Markets traded in a subdued tone through most of the day, with investors largely sidelined ahead of the Federal Reserve’s policy decision. That calm was abruptly shattered as the US session began, with a sharp deterioration in risk sentiment accompanied by a broad rebound in Dollar and a selloff in equity futures.

The sudden shift was driven by a double shock. Oil prices surged after reports of Israeli and US air strikes targeting Iran’s South Pars gas field and the Asaluyeh energy complex in Bushehr Province, while US PPI data came in significantly stronger than expected, reinforcing inflation concerns just hours before the Fed decision.

The energy red line has been crossed

The strike on South Pars marks a critical escalation in the conflict. Until now, markets had largely assumed that core energy infrastructure—particularly assets of systemic global importance—would remain off-limits to avoid triggering a global economic shock. That assumption has now been broken.

By targeting Asaluyeh, the conflict has moved beyond proxy confrontations to direct hits on economic arteries. The development raises the risk that other key energy assets in the region, including those in Saudi Arabia and the UAE, could come into scope, increasing the probability of broader supply disruptions.

The implications extend beyond global markets. South Pars accounts for roughly 70% of Iran’s domestic gas supply, and disrupting it during a period of conflict is likely to intensify internal pressure on the Iranian regime. Historically, such pressure has often led to more aggressive external responses, including threats to oil flows through the Gulf.

Inflation already accelerating before the first missile was fired

At the same time, inflation risks were already building even before the geopolitical shock. US PPI rose 0.7% mom in February, more than double expectations, while the annual rate accelerated to 3.4% yoy, the fastest pace in a year. The data signals that upstream price pressures were strengthening prior to the outbreak of the Iran conflict.

Importantly, the composition of the PPI report points to structural inflation. Gains were broad-based, with services leading but goods prices also rising sharply. Increases in tariffs, metals, and industrial inputs highlight that cost pressures are embedded across the production chain rather than driven by temporary factors.

This creates a more challenging backdrop for policymakers. If inflation was already accelerating before the war, the subsequent surge in energy prices—yet to be reflected in official data—suggests that the forward inflation path could be significantly higher. The Fed is therefore faced with inflation pressures that are both structural and geopolitical.

Market reaction reflects this repricing. Dollar has emerged as the strongest performer on the day. Commodity currencies show mixed performance, with Loonie supported by oil, but Aussie and Kiwi under pressure amid broader risk aversion.

In Europe, at the time of writing, FTSE is down -0.60%. DAX is down -0.52%. CAC is up 0.01%. UK 10-year yield is up 0.067 at 4.692. Germany 10-year yield is up 0.021 at 2.928. Earlier in Asia, Nikkei rose 2.87%. Hong Kong HSI rose 0.61%. China Shanghai SSE rose 0.32%. Singapore Strait Times rose 1.34%. Japan 10-year JGB yield fell -0.045 to 2.218.

“Hawkish hold” may disappoint as Fed avoids committing either way

A “hawkish hold” is priced in—but the Fed may deliver something more neutral. If so, markets could be caught off guard, opening the door to a sharp repricing in Dollar and global assets. Read more.

US PPI jumps 0.7% mom, services and goods both rise

US PPI beat expectations at 0.7% mom, with broad-based gains in services and goods pushing annual inflation to 3.4% yoy. Persistent core strength signals inflation risks are far from easing. Read more.

Eurozone CPI finalized at 1.9% in February as price pressures broaden

Eurozone CPI was finalized at 1.9% yoy in February, while core rose to 2.4% yoy, led by strong services inflation. Persistent underlying pressures are likely to keep ECB cautious despite near-target headline CPI. Read more.

Swiss growth outlook cut as energy shock and strong Franc weigh on economy

Switzerland’s 2026 growth forecast was cut to 1.0% as rising energy prices and geopolitical uncertainty weigh on demand. Inflation is now seen slightly higher, while a strong franc and weak global outlook continue to drag on exports. Read more.

Japan trade data highlights diversification, shift away from China and U.S.

