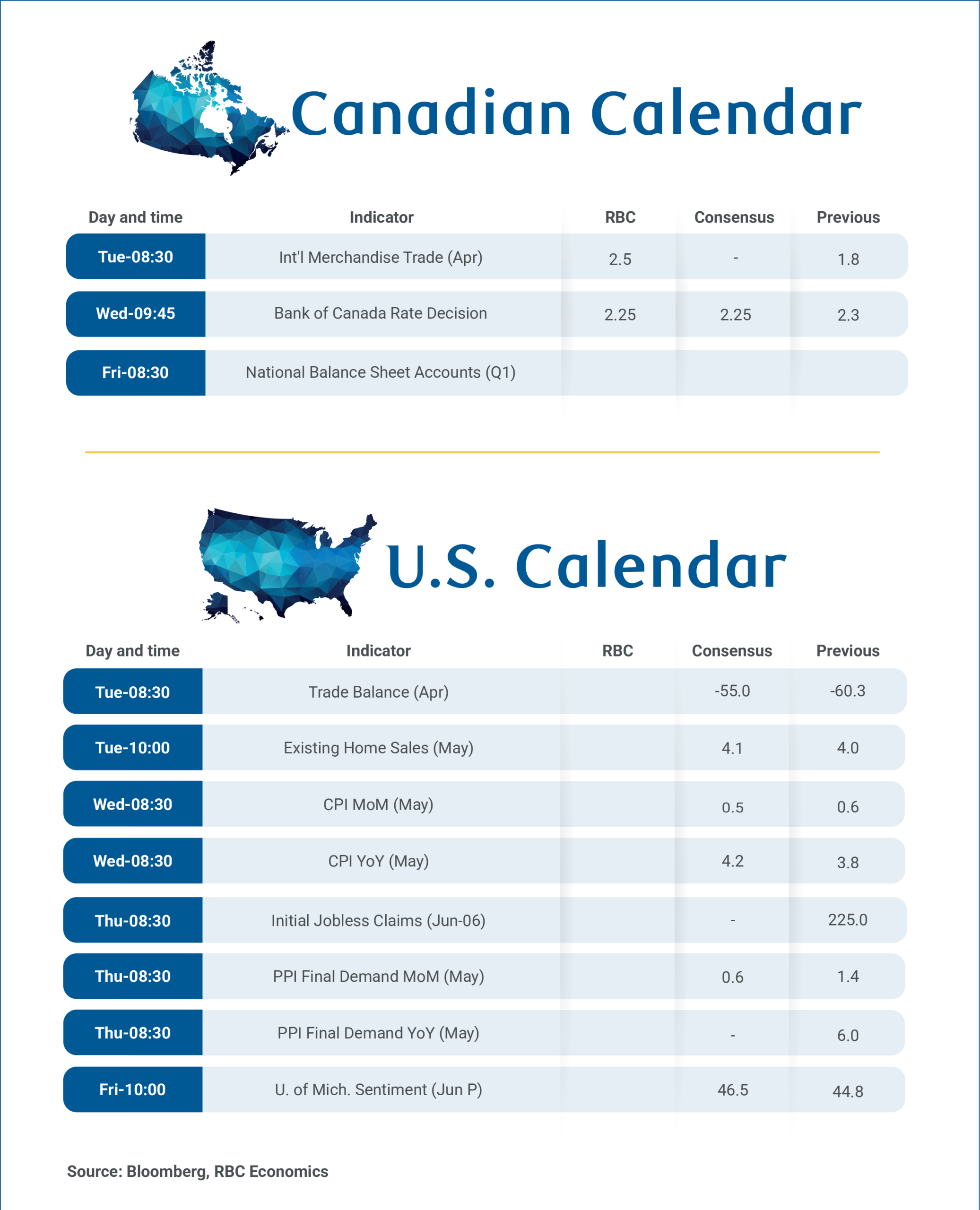

We have some key data releases in the week ahead, but the focus will be on the Bank of Canada’s decision on interest rates on Wednesday where we expect a fifth consecutive hold.

The surge in oil prices has sent inflation back above the central bank’s 2% target. But, there is nothing the BoC can do about global oil prices, and there’s little evidence so far that higher energy prices are filtering into broader measures of underlying inflation. The BoC’s preferred core inflation measures surprised broadly to the downside in April.

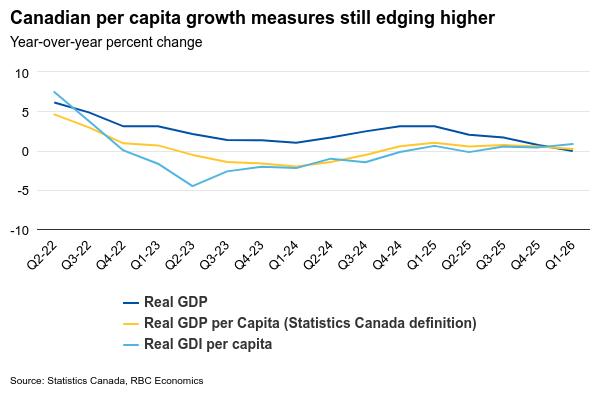

And, growth has also surprised in the same direction. Gross Domestic Product marked a second consecutive quarterly decline, edging down 0.1% annualized in Q1—well below the BoC’s April estimate for a 1.5% increase, building on a 1% decline in Q4.

We continue to think the broader Canadian growth backdrop is more resilient than implied by headline GDP readings. Controlling for a sharp slowing in population, per-capita GDP increased in Q1, and overall consumer spending advanced a solid 1.5%.

Higher oil prices are raising consumer costs, but they are also increasing revenue flowing into the economy. During past periods of large changes in oil prices, the BoC put more emphasis on real gross domestic income—essentially the amount of goods/services that can be purchased with domestic production. That measure rose 2.7% in Q1, because a spike in oil prices means a larger quantity of imports can be purchased with the same quantity of exports.

The unemployment rate in May was 6.6%, down from 6.9% in April but still elevated. Critically, layoffs have continued to decline, but hiring demand has been soft with new labour market entrants still struggling to find work. Hours worked rose 0.6% in May after remaining flat in April, suggesting labour market conditions are improving gradually rather than deteriorating.

That said, there have been enough cracks in growth and labour market data