Summary

U.S. Week In Review

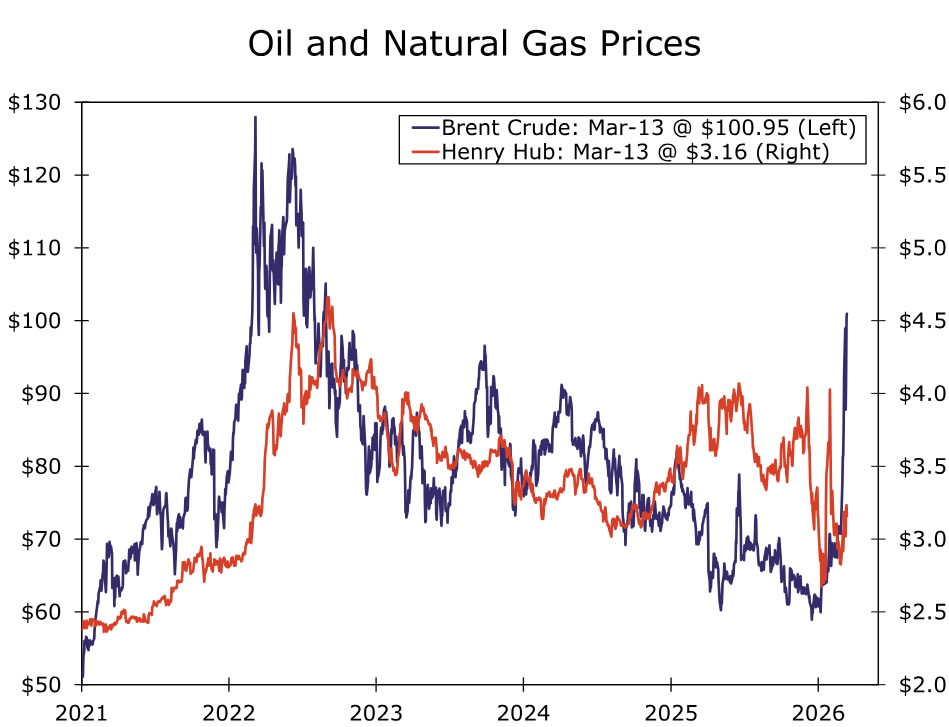

- Nearly two weeks into the conflict with Iran, energy prices have surged, adding fresh inflation risk to an already fragile backdrop. Recent CPI and PCE data show further progress on inflation stalling out, driven in part by rising energy and goods prices, with March energy inflation expected to spike sharply if gasoline prices remain elevated. Housing activity remains subdued due to affordability constraints, as higher mortgage rates and soft single‑family demand offset pockets of strength in multifamily construction, while small business sentiment has weakened modestly. For the Fed, the uncertain inflation and labor market outlook reinforces a data‑dependent stance, with two rate cuts still our expectation this year, though persistently high oil prices and rising inflation expectations could delay or reduce future easing.

U.S. Week Ahead

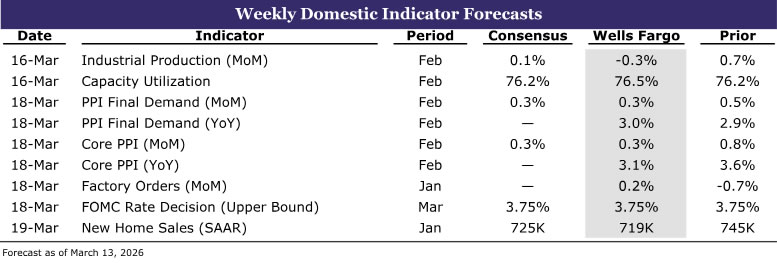

- The FOMC meeting will be the focal point next week, as intensifying stagflation risks put the Fed’s dual mandate in tension. We expect the Committee to hold rates steady and emphasize optionality, with the updated SEP likely to show that expectations for slightly higher inflation and lower growth will net out to an unchanged policy path. Elsewhere, activity in interest rate sensitive sectors remains touch and go; we forecast industrial production slipped in February and new home sales rose in January.