Japan’s exports rose 4.2% yoy in February, beating forecasts despite sharp declines in shipments to China and the U.S. Strong demand from Southeast Asia and Europe helped offset weakness, signaling a shift in trade dynamics. Read more.

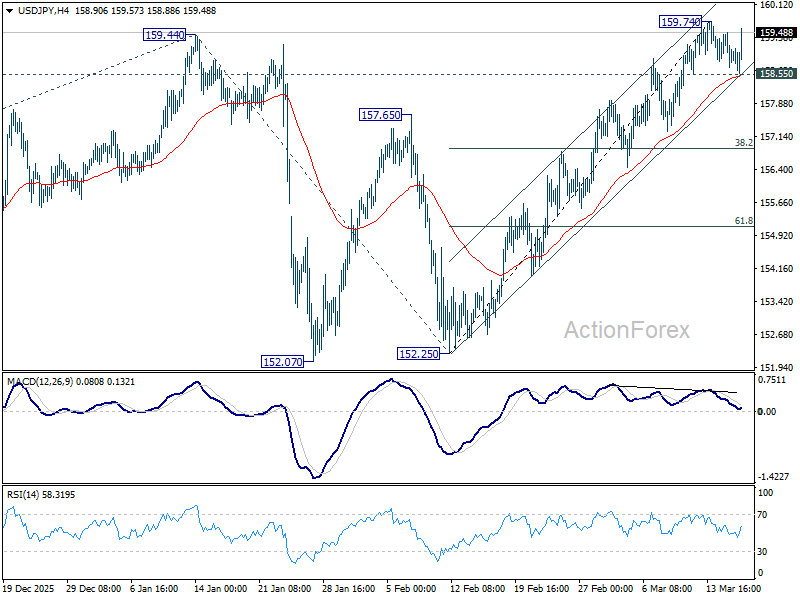

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.65; (P) 159.07; (R1) 159.43; More…

USD/JPY rebounded strongly after touching 158.55 support and focus is back on 159.84 temporary top. Above there will resume the rally from 152.25 to retest 161.94 high. Firm break there will confirm larger up trend resumption and target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. Nevertheless, considering bearish divergence condition in 4H MACD, break of 158.55 should indicate short term topping. Intraday bias will then be back on the downside for 38.2% retracement of 152.25 to 159.74 at 156.87.

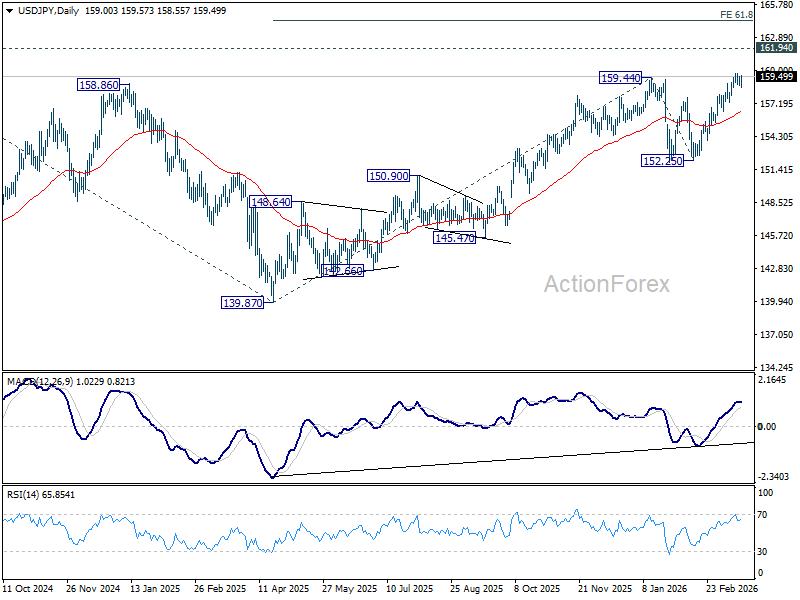

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.70) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

{kind=link}