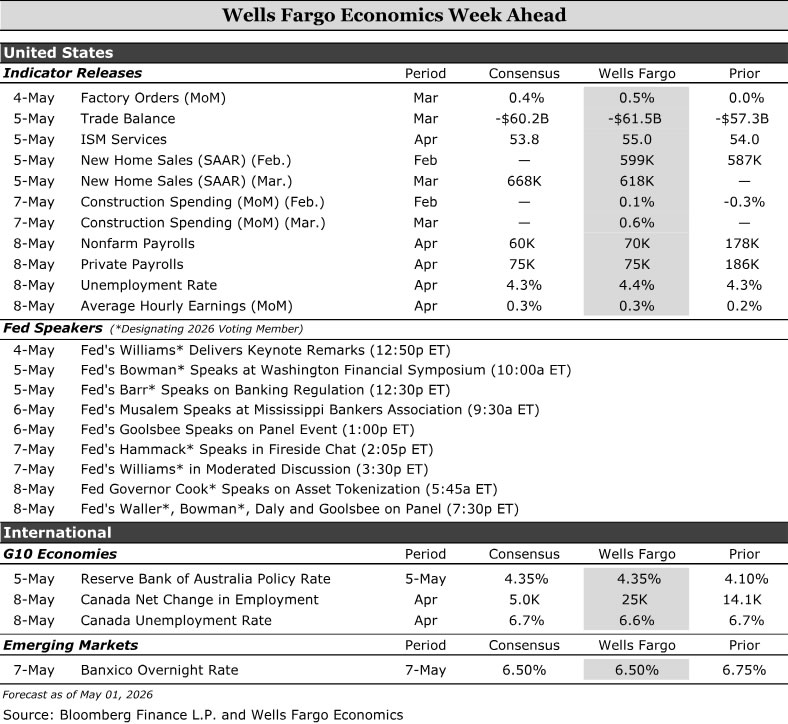

The labor market is still stuck in the low fire, low hire dynamic that has prevailed for the past two years. While layoffs at well-known tech companies made headlines in recent weeks, initial jobless claims, WARN notices and Challenger job cut announcements point to economy-wide layoffs remaining tame for now. Yet, firms still show little appetite to hire additional workers. Small business hiring plans are sitting at a two-year low, regional Fed employment PMIs sank further into negative territory in April and Indeed job postings—which had been on an upswing since the start of the year—wobbled in March.

With demand for workers little changed, the supply of workers has become a bigger factor in the pace of job growth. Last month’s 178K rise in payrolls, even accounting for the ~30K boost from completed strikes, is untenable given the immigration and demographic constraints on labor force growth. We expect some payback in April and estimate total payrolls advanced 70K, with private payrolls up 75K.

