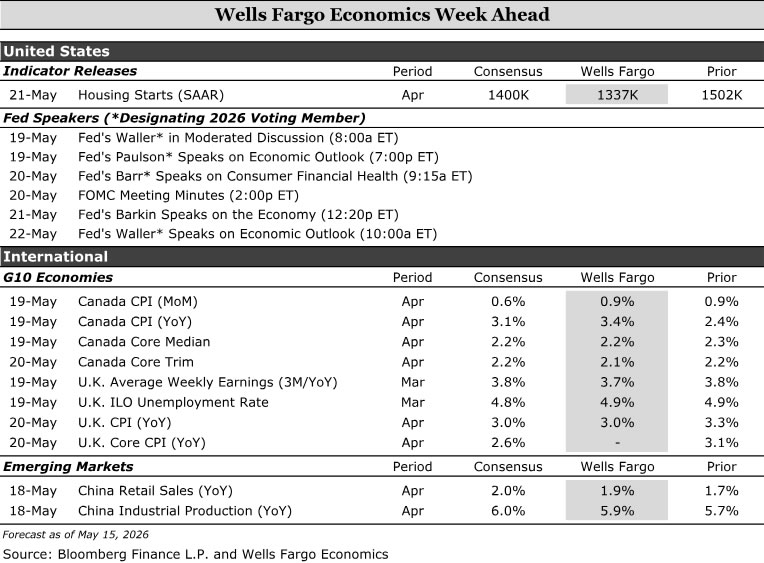

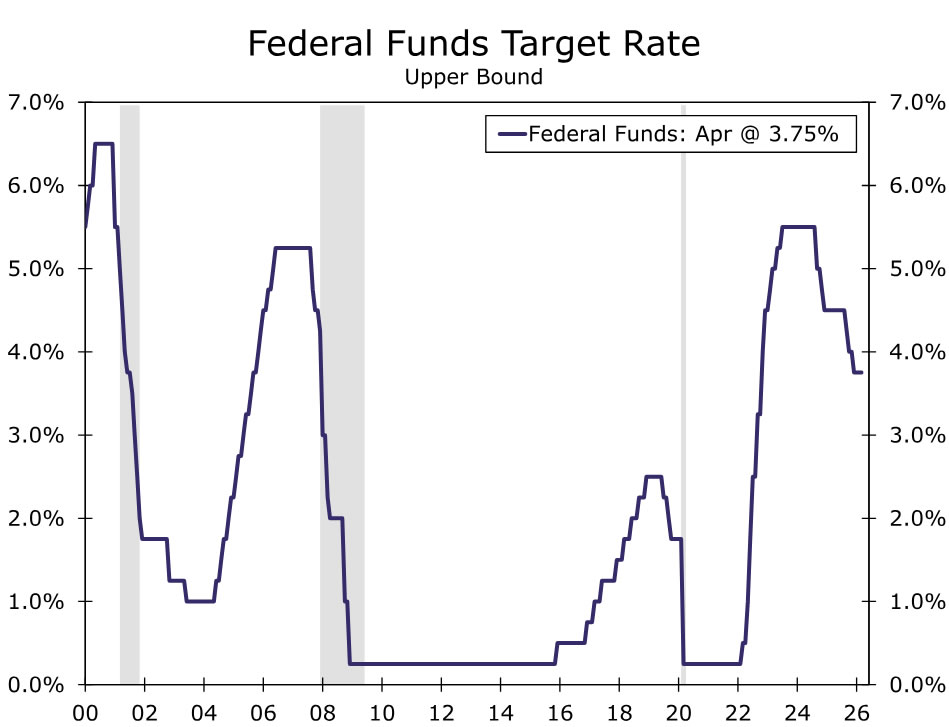

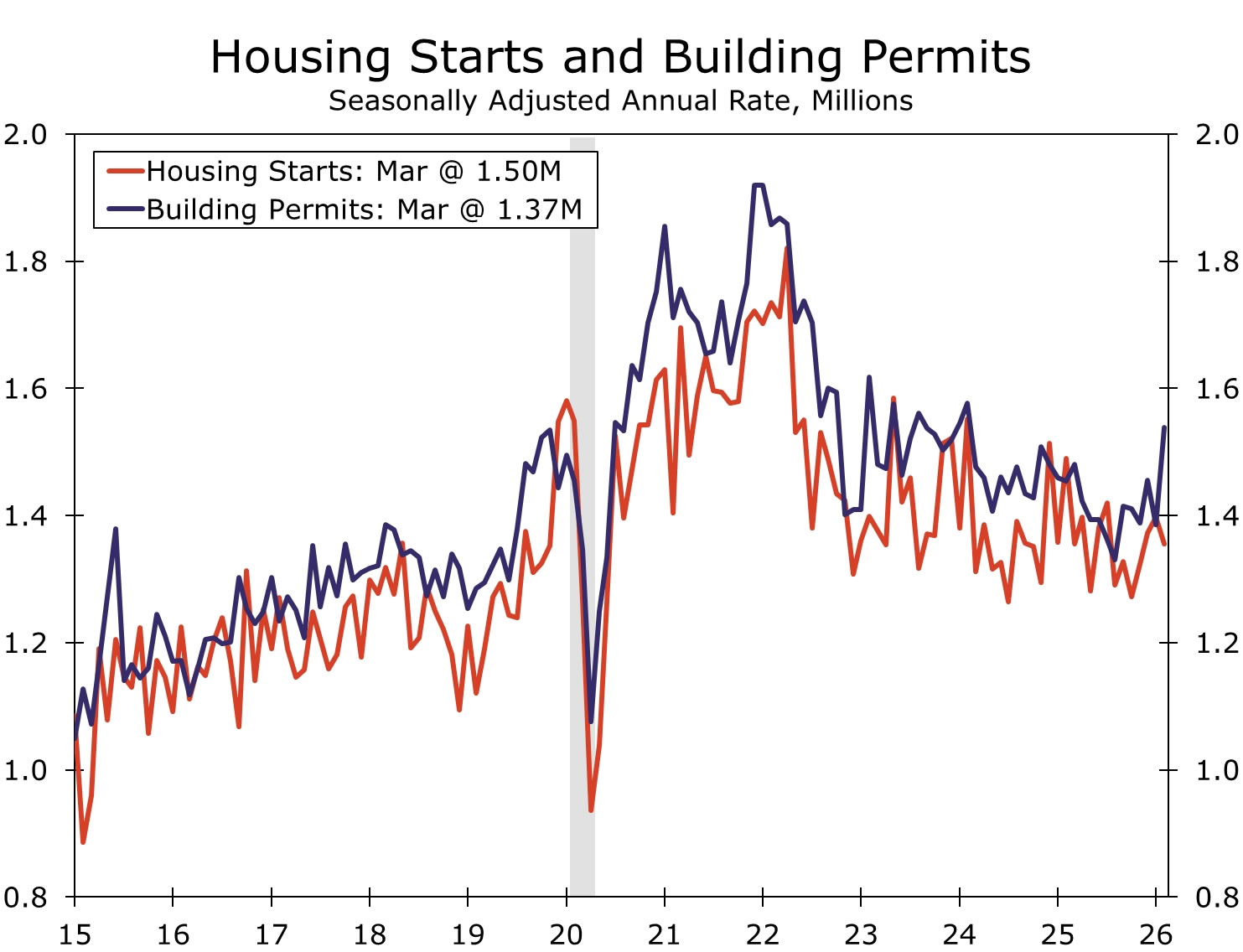

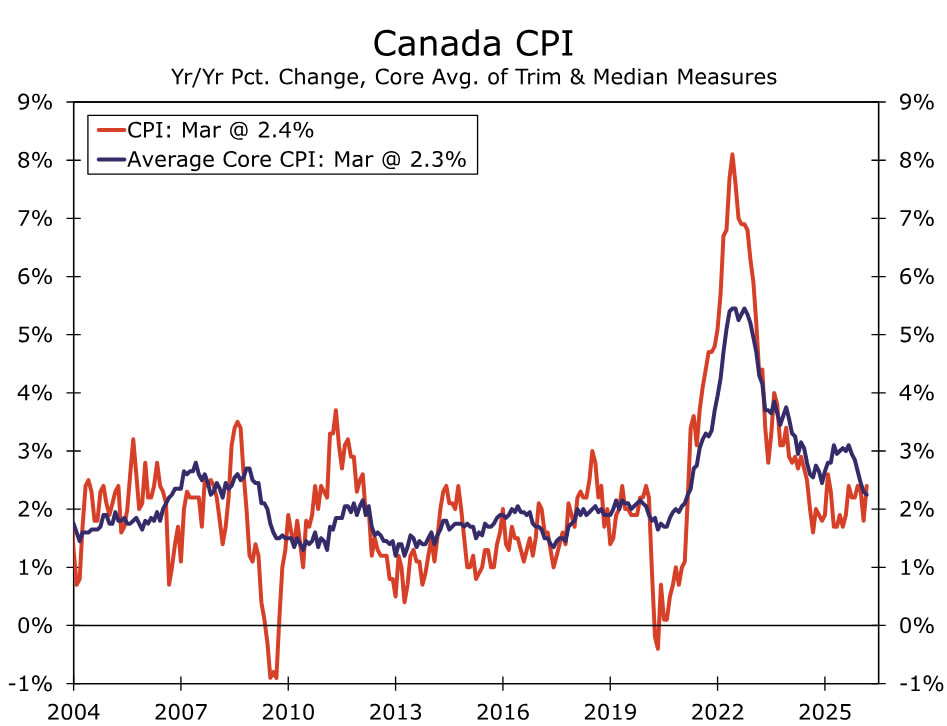

Next week’s release of the April FOMC minutes will shed light on how members of the committee saw the Fed’s next move as balanced between a hike and a cut. U.S. housing data, meanwhile, point to a moderating construction backdrop, as March’s rebound in starts likely overstated momentum amid a 2.6% year‑to‑date decline in permits and continued affordability pressures. In Canada, inflation remains elevated but mixed, with headline near 3.4% and softer core measures around 2.1–2.2%, keeping the Bank of Canada cautiously tilted toward further tightening. In the UK, easing labor market conditions—wage growth near 3.8% and declining vacancies—contrast with still‑firm inflation around 3.0%+, leaving policy finely balanced. In China, growth remains uneven but steady, with industrial production near 5.9% and retail sales around 1.9%, as strong manufacturing offsets softer domestic demand and points to a gradual cooling ahead.

United States:

- FOMC Minutes (Wednesday), Housing Starts (Thursday)

G10 Economies:

- Canada CPI (Monday), UK Labor Market Overview & CPI (Tuesday & Wednesday)

Emerging Markets:

- China Retail Sales & Industrial Production (Monday)

U.S. Week Ahead

FOMC Minutes • Wednesday

The minutes to the April 29 FOMC meeting will provide details on where the Committee stood just ahead of the leadership transition to Chair Warsh. Three voters dissented to the easing bias maintained in April’s post-meeting statement (even as they agreed with the decision to keep the fed funds rate unchanged), highlighting growing discomfort with signaling cuts as the default next move.

