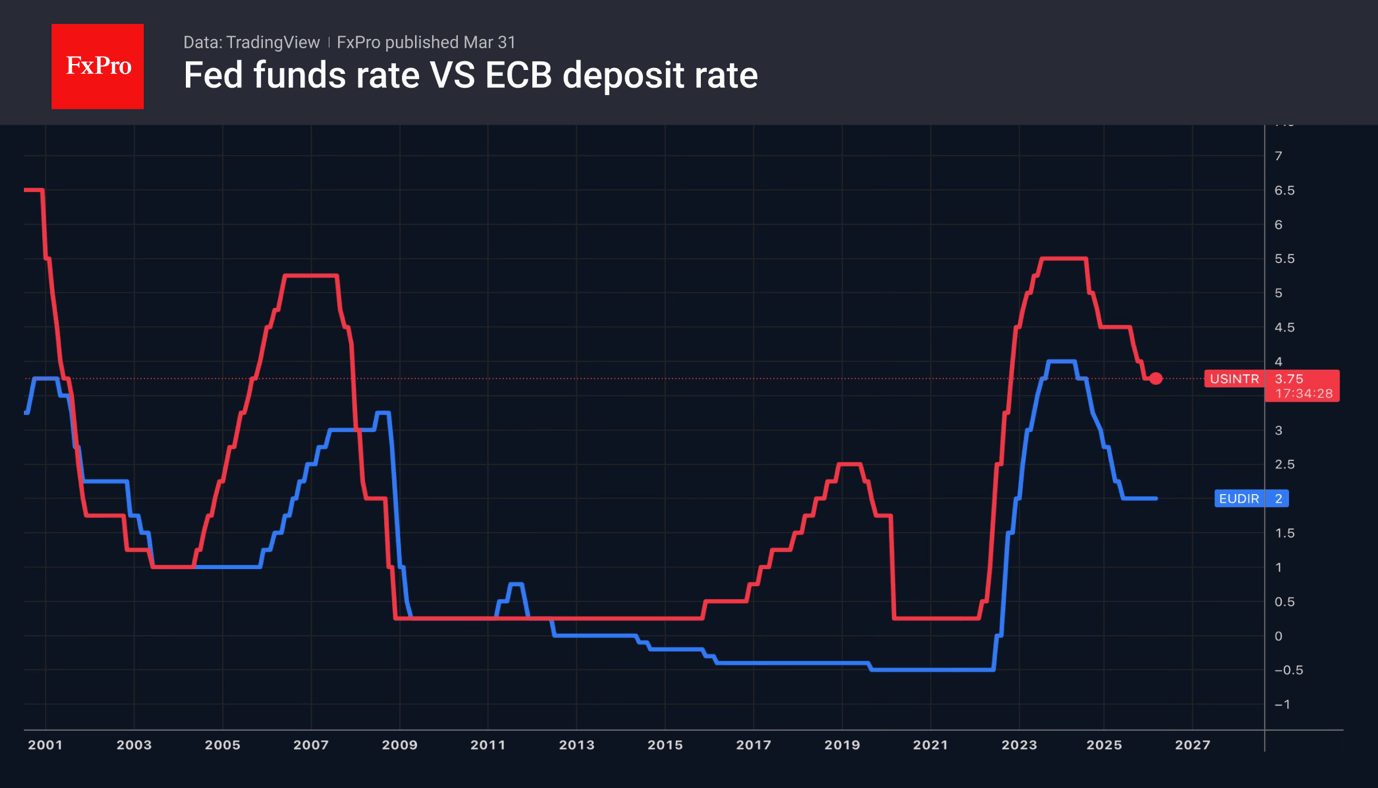

- Expectations of ECB hikes are not helping the EURUSD.

- Iran holds the reins of the conflict in the Middle East.