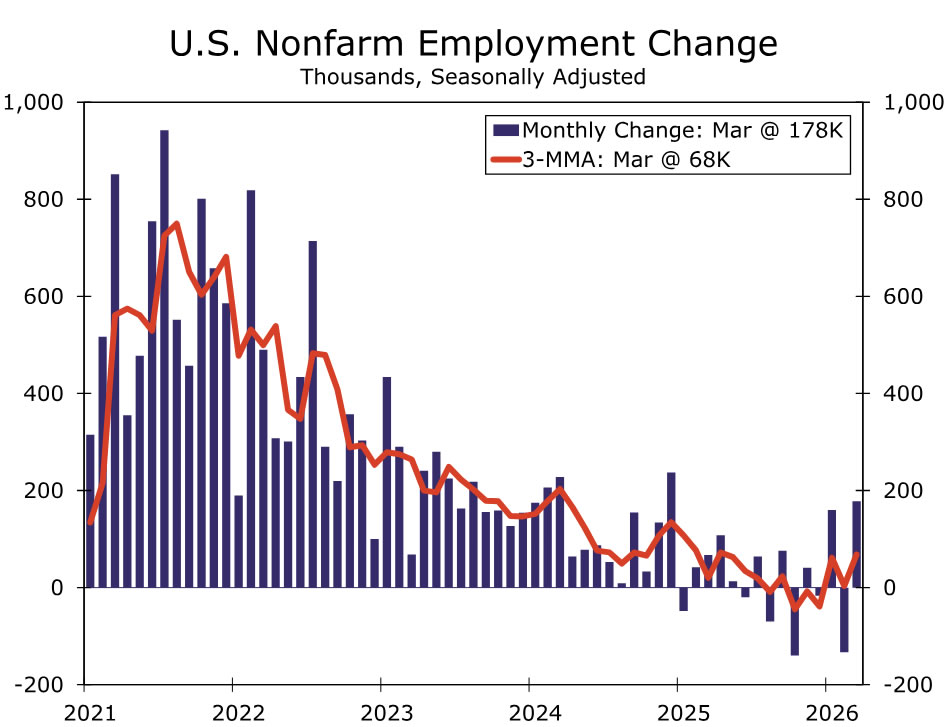

The April unemployment rate is also like to point to a slightly softer jobs market. Last month’s drop to nearly 4.2% (4.26% unrounded) was driven by a swath of unemployed workers leaving the labor force. We look for a rebound in the labor force and ranks of the unemployed in April to push the unemployment rate back to 4.4%. That would leave the unemployment a tick higher than what most FOMC members estimate is full employment—uncomfortable amid an uncertain demand backdrop, but not indicative of the labor market’s delicate balance tipping in April.

G10 Week Ahead

Reserve Bank of Australia Cash Rate • Wednesday

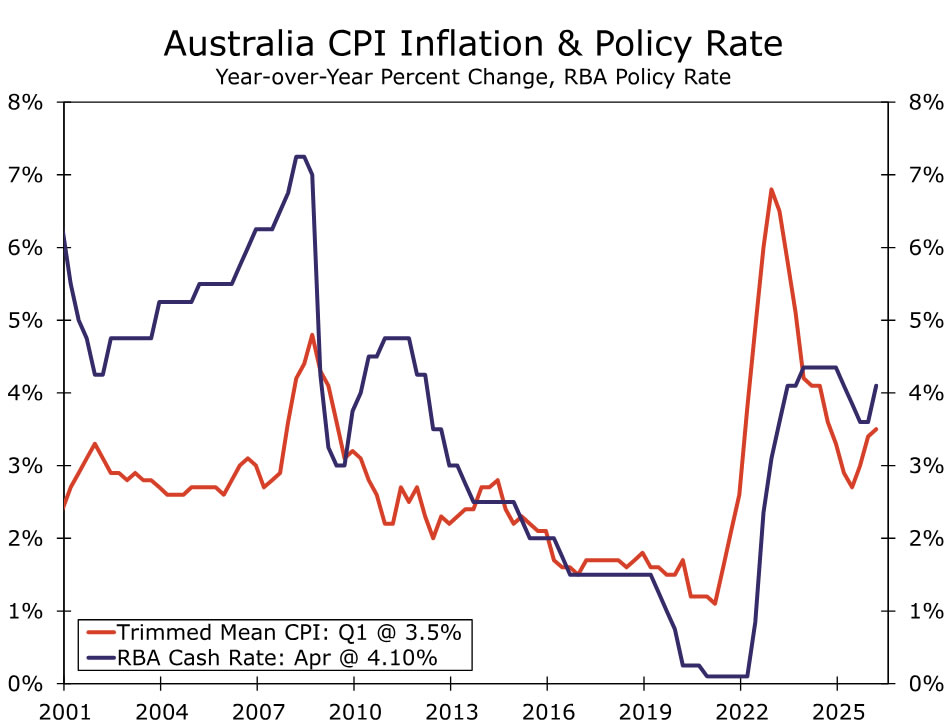

We expect a third consecutive 25 bps rate hike from the Reserve Bank of Australia (RBA) next week, lifting the Cash Rate to 4.35%. Further, we see the RBA prolonging its hiking cycle through mid-year, a shift from our prior view of rates on hold through end-2026. At its March meeting, the RBA stressed that with inflation still too high, the question of raising rates was about “timing rather than direction.” Recent communication reinforces that message, with greater emphasis on anchoring long‑term inflation expectations. Deputy Governor Hunter described this as being a central bank’s ‘North Star’, while Governor Bullock, at the March meeting, stated that anchoring long-term inflation expectations depends on convincing households and firms the RBA “would take action to bring inflation back to target.” While March headline CPI rose 4.8% year-over-year due largely to fuel prices, the print undershot expectations and trimmed mean inflation held at 3.3%, pointing to moderating core inflation before the Middle East conflict. That dynamic, however, is likely to shift over the next months, with April PMIs showing the fastest rise in input costs in over four years.