U.S. Week in Review

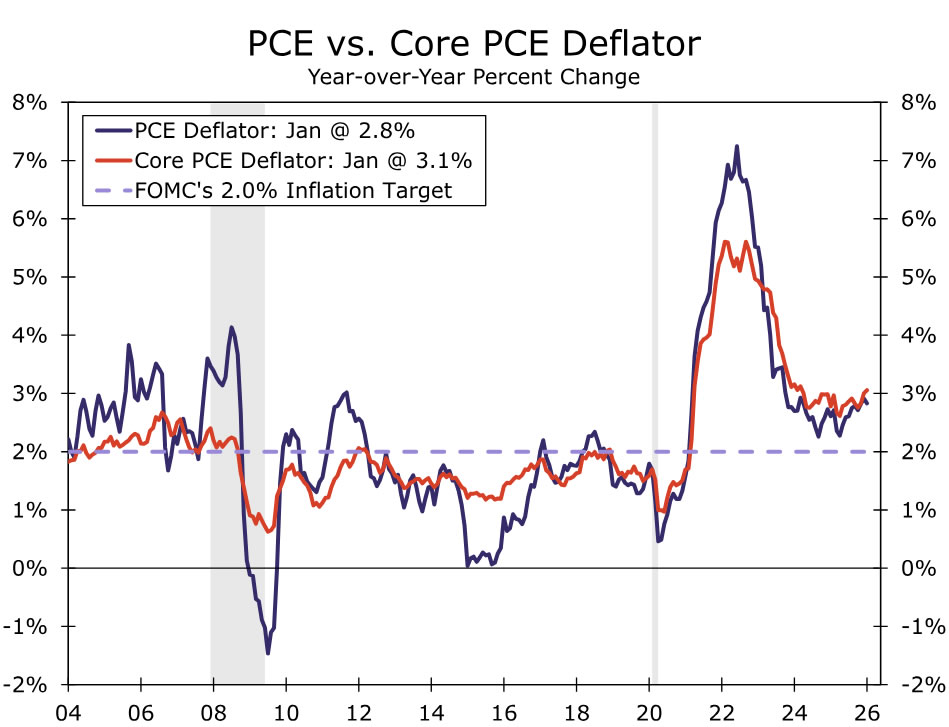

It has been almost two weeks since the start of the conflict with Iran, and since then, oil prices have been very volatile. As we go to print, the price of Brent crude has risen $32 since the U.S. strikes, or about 46% above its February average. Henry Hub natural gas prices are also up 4% in the wake of the strikes. The surge in oil prices introduces fresh risk to an already complicated economic environment. A renewed rise in energy prices is especially troublesome for inflation, which has stalled on its progress back toward 2%. We got fresh CPI data this week, which showed that headline inflation rose 0.3% in February, leaving the year-over-year rate at 2.4% but pushing the more recent three-month annualized pace up to 3.0%. Energy prices rose 0.6% in February, driven primarily by a solid 1.1% gain in energy goods. Oil and gas prices were already rising in February in anticipation of a conflict in the Middle East, underpinning the strength, and we anticipate this will only further strengthen in March. Assuming the cost of regular gas averages $3.65 per gallon for the rest of this month, we estimate energy goods will rise a more jarring ~18% month-over-month in March. Core CPI increased a moderate 0.22%, with softer vehicle prices offset by firmer gains in tariff-exposed goods such as apparel and household furnishings, while core services rose 0.3%, led by travel and medical services. Inflation pressures appear more stubborn in the PCE deflator, the Fed’s preferred inflation metric. Headline PCE rose 0.3% over the month and 2.8% over the year in January, while core PCE rose 0.4%, lifting the year-ago rate a tenth to 3.1%. We estimate both headline and core measures to rise around 0.4% in February.