We will be looking at the minutes to see the extent to which non-voters shared the view that the Fed’s next move is equally likely to be a hike as a cut. Heading into the April meeting, policymakers had received more favorable employment data but were seeing renewed risks to inflation, a dynamic that has since intensified. This will make any discussion of the conditions that would warrant rate hikes more salient to the current policy outlook. At the same time, the departure of Governor Miran suggests the minutes may overstate the degree of dovish support on the Committee.

Even with a more hawkish tone likely to come through, we expect the minutes to indicate that most participants still favored holding rates steady for some time while they assess how the energy shock feeds through to inflation and the labor market.

Housing Starts • Thursday

Residential construction appears to be downshifting. Total housing starts rose strongly during March, with gains registered across both the single-family and multifamily categories. Although the improvement is an encouraging sign activity is not contracting sharply, our sense is the monthly gain was mostly payback from February’s weather-related slowdown and vastly overstated the underlying moderating trend in new construction.

So far this year, building permits have trended lower and were down 2.6% on a year-to-date basis in March. The slowdown has been most apparent within single-family, largely reflecting increased caution on the part of home builders stemming from ongoing buyer affordability challenges, soft new home sales, and elevated inventory levels. Multifamily permits have outperformed, which we attribute to firming apartment market conditions as well as a slightly lower cost of capital. Taking all of these factors into consideration, we expect housing starts declined to a 1,337K unit pace in April, lower than the current consensus estimate.

G10 Week Ahead

Canada CPI • Monday

We expect headline inflation to rise another 0.9% month-over-month in April, following a similar print in March, lifting year-over-year inflation to 3.4%. Core measures, including trimmed mean and weighted median inflation, are likely to show a further month of softening, aided by favorable base effects. We look for both trimmed mean and weighted median inflation to ease to 2.1% and 2.2% year-over-year, respectively. That said, April is likely to mark an inflection point for core inflation, with signs of underlying price pressures beginning to broaden. With headline inflation running well above the upper end of the Bank of Canada’s target range and underlying inflation set to reaccelerate, we continue to expect the Bank of Canada (BoC) to hike rates at its July meeting. The policy rate remains at the bottom of its estimated neutral range, and we expect downside risks to the BoC’s outlook to diminish as the July 1 USMCA deadline passes without new tariffs, leaving the parties locked into a prolonged annual review process.

