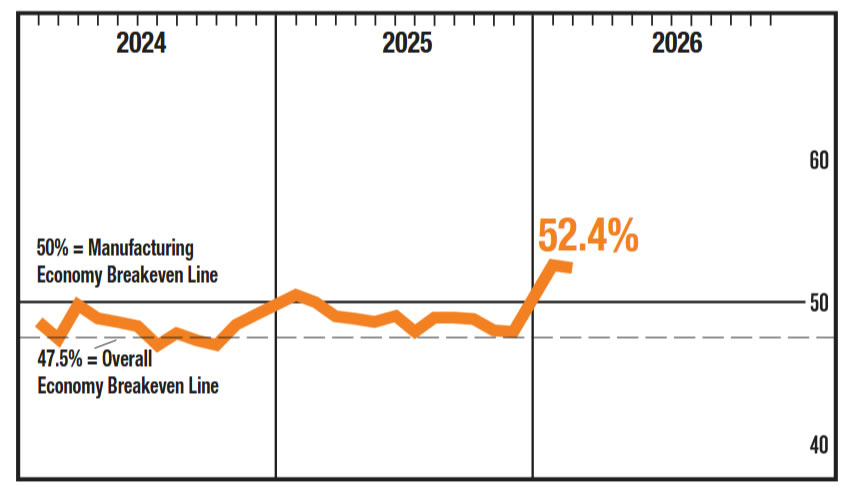

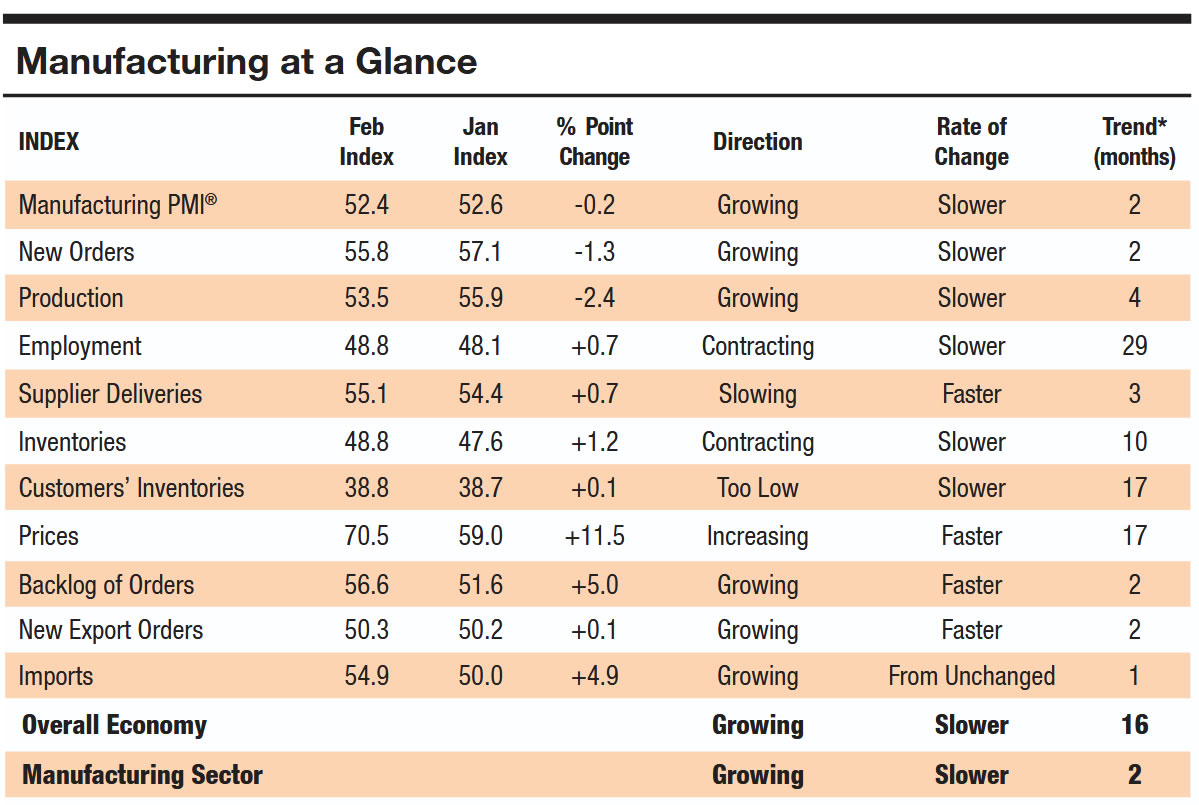

US ISM Manufacturing PMI edged down from 52.6 in January to 52.4 in February, but the reading remained comfortably above expectations of 51.9 and firmly in expansion territory. The data point to continued resilience in the factory sector, with activity still consistent with moderate economic growth.

The most striking development was the sharp surge in the Prices Index, which jumped from 59.0 to 70.5 — the highest level since June 2022. The move signals a renewed acceleration in input cost pressures and raises questions about the pace of disinflation in the goods sector, particularly as energy and supply risks intensify.

Underlying components showed some cooling in demand momentum. New orders declined from 57.1 to 55.8, while production eased from 55.9 to 53.5. Employment improved slightly from 48.1 to 48.8 but remained in contraction.

Importantly, only 1% of manufacturing GDP was in strong contraction territory (PMI at or below 45), down sharply from 12% in January. Historically, a PMI reading of 52.4 corresponds to roughly 1.7% annualized real GDP growth.

{kind=link}