On the housing front, housing starts jumped 7.2% in January, though this was driven by a surge in multifamily starts. Underlying details painted a weaker picture as single‑family starts declined and permits fell. Builder confidence deteriorated amid slowdowns in buyer traffic and a weakening in sales expectations. That said, there remains scope for improvement in multifamily development, driven primarily by single-family affordability challenges and thinning apartment supply. Affordability remains a significant hurdle for home sales, and this was apparent in the existing home sales print for February. Though existing home sales rose 1.7% to a 4.09 million-unit pace in February, sales remain notably below the trend in late 2025. Mortgage rates remain elevated around 6.0%-6.1%, and inventories remain strong. Overall, home buying is likely to slowly improve over the course of the year, but likely should continue to run at a sluggish rate due to the adverse affordability conditions.

Small business sentiment softened for a second month as firms pared back hiring and capex plans, though optimism about broader economic conditions remained relatively constructive, supported by solid earnings and sales. Meanwhile, trade data continue to be distorted by investment‑related flows such as non‑monetary gold. These data won’t translate directly to what is included in GDP accounting, and thus the $18.4 billion narrowing in the January trade deficit overstates the growth impact. Strong demand for high-tech-related products has propped up imports, though non-monetary gold accounted for roughly 40% of the overall drop in imports over the month. We expect the trade deficit to widen over the course of the year due to pent-up import demand and near-term clarity on tariffs.

It is times like these that justify the mantra of “data-dependence” for policymakers at the Fed. Given the inflation data from this week are a bit more dated than is typical when heading into the March meeting, we expect they do little to sway the hawks, doves, and undecideds one way or another. Policymakers are likely to focus instead on the uncertain outlook for energy prices and the broader inflation outlook in light of the developing conflict with Iran. On face value, the Fed is likely to look through a temporary energy-driven increase in inflation. However, inflation expectations are highly sensitive to energy prices, and sustained upward pressure on inflation could narrow the margin for additional easing and delay future rate cuts, particularly if labor market cooling continues to be gradual. For now, our base case forecast remains two 25 bps rate cuts at the June and September FOMC meetings. That said, the longer oil prices remain elevated, the more difficult that may be to realize.

