FX markets are subdued, with major pairs largely contained within recent ranges. Dollar is edging higher from earlier lows, but the move lacks follow-through amid a strong risk-on backdrop. Yen staged a mild recovery after hawkish signals from BoJ officials, yet it remains the week’s worst performer. Risk-on dynamics continue to outweigh policy rhetoric.

For the week so far, Australian Dollar still tops the board, though upside momentum has softened. The currency appears to be consolidating after its CPI-driven advance, while struggling to break decisively against the greenback. Sterling and Euro are also on the firmer side, while Kiwi and Swiss Franc trade in the middle. On the other hand, Yen, Dollar, and Loonie sit at the bottom of the leaderboard.

With no major data releases today, currencies are trading off broader risk tone and geopolitical developments, particularly the latest round of US-Iran negotiations in Geneva. Ahead of that, oil prices have dipped notably, with WTI slipping back below 65 and Brent under 70, reversing last week’s surge. The pullback reflects growing optimism that diplomacy may prevail over escalation.

The third round of US-Iran negotiations opened in Geneva. Reports from Geneva suggest Iran is showing seriousness and flexibility, potentially paving the way for at least an interim nuclear agreement. While tensions remain, investors increasingly see the probability of immediate military conflict as lower than earlier feared.

The standout story, however, is Chinese Yuan. It has reached its strongest level against Dollar since early 2023 and broken a significant technical barrier against Euro, marking its strongest level since May 2025. This is not merely a Dollar-weakness move. The appreciation is broad-based and could reflect shifting geopolitical calculations.

German Chancellor Friedrich Merz’s visit to Beijing appears to be a contributing factor. European officials have openly called for a stronger Yuan to help rebalance trade. The surge in Yuan is being read as a “calculated concession” by Beijing. By allowing the Yuan to rise, China is signaling a willingness to reduce the trade imbalance in exchange for avoiding a “two-front” trade war with both the US and the EU. Additionally, some investors anticipate the People’s Bank of China will tolerate continued appreciation into the “Two Sessions” to reinforce economic stability messaging.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.44%. CAC is up 0.89%. UK 10-year yield is down -0.023 at 4.300. Germany 10-year yield is down -0.001 at 2.709. Earlier in Asia, Nikkei rose 0.29%. Hong Kong HSI fell -1.44%. China Shanghai SSE fell -0.01%. Singapore Strait Times fell -0.87%. Japan 10-year JGB yield rose 0.01 to 2.157.

US initial jobless claims edge higher to 212k, vs exp 211k

US initial jobless claims rose 4k to 212k in the week ending February 21, slightly above expectation of 211k. Four-week moving average of initial claims rose 1k to 220k.

Continuing claims fell -31k to 1,833k in the week ending February 14. Four-week moving average of continuing claims rose 3.5k to 1,848k.

Eurozone economic sentiment moderates in February, services drag

Economic sentiment in Europe softened in February, with the Economic Sentiment Indicator falling by 1.0 point to 98.3 in both the EU and the Eurozone. The Employment Expectations Indicator also declined, slipping to 98.5 in the EU and 97.6 in the Eurozone. Both gauges remain slightly below their long-term average of 100.

The drop in the ESI was driven primarily by a marked deterioration in services confidence, while construction also contributed modestly to the decline. In contrast, sentiment in industry and among consumers was broadly stable, and retail trade confidence continued to improve, suggesting that weakness is not yet broad-based.

Among the largest EU economies, France (-2.8) recorded the sharpest fall in sentiment, followed by Poland (-1.9) and Italy (-0.6). Germany and the Netherlands (-0.2 each) saw only marginal declines, while Spain was broadly unchanged.

ECB’s Lagarde: Rising real incomes to support growth

Speaking before the European Parliament’s Committee on Economic and Monetary Affairs, ECB President Christine Lagarde said the Eurozone economy should find support from rising labor income and resilient employment. Investment in defence, infrastructure and digital transformation is also expected to underpin growth, even as the region faces higher tariffs, a stronger Euro and ongoing global policy volatility.

She pointed out that real wages growth have moved above early-2021 levels, reflecting inflation that has fallen below nominal wage gains. Although wage growth is still elevated, it is gradually moderating and expected to settle near 3% over the medium term.

Lagarde reaffirmed that the ECB sees inflation stabilizing around its 2% target. That assessment supported the decision earlier this month to keep key interest rates unchanged.

Looking ahead, she emphasized that policy will remain data-dependent and assessed meeting by meeting. “”We are not pre-committing to a particular interest rate path,” she reiterated.

BoJ’s Ueda signals hike still possible in spring

BoJ Governor Kazuo Ueda signaled that a March or April rate hike remains on the table, stating in a Yomiuri interview that the central bank will continue raising interest rates if economic and price projections evolve as expected. “We will hold a policy meeting in March and April, so we would like to reach a decision by scrutinising data available by then,” he said.

Additionally, Ueda noted that the BOJ does not necessarily need to wait for the quarterly Tankan survey release on April 1 to act, as it relies on a range of business and economic indicators. He also also rejected suggestions that the BOJ is behind the curve on inflation, arguing that underlying price pressures have yet to fully reach the 2% target.

Markets had earlier pared back expectations for a near-term hike after reports that Prime Minister Sanae Takaichi expressed reservations about further rate increases. Ueda’s remarks appear to have recalibrated those bets, bringing March and April back into active consideration as the BoJ weighs the impact of December’s hike on lending, investment, and consumption.

