Markets are still trading as though peace is coming — even though not with the same confidence seen at the start of the week. Brent oil prices slipped again today to below $93 as investors continued betting that the United States and Iran are inching closer toward a broader agreement that could eventually reopen the Strait of Hormuz and ease fears of a prolonged global energy shock. But the easy part of the “peace dividend” trade now appears over. Traders are demanding proof before pushing oil sharply lower again.

The most important signal may actually be coming from bond markets rather than oil itself. Treasury yields have eased from their recent highs but are refusing to collapse, suggesting fixed-income traders remain deeply skeptical that inflation risks will disappear quickly. The logic is straightforward: if negotiations fail or energy disruptions intensify again, another inflation shock could rapidly force central banks back into a much more aggressive tightening posture. That is particularly important for Europe, where policymakers increasingly believe the energy shock is already spreading through the broader economy regardless of whether a final Iran deal eventually materializes.

Meanwhile, currency markets reflected widening central bank divergence rather than pure geopolitical positioning. New Zealand Dollar led gains after the Reserve Bank of New Zealand delivered a sharply hawkish hold that surprised markets. Policymakers split evenly 3-3 on whether to raise rates immediately, forcing Governor Anna Breman to use her casting vote to keep the OCR unchanged at 2.25%. The RBNZ also warned that rates would likely need to rise “sooner and by more” than previously projected. That dramatically strengthened expectations that the July meeting is now live for a hike, even though broader market consensus still leans toward September tightening.

Euro also remained firmly bid as senior European Central Bank officials continued preparing investors for a June hike. ECB Executive Board member Isabel Schnabel warned this week that “looking through is no longer an option,” while ECB Chief Economist Philip Lane effectively endorsed tighter market pricing by saying investors did not need “extra guidance.” The key issue for the ECB now is no longer whether inflation will rise — it is whether policymakers can stop energy costs from embedding themselves into wages and broader pricing behavior across the Eurozone economy.

On the other side of the spectrum, Australian Dollar and Canadian Dollar both struggled. Aussie weakened after softer-than-expected April inflation data reduced urgency for another Reserve Bank of Australia rate increase. While markets still see some possibility of an August hike, deteriorating labor-market conditions and easing headline inflation have clearly weakened conviction compared with a week ago. Canadian Dollar also remained under pressure as falling crude prices eroded one of the Loonie’s key macro supports.

Meanwhile, Dollar traded closer to the middle of the performance table, caught between losses against the increasingly hawkish Kiwi and Euro, and support from cautious Treasury markets that still see meaningful inflation risks if Iran negotiations ultimately fail.

EUR/CAD Rally Continues as ECB Officials Prepare Markets for June Hike

EUR/CAD surged as ECB officials increasingly prepared markets for a June rate hike while falling oil prices weakened Canadian Dollar. The widening divergence between Europe’s inflation fears and Canada’s fading commodity support is now becoming one of the main macro themes in FX markets. Read More.

Fed’s Kashkari Warns of Rising Inflation Risks, But Says It’s Too Soon to Predict Rate Hike

Minneapolis Fed President Neel Kashkari warned that inflation risks are “higher, not lower” as the Iran conflict continues pushing energy and supply-chain costs higher globally. But despite rising market bets on a Fed hike later this year, Kashkari said it remains “far too soon” to predict the timing of the next move. Read More.

AUD/NZD Correction Risk Growing After RBNZ and Australia CPI, But Confirmation Still Missing

AUD/NZD tumbled after markets were hit by simultaneous surprises from both sides of the Tasman — a much more hawkish RBNZ hold and softer Australian inflation data. Correction risks are clearly building, but traders are still waiting for the decisive technical breakdown needed to confirm a larger reversal. Read More.

RBNZ Delivers Hawkish Hold as Split Vote Signals Rate Hikes Coming Soon

The RBNZ may have held rates unchanged at 2.25%, but the decision was one of the most hawkish holds in years. A shock 3-3 split vote forced Governor Anna Breman to use her casting vote, while policymakers warned that OCR hikes will likely come “sooner and by more” than previously expected. Read More.