U.S. Week Ahead

Industrial Production • Monday

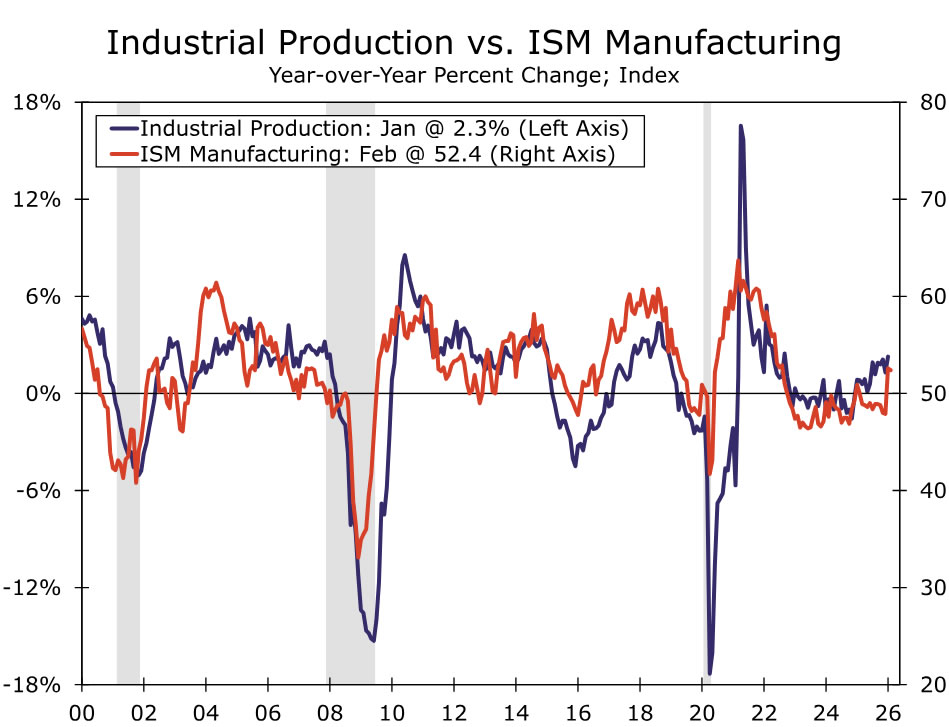

The manufacturing backdrop remains touch and go amid elevated uncertainty. We have long expected a rebound in broad manufacturing activity this year as firms begin to reengage sidelined capital spending plans that were delayed by tariffs, but the latest conflict in Iran introduces new downside risks to that outlook. Recent industrial data point to modest improvement at the margin, though growth continues to be driven primarily by high-tech-related investment rather than more traditional areas of capex.

That said, pent-up demand for conventional capital spending, combined with a recent easing in tariff pressures following the ruling against IEEPA tariffs and the maintenance of a 10% baseline tariff, could support a gradual pickup in activity. February ISM manufacturing edged down just 0.2 points to 52.4 but remained in expansion territory, supported by strength in new orders, production and supplier deliveries. Against this backdrop, we expect industrial production slipped modestly in February, down 0.3%.

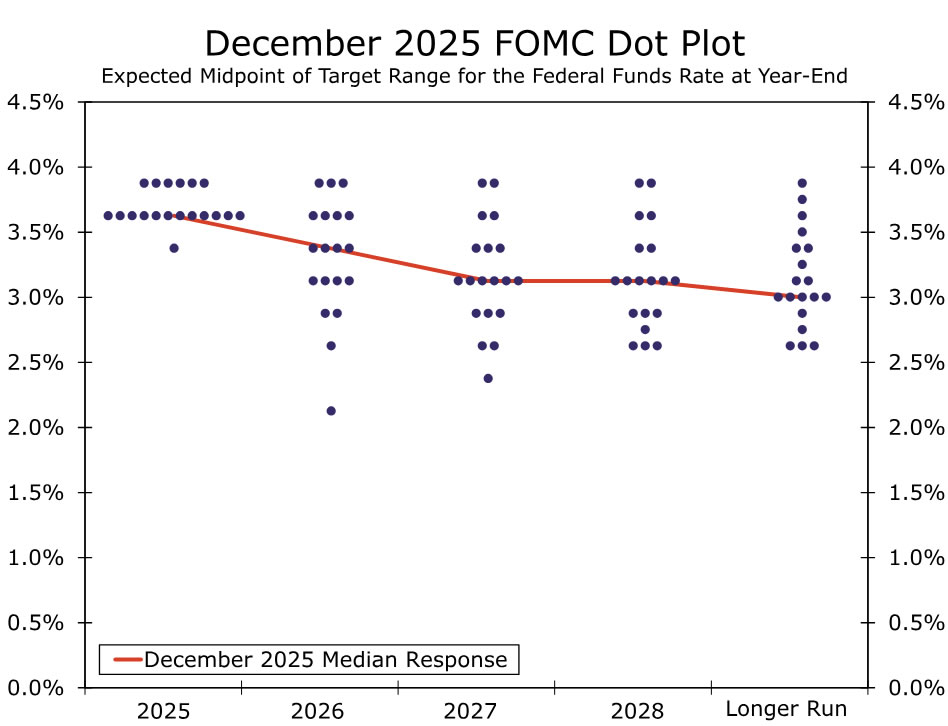

FOMC • Wednesday

Stagflation risks have increased since January, putting the FOMC’s dual mandate in tension. Volatile energy prices tied to the Iran conflict have induced uncertainty, but the net signal from recent data is little changed: the labor market is still muddling along, and PCE inflation remains stuck near 3%. We expect the Committee to hold rates steady next week and lean heavily on optionality, emphasizing that higher uncertainty argues for a data-dependent approach.