Takata says BoJ should consider another “gear shift”

BoJ Board member Hajime Takata said in a speech that overseas risks, particularly around tariff policy, had been a key consideration when evaluating the timing of another rate increase. However, he said initial concerns over those external factors “have abated”, clearing part of the uncertainty that had previously restrained policy action.

Domestically, Takata emphasized that Japan’s long-standing “the norm of prices not increasing easily has already been dispelled”. Medium- to long-term inflation expectations have risen. Price increases now “have a greater tendency to generate second-round effects”. He also cautioned that external shocks could produce greater-than-expected price surges.

Looking ahead, Takata highlighted expectations of a fourth consecutive round of wage increases in 2026, driven largely by base pay gains. In that context, he said the BOJ should prepare for another “gear shift” in policy and communicate under the assumption that the 2% price stability target is nearly achieved.

NZ business confidence falls, wage and price expectations rise

New Zealand’s ANZ Bank Business Confidence index eased from 64.1 to 59.2 in February. However, the Own Activity Outlook edged higher from 51.6 to 52.6, suggesting firms remain broadly optimistic about their near-term operating conditions.

Beneath the surface, inflation pressures appear to be building again. The net percentage of firms expecting to raise prices over the next three months fell 4 points to 53%, partially reversing last month’s surge. Yet cost expectations remain elevated, with 79% of firms anticipating higher costs — the highest level since July 2023.

More notably, one-year inflation expectations rose from 2.77% to 2.93%, their highest level since July 2024. Wage expectations climbed above 3% for the first time since April 2024.

ANZ noted that pricing intentions are not consistent with widespread expectations of a steady decline in headline inflation this year. Although inflation is projected to return to the target band in Q1 and the RBNZ has expressed confidence in the disinflation path, the survey highlights ongoing upside risks.

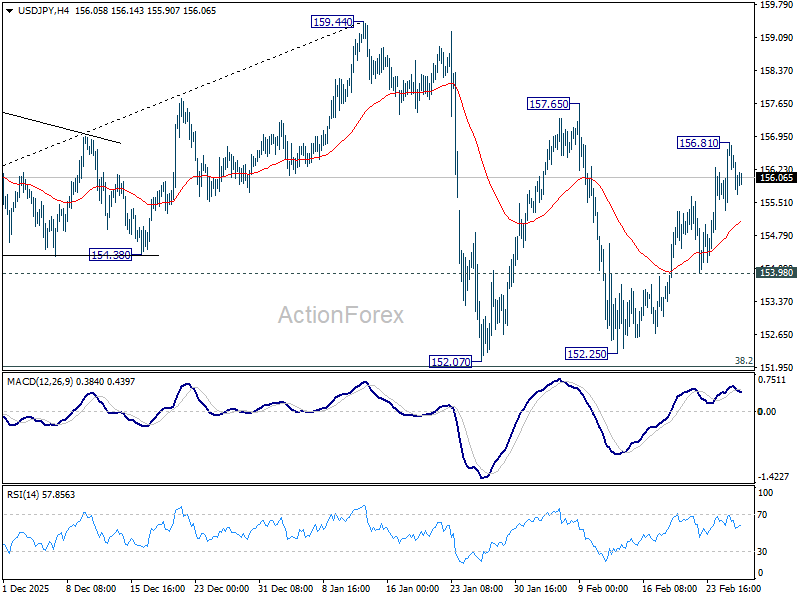

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.54; (P) 156.19; (R1) 157.02; More…

Intraday bias in USD/JPY remains neutral and some more consolidations could be seen below 156.81 temporary top. On the upside, above 156.81 will resume the rally from 152.25 to 157.65 resistance first. Firm break there will target a retest on 159.44. high. On the downside, however, break of 153.90 will bring deeper fall to 152.25 support. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

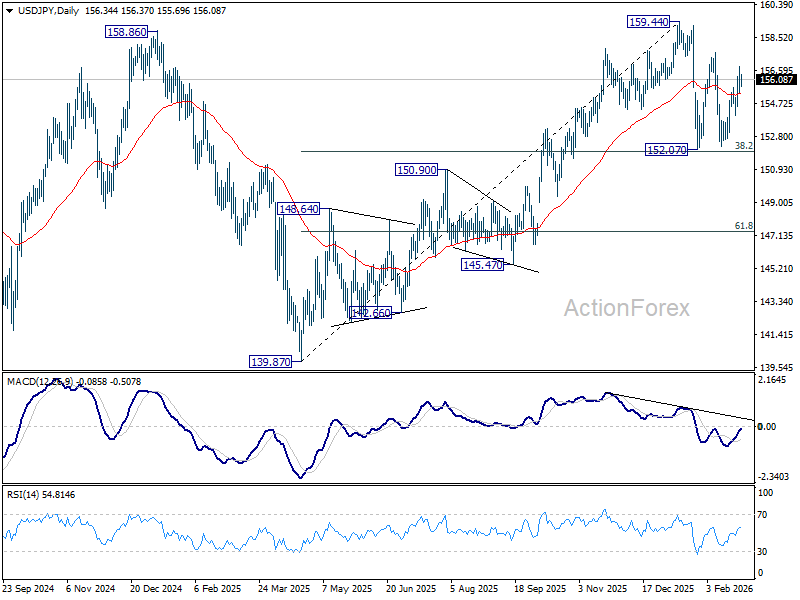

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

{kind=link}