The “safe haven” trade continues to unwind today, as seen in the weakness in Dollar. This softening is mirrored across the traditional safe-haven trio, with Yen and Swiss Franc also underperforming. The primary catalyst for this shift in sentiment is the “Trump de-escalation” narrative regarding the Iran conflict, which has successfully pulled a significant portion of the geopolitical risk premium out of the currency markets.

Meanwhile, the greenback is not simply drifting; it is bracing for a critical fundamental test in the form of the February US CPI data. The timing of this February report is particularly vital. Because the massive “war premium” that spiked gasoline and energy prices occurred late in the month and into March, today’s data offers a final “clean” look at underlying US inflation. It represents the baseline of price pressures that existed before the latest global shock, allowing the market to see if the disinflationary trend continued to stall, or even reversed.

Expectations for the Fed’s policy path have undergone a drastic recalibration since the onset of the Iran conflict. While the market was once hopeful for a series of aggressive cuts in early 2026, those dreams have largely evaporated. However, it is important to note that expectations have not yet flipped to a regime of further rate hikes; instead, the market has just moved into a defensive “higher for longer” stance.

Traders are now treating a March “hold” as a certainty, with the focus shifting to the mid-year outlook. Fed Fund futures currently indicate only a 40% chance of a cut in June, making September the more realistic candidate for any policy easing. This reflects a broader consensus that we are looking at a maximum of two cuts this year, a far cry from the aggressive easing cycles predicted just months ago.

Today’s core inflation readings will be an important arbiter of this outlook. Should Core CPI print higher than 0.3% mom, or exceed 2.5% on an annual basis, the narrative could shift significantly. Such a “hot” reading would likely force traders to move beyond the “hold” scenario and seriously entertain the possibility of an interest rate hike to combat a secondary wave of inflation.

Conversely, a downside surprise in the core readings would be a major relief for the markets. If a cooling CPI is coupled with the current pullback in oil prices—specifically if Brent and WTI slide below 80 mark—hopes for a rate cut in the first half of the year could be revived. This would likely accelerate the Dollar’s slide as the “yield advantage” narrative weakens.

For the week so far, Aussie is leading the pack as the week’s top performer. Markets are aggressively betting on a hawkish divergence, where the RBA pulls ahead a rate hike from May to this month. Following the Aussie’s lead are the Kiwi and Sterling, both of which are capitalizing on the “risk-on” mood. These currencies are effectively absorbing the liquidity that is currently exiting the safe-haven trio of Dollar, Yen, and Franc, which sit at the bottom.

In Asia, at the time of writing, Nikkei is up 1.94%. Hong Kong HSI is down -0.20%. China Shanghai SSE is down -0.04%. Singapore Strait Times is down -0.11%. Japan 10-year JGB yield is down -0.012 at 2.174. Overnight, DOW fell -0.07%. S&P 500 fell -0.21%. NASDAQ rose 0.01%. 10-year yield closed flat at 4.136.