Australia CPI Slows More Than Expected to 4.2% as Fuel Inflation Eases

Softer fuel inflation helped cool Australia’s headline CPI in April, easing immediate pressure for another RBA hike. But trimmed mean inflation climbed to its highest level since mid-2024, reinforcing concerns that underlying price pressures are still proving sticky. Read More.

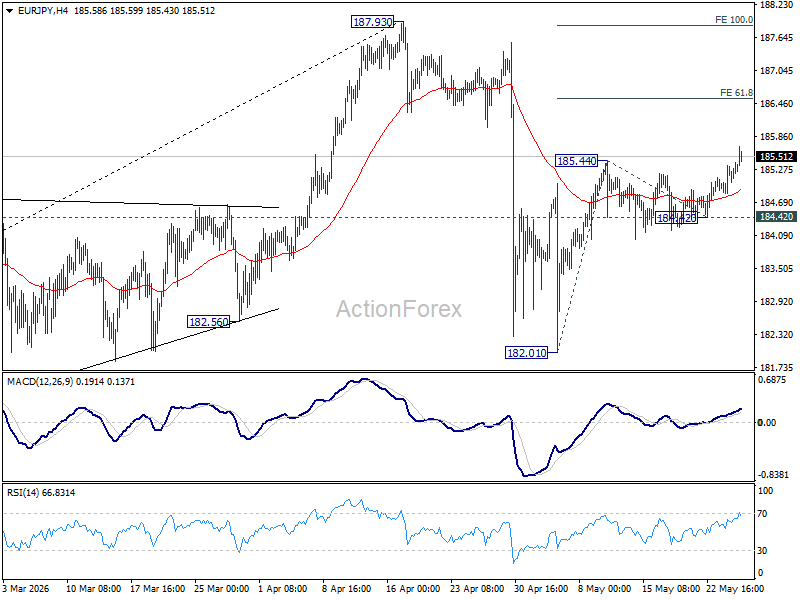

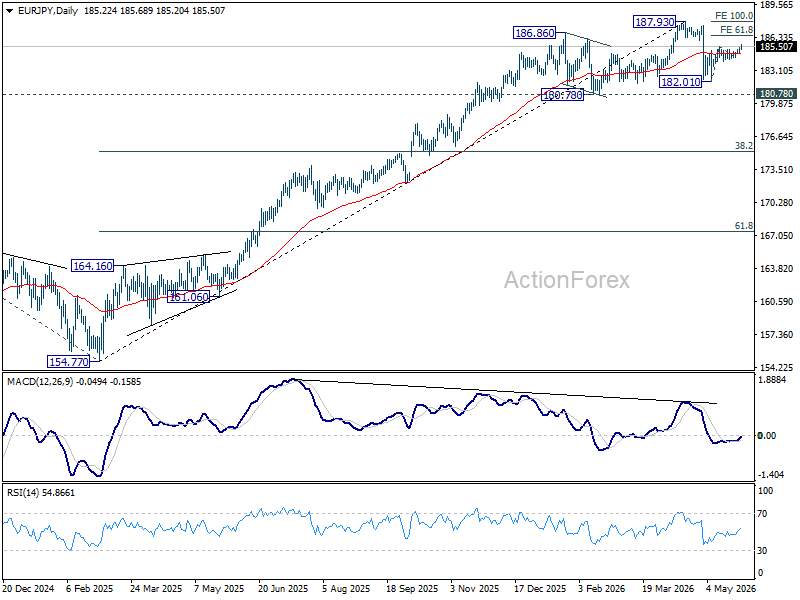

EUR/JPY Daily Outlook

EUR/JPY’s rebound from 182.01 resumed today and intraday bias is back on the upside. Next target is 61.8% projection of 182.01 to 185.44 from 184.42 at 186.53. Near term risk will stay on the upside as long as 184.42 support holds, in case of retreat.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.51) will argue that it’s already in a medium term down trend to 175.41 resistance turned support and below.

{kind=link}