Dollar is paring back some of this week’s gains as tentative optimism emerges around a possible revival in US–Iran peace talks. The shift in sentiment is modest but notable, with traders dialing down some defensive positioning built earlier in the week. Oil prices are also reflecting this adjustment, with Brent pulling back to around $105 after briefly touching $108 earlier in the day.

The key catalyst is the report that Iranian Foreign Minister Abbas Araqchi is scheduled to arrive at Islamabad tonight, leading a high-level delegation. This development is being interpreted as a key signal that diplomatic channels are reopening after a week of uncertainty.

Pakistan’s role has been critical. Prime Minister Shehbaz Sharif and his mediation team have been actively working behind the scenes to bridge gaps after the first round of talks failed. The fact that discussions have progressed to the point of a physical meeting suggests that backchannel diplomacy has made tangible progress.

In diplomatic terms, such a visit is not symbolic. A foreign minister does not enter a high-stakes negotiation environment without a pre-negotiated framework or at least a baseline for discussion. Araqchi’s arrival suggests that both sides may have moved beyond the earlier stalemate over the 10-point plan.

His profile also matters. Araqchi is widely seen as a pragmatic negotiator, in contrast to the more hardline stance of the IRGC. His involvement signals that Iran’s leadership may be willing to explore a more flexible position, potentially opening the door for progress.

Equally important is the continued US presence in Islamabad. Reports that logistics and security teams remained on the ground even when talks were “on hold” earlier in the week indicate that Washington never fully disengaged. This suggests that neither side is prepared to let the ceasefire collapse outright.

Still, uncertainty remains high. The geopolitical backdrop has not fundamentally changed, with maritime tensions and supply risks in the Strait of Hormuz continuing to underpin oil prices. This limits the extent of risk recovery and keeps markets cautious.

In FX markets, the reaction is measured. Canadian Dollar leads the week so far, supported by oil, while Dollar holds firm despite today’s pullback. Euro continues to lag on weak economic fundamentals, and Yen remains under pressure, though intervention risks persist. Aussie and Kiwi are positioned in the middle.

Overall, markets are positioning carefully, aware that any breakthrough—or breakdown—over the weekend could trigger sharp gaps at the next open.

In Europe, at the time of writing, FTSE is down -0.24%. DAX is up 0.28%. CAC is down -0.41%. UK 10-year yield is down -0.205 at 4.992. Germany 10-year yield is up 0.005 at 3.016. Earlier in Asia, Nikkei rose 0.97%. Hong Kong HSI rose 0.24%. China Shanghai SSE fell -0.33%. Singapore Strait Times fell -0.43%. Japan 10-year JGB yield rose 0.014 to 2.441.

Canada Retail Sales Rise 0.7% in February, Miss Expectations Despite Broad Gains

Canada retail sales rose 0.7% in February, missing expectations, while core sales gained 0.6%. Advance estimate points to another 0.6% increase in March. Read More.

Germany Ifo Falls to 84.4 as Iran Crisis Hits Confidence

German business confidence has dropped to pandemic-era lows as the Iran crisis hits sentiment. The outlook is deteriorating fast. Read More.

UK Retail Sales Rise 0.7% as Fuel Stockpiling Drives March Rebound

UK retail sales rose 0.7% in March, beating expectations as fuel buying surged, while underlying demand remained modest with ex-fuel sales up just 0.2%. Read More.

SNB’s Schlegel Flags Global Uncertainty from Middle East Conflict, Signals Policy Readiness

Rising energy prices are pushing inflation higher—and central banks are watching closely. SNB signals readiness to act. Read More.

Japan’s Core Inflation Rises to 1.8% in March, Core-Core Ticks Down

Japan CPI rises to 1.8% in March but remains below BoJ’s target as core-core inflation slips to 2.4%. Rising oil prices and cost pressures pose risks ahead. Read More.

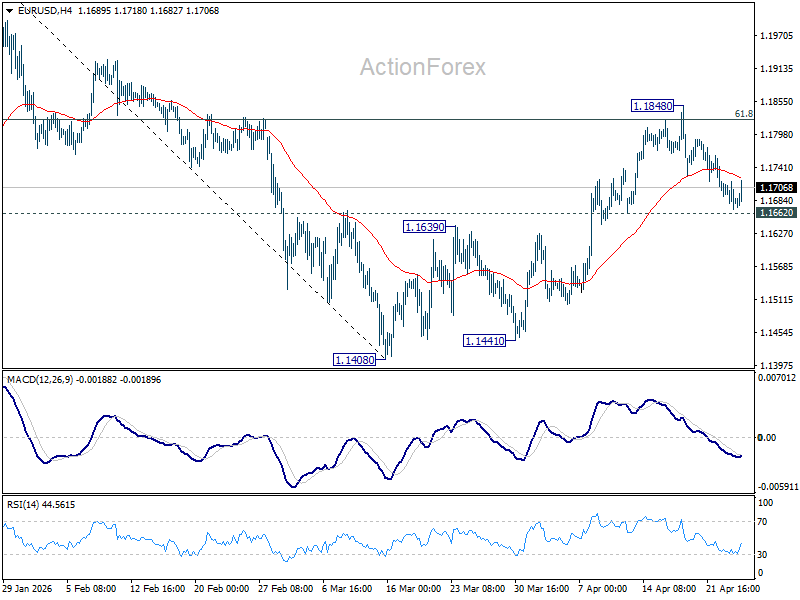

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1663; (P) 1.1691; (R1) 1.1712; More….

EUR/USD recovers ahead of 1.1662 support and intraday bias remains neutral. Further rise is still mildly in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will indicate the the rebound fro 1.1408 has completed, and bring deeper decline back towards this low instead.

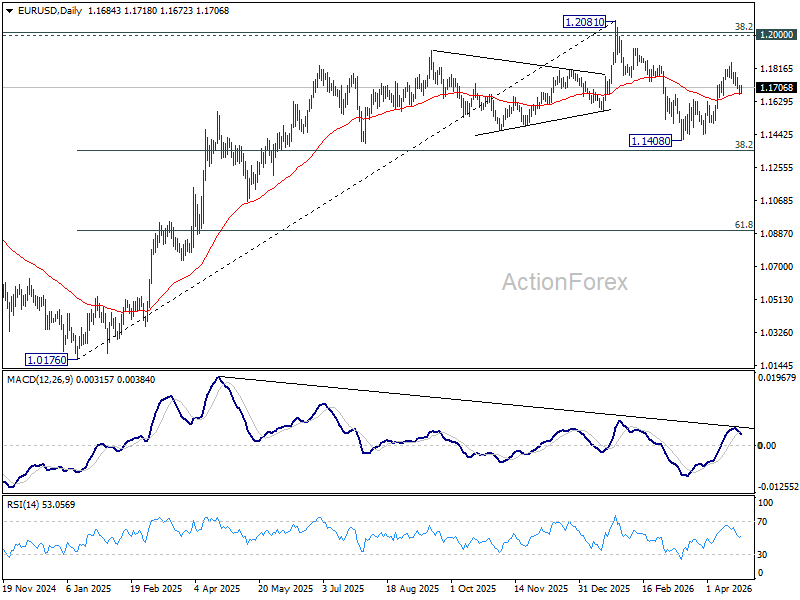

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}