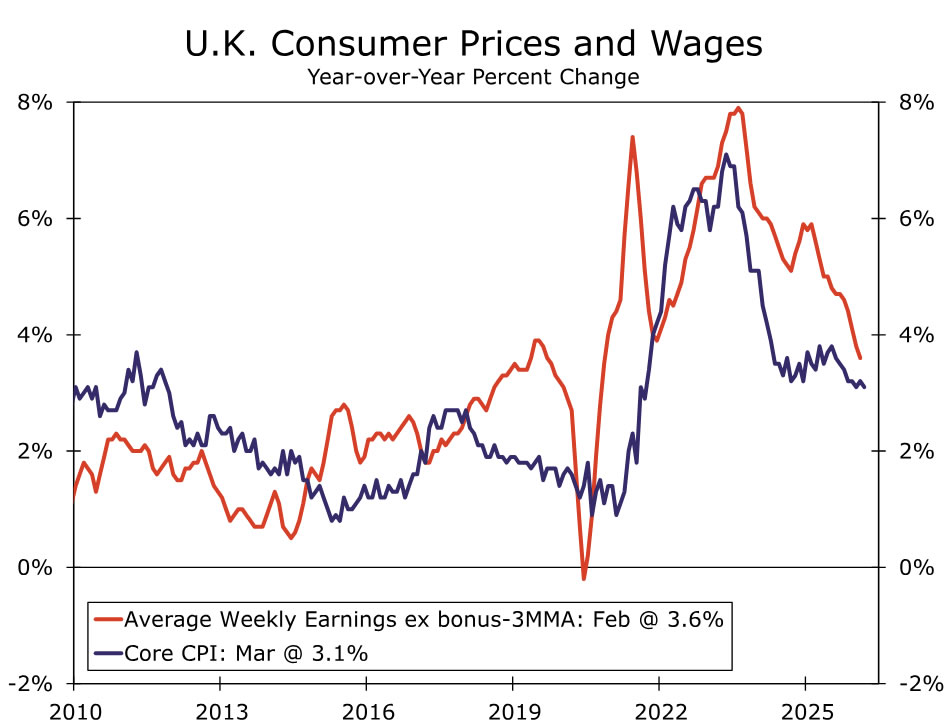

UK Labor Market Overview & CPI • Tuesday & Wednesday

U.K. labor and wage data on Tuesday and April CPI on Wednesday will give market participants a fresh read on wage dynamics and inflationary pressures as Bank of England (BoE) policymakers weigh the appropriate response to an energy-driven price shock against a fundamentally weaker labor market. For the three months to February, average weekly earnings growth eased to 3.8% year-over-year, marking the first sub-4% total pay reading since 2020. The broader labor market has continued to loosen gradually, with vacancies at 711K, the lowest since early 2021, and payrolled employees down 65K on the year in the March early estimate. Pay growth is expected to ease slightly further, though base effects and the recent National Living Wage uplift warrant attention.

Turning to prices, Wednesday’s release follows March’s upside surprise of 3.3% year-over-year, with services inflation at 4.5% and core at 3.1%. The BoE’s April Monetary Policy Report projects headline CPI to ease to 3.0% year-over-year, largely reflecting base effects. Any new upward pressure from energy showing up in the data would therefore require a closer look at the underlying components.

While 2026 public pay awards and the bulk of private sector wage settlements were largely completed before the energy shock and the labor market has visibly loosened, we still see risks to second-round effects skewed to the upside even if they do not show up via the wage channel this year. With energy and fertilizer prices still rising amid the ongoing conflict, the pass-through to core goods and food prices argues for a more pre-emptive stance, in our view. As such, and as noted in our May international outlook, we look for a 25 bps hike to 4.00% in July, with a further Q4 move to 4.25% contingent on Middle East developments.

`

`

EM Week Ahead

China Retail Sales & Industrial Production • Monday

Next week’s retail sales and industrial production data for April will provide an early read on how China’s economy fared at the beginning of the second quarter. China’s economy got off to a solid start in 2026, outperforming expectations, although growth has been somewhat uneven. Strength has been largely driven by firmer manufacturing production, solid external trade performance and front-loaded fiscal stimulus, while domestic demand has remained relatively weak. To that point, March activity data showed some stabilization, with industrial production growth firming to 5.7% year-over-year and retail sales growth rising to 1.7%. However, China’s April PMIs suggest conditions may have softened at the start of Q2, as export-backed manufacturing resilience contrasted with contractions in services and construction. As such, we expect both measures grew at a somewhat slower pace in April and look for year-over-year industrial production growth of 5.9% and retail sales growth of 1.9%.

Looking at the bigger picture, we expect recent strength in China’s economy to gradually abate in the second half of 2026. The boost from fiscal stimulus should fade over time, while higher energy prices and tighter energy supply could become more meaningful headwinds. Accordingly, we look for China’s annual GDP growth to ease to 4.5% in 2026, before slowing further to 4.3% in 2027.

{kind=link}