With the labor market tight, inflation above target and the economy starting from a relatively strong position, policymakers appear focused on near-term action. As this meeting includes an updated Statement on Monetary Policy, it should clarify how much higher inflation is expected to run by the RBA and what that implies for the path ahead. While the outlook beyond May is less certain after three hikes, risks have shifted to the upside. We now see scope for another increase (most likely in June but could be delayed to August), taking the Cash Rate to 4.60%, with the possibility of higher rates if the conflict continues and inflation pressures intensify.

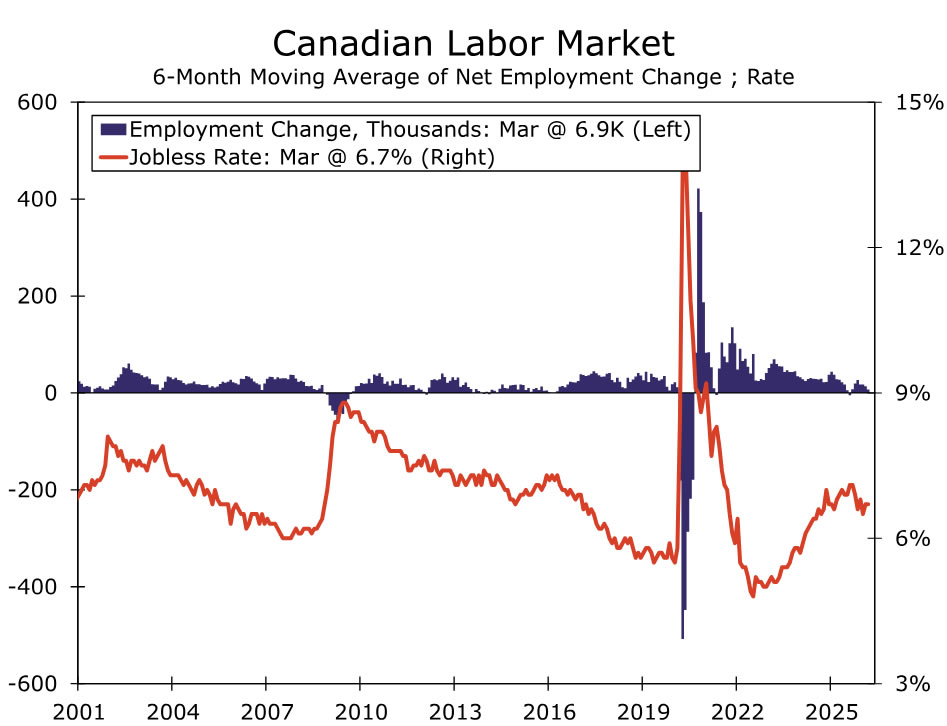

Canada Labor Force Survey • Friday

We expect further improvement in Canadian labor market data next week, with employment rising by around 25K in April and the unemployment rate ticking down to 6.6%. The April report should confirm the stabilization in labor market conditions seen in March. We expect job gains to be concentrated in full-time employment and led by goods-producing sectors, particularly energy and mining. Demographics and net migrant outflows continue to point to weak labor force growth and subdued participation rates. This is pushing down the breakeven pace of job growth needed to keep the unemployment rate stable, potentially into slightly negative territory. As a result, we expect the unemployment rate to drift gradually lower over the course of 2026.

On net, stabilization in labor market conditions shifts the balance of risks for the Bank of Canada back toward inflation. This week’s meeting emphasized USMCA-related uncertainty as a near-term dovish risk. However, we continue to expect a Bank of Canada rate hike at the July meeting, assuming the July 1 deadline passes with a muddle-through outcome, policymakers gain further evidence of inflation pass-through and the Bank delivers a refreshed July Monetary Policy Report.