The Summary of Economic Projections (SEP) should tilt modestly in a stagflationary direction, with higher inflation forecasts extending into 2027, and slightly lower GDP projections and modestly higher unemployment rate expectations for 2026. We expect the median dot for the federal funds rate to remain unchanged, as the risks of higher inflation and lower growth are likely to offset each other. Our forecast continues to call for two 25 bps cuts in June and September, alongside a well‑telegraphed slowdown in balance sheet runoff that should have minimal impact on longer-term interest rates.

New Home Sales • Thursday

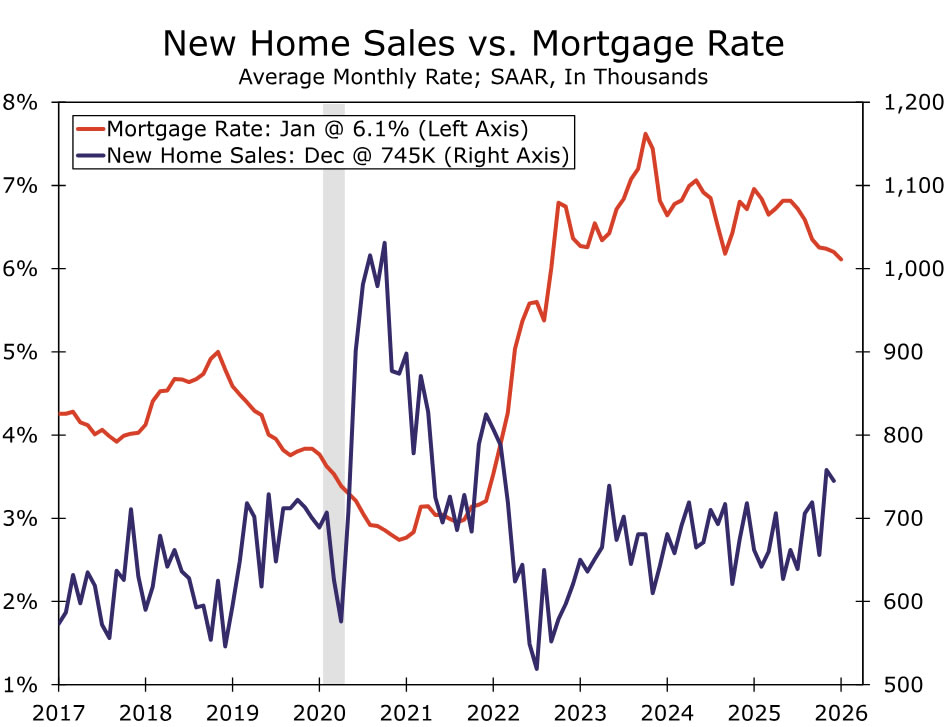

New home sales are gaining momentum. After averaging a 660K annual pace through the first half of 2025, which was slightly below the year prior, the average pace of transactions jumped to 751K in November and December. Lower mortgage rates appear to be a main driver. The average 30-year fixed rate fell from 7.0% in January 2025 to 6.2% in December and have since slid further to 6.0%. Furthermore, approximately two-thirds of builders are using incentives like price cuts and mortgage rate buy-downs to offset macro challenges, an elevated share compared to recent history.

Harsh winter weather likely prompted some giveback in January. However, price cuts and lower mortgage rates are likely to sustain a healthy overall pace of transactions. We forecast that 2026 started off with a 719K annual sales rate in January, which would be near the upper end of new home sales’ overall range last year.

We expect that new home sales will sustain this momentum over the course of 2026. Builder incentives will likely continue to buttress new home sales in the year ahead. We also anticipate an average 30-year mortgage rate of around 6.1% this year, still elevated but below the 6.6% average in 2025. That said, lofty inventory-to-sales ratios will likely preclude a corresponding pickup in single-family construction.

{kind=link}