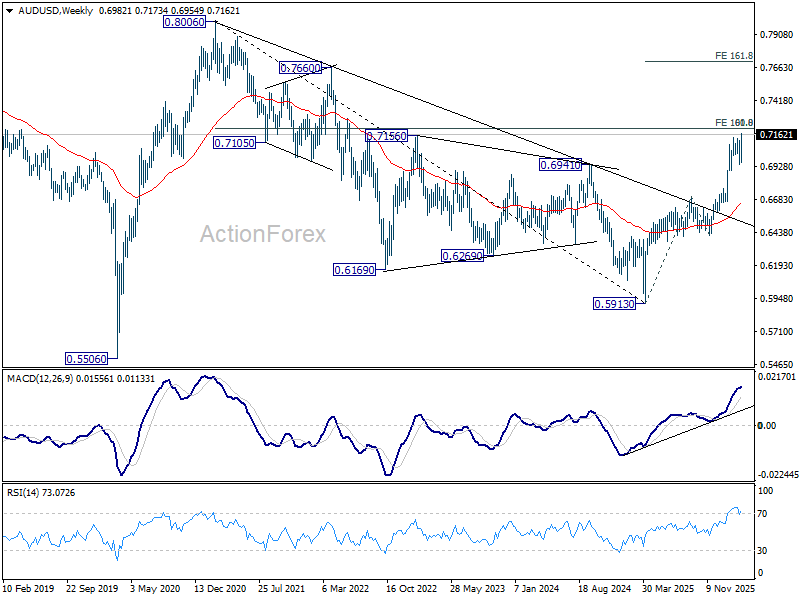

AUD/USD Breakout as RBA Faces Urgency to Hike, 0.80 After Clearing 0.72?

Aussie has staged a remarkable breakout today, surging broadly higher to clip a near four-year peak against Dollar. AUD/USD is now knocking on the door of a critical resistance zone at 0.72. Firm break above this level wouldn’t just be a win for the bulls—it would signal strong underlying momentum that could pave the way for a climb toward 0.77 or even a return to 0.80 handle.

This aggressive rally isn’t happening in a vacuum. It is being fueled by a violent repricing of interest rate expectations. Global markets have suddenly realized that the RBA is pivoting toward a much more aggressive tightening cycle than anyone predicted just a month ago. The “patience” stance is being replaced by a sense of tactical urgency.

Previously, the “consensus” roadmap was clear and cautious. Following the 25bp hike to 3.85% in February, the RBA was expected to hold steady on March 17. The plan was to wait for the comprehensive quarterly CPI data in late April before considering a follow-up move in May. It was a “wait-and-see” approach designed to protect the economy.

However, the outbreak of the Iran war has shredded that calculus. The geopolitical shock sent oil prices into a frenzied spike to $120 earlier this week. While prices have pulled back, they remain stubbornly elevated above $80—carrying a “war premium” of roughly $20 compared to pre-conflict levels. For a central bank fighting inflation, this is an external shock that cannot be ignored.

The RBA could now view waiting until May as a luxury it simply cannot afford. There is a growing fear within the Board that if inflation expectations become “unanchored” due to this energy shock, the genie will be impossible to put back in the bottle. To prevent inflation from running further away, the RBA could feel compelled to act as an “inflation hawk” right now.

The data justifies this anxiety. Headline CPI sat at 3.8% in January, but the real concern lies in the Trimmed Mean, which rose to 3.4%. Both figures are well above the RBA’s 2–3% target range. More importantly, the rise in the Trimmed Mean—which strips out volatile items like petrol—proves that inflation is not just a “fuel story.” It is becoming “sticky” and embedded across the broader service economy.

The messaging from Martin Place has been unusually blunt. Deputy Governor Andrew Hauser has led the charge this week, using his platform to describe high inflation as “toxic.” He cautioned that the Middle East conflict could push domestic prices even higher, emphasizing that the March 17 meeting will involve a “very genuine debate” about hiking. In central-bank-speak, a “genuine debate” is a clear warning that a hike is on the table.

The banking sector has heard the message loud and clear. NAB and Westpac official teared up their old playbooks. Both banks now forecast back-to-back 25-basis-point hikes in both March and May.

Technically, AUD/USD’s up trend from 0.5913 (2025 low) resumed today and it will soon be testing a key cluster resistance zone at around 0.72. That zone includes 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213, and 61.8% retracement of 0.8006 (2021 high) to 0.5913 at 0.7206. Decisive break there would pave the way to 161.8% projection at 0.7703 or even further to 0.8006 high.

Japan import costs surge on weak Yen, fastest since July 2024

Japan’s producer inflation moderated in February, offering some relief on the domestic cost front even as import prices surged. Producer Price Index rose 2.0% yoy, slowing from January’s 2.3% pace and coming in slightly below market expectations of 2.1%.