EM Week Ahead

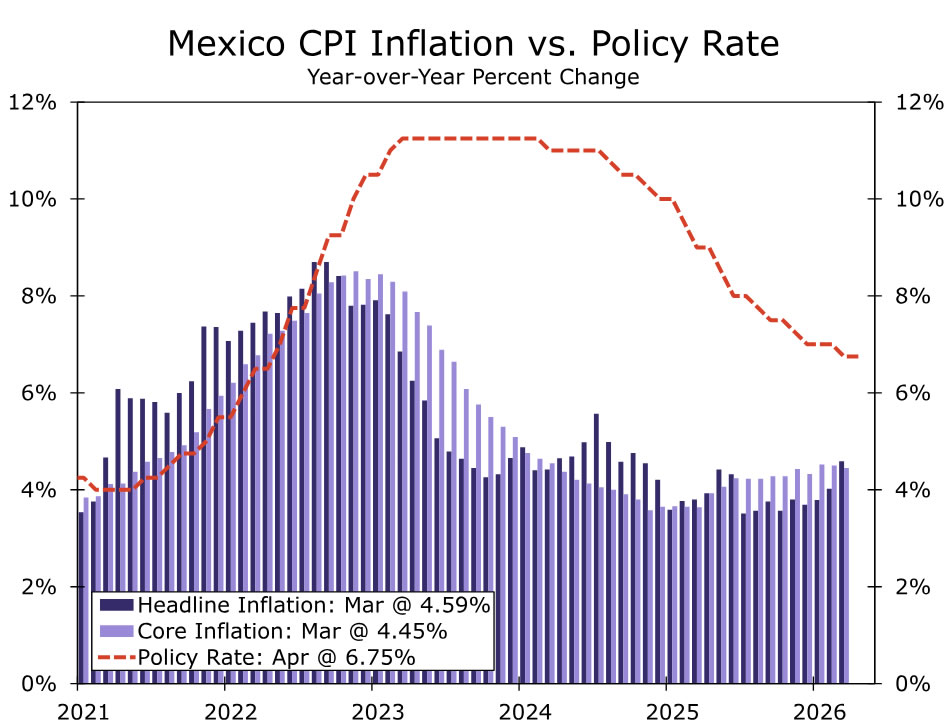

Banxico Policy Rate • Thursday

We expect Banxico to cut the policy rate by 25 bps next week to 6.50%, with the window for further easing now rapidly closing. We anticipate a 3–2 decision, with the dovish majority leaning heavily on softer activity data. Economic momentum weakened sharply in Q1, with GDP contracting 0.8% quarter-over-quarter and growth barely positive on a year-over-year basis. Retail sales, labor market indicators and downward revisions to services output all point to a loss of momentum early in the year. Q2 should improve mechanically, but this is more likely to reflect stabilization than a meaningful rebound. Inflation dynamics remain problematic. Both headline and core inflation are around 4.5% year-over-year, with core inflation having remained above 4% for nearly a year, well above the upper bound of Banxico’s 2–4% target range. Non-core inflation is likely to re-accelerate in coming months as higher food and energy prices feed through, reflecting Middle East developments and adverse agricultural conditions. Inflation risks are therefore clearly skewed to the upside, leaving Banxico’s dovish bias increasingly out of step with inflation realities.

A final rate cut in Q2 appears likely, particularly given recent comments from Governor Rodríguez and Deputy Governor Mejía. As in the March meeting, we expect Deputy Governors Borja and Heath to dissent in favor of holding rates steady. Looking beyond, the macro mix for H2 2026 is unfavorable, characterized by low trend growth, elevated inflation, limited fiscal support, and fragile monetary credibility. A key risk event later this year will be the replacement for Heath, whose term ends in December. A technocratic appointment would be viewed positively by markets and help contain risk premia in both rates and FX. Absent that, we see weak growth and Banxico’s dovish bias weighing on the peso, while credibility concerns are more likely to lift term premia in local rates.

{kind=link}