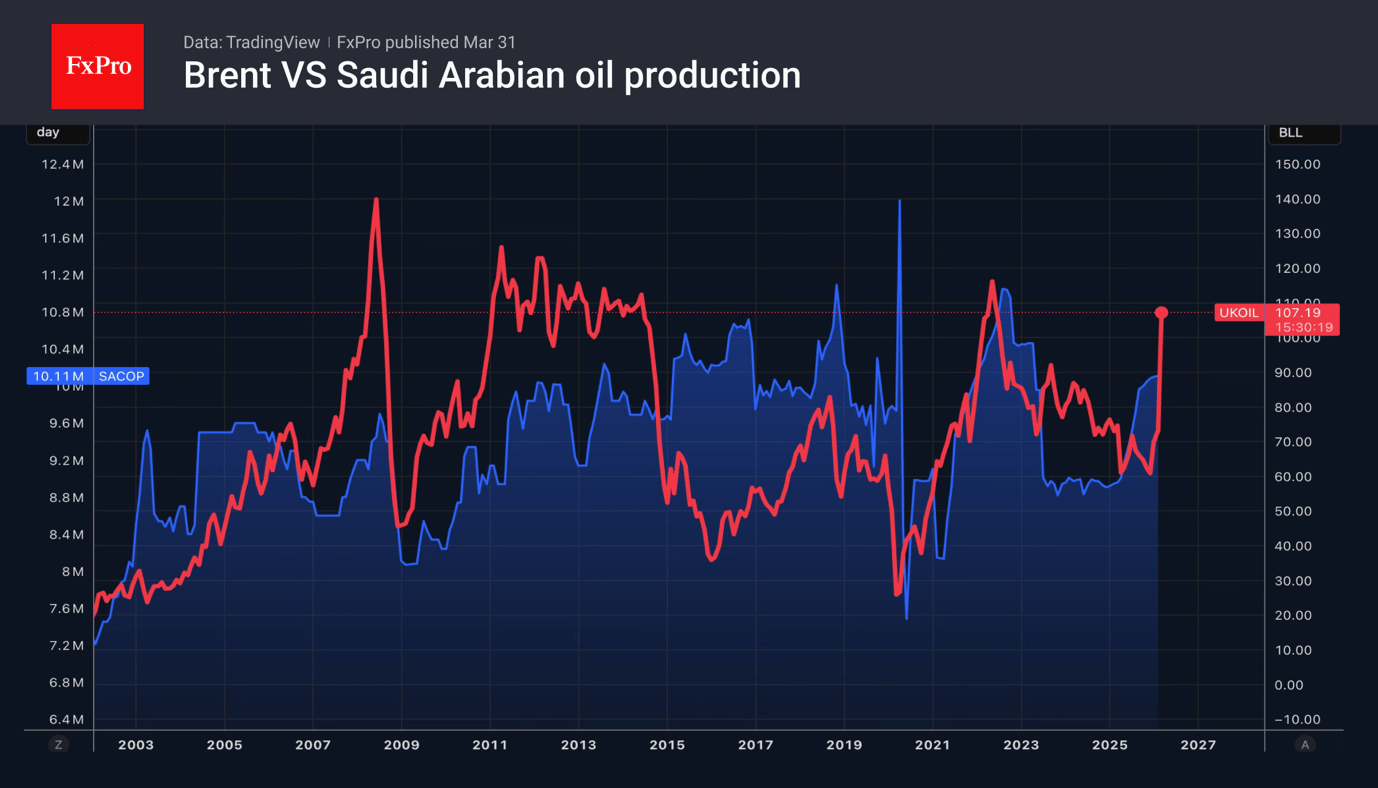

The US dollar ends March with its best monthly performance since September 2022, whilst the euro ends with its worst quarterly performance since 2024. This divergence has been driven by investor concerns about the global economy. The conflict in the Middle East has pushed Brent above $105 per barrel. The supply shock is heightening the risks of a slowdown in global GDP and putting pressure on currencies sensitive to falling export demand.

The divergence in monetary policy is not helping the EURUSD. Before the conflict in the Middle East, the chances of an ECB rate cut in 2026 stood at 35%, and the Fed’s at 96%. However, a month on, the futures market expects three rounds of monetary tightening from the European Central Bank, and a 74% probability that the Fed will keep the federal funds rate at its current level.

Alas, monetary policy operates with a lag and cannot counter energy disruptions in real time. This is the view of Jerome Powell. He and his FOMC colleague, New York Fed President John Williams, believe the best course is to keep rates at current levels.

Meanwhile, according to Société Générale, Brent risks rising to $150 per barrel in April, with an average price of $125. A closure of the Bab al-Mandab Strait by the Houthis could push prices higher. Saudi Arabia has managed to bypass the Strait of Hormuz and deliver 6 million BPD via alternative routes. However, new difficulties will automatically force Riyadh to cut production.

Amid escalating geopolitical tensions, risks to energy infrastructure and supply routes are driving concerns over a potential surge in oil prices and a broader economic slowdown. The situation remains fluid, leaving policymakers with difficult strategic choices. Market-based indicators suggest a rising probability of further escalation.

Meanwhile, gold is attempting a counter-offensive amid falling US Treasury bond yields. Treasury yields are falling due to a shift in investor sentiment. Whereas stagflation previously frightened them, markets are now discussing the likelihood of a US economic downturn.

{kind=link}