The softer PPI reading suggests upstream price pressures in Japan’s domestic production sector may be easing slightly. However, the picture is less benign when looking at import costs, which are heavily influenced by Yen’s weakness.

Japan’s yen-based import price index jumped 2.8% yoy, accelerating sharply from a revised 0.7% increase in January and marking the fastest rise since July 2024. The data highlights how the weak Yen continues to push up import costs, a dynamic that could keep underlying inflation pressures elevated despite the moderation in producer prices.

ECB’s Lagarde says too much uncertainty to predict March rate decision

ECB President Christine Lagarde signaled that policymakers will remain vigilant against inflation risks stemming from the Iran war while avoiding hasty decisions in the face of heightened uncertainty. In an interview with France2, Lagarde said the ECB will ensure the conflict does not trigger the kind of inflation shock the Eurozone experienced after Russia’s invasion of Ukraine.

“We are in an economic situation that’s different,” Lagarde said, adding that the Eurozone now has a “greater capacity” to manage disruptions. She emphasized that the ECB will take the necessary steps to keep inflation under control and avoid a repeat of the sharp price increases seen in 2022 and 2023 following the energy crisis triggered by the Ukraine war.

At the same time, Lagarde acknowledged that the current geopolitical environment makes policymaking particularly challenging. With the Iran conflict adding new uncertainty to global energy markets, she said it was impossible to predict the outcome of the ECB’s March 18–19 policy meeting. “There is so much uncertainty that I’d be incapable to say precisely what we will decide,” she said.

Lagarde added that the degree of volatility currently facing policymakers is unusually high, even compared with the turbulence seen during the 2022 energy shock. Nevertheless, she rejected the suggestion that Europe is heading toward stagflation, insisting that the ECB remains committed to maintaining price stability while navigating the heightened uncertainty.

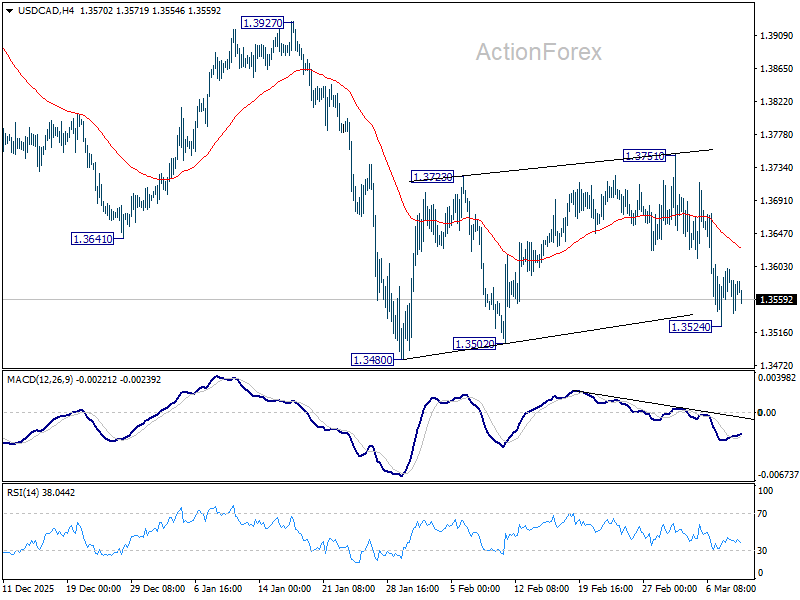

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3575; (R1) 1.3609; More…

Intraday bias in USD/CAD is turned neutral first with a temporary low formed at 1.3524. Nevertheless, outlook is unchanged that consolidation pattern from 1.3480 could have completed at 1.3751, after hitting 55 D EMA (now at 1.3704). Risk will stay on the downside as long as 1.3751 resistance holds. On the downside, below 1.3524 will bring retest of 1.3480 low. Firm break there will confirm resumption of whole fall from 1.4791, and target 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

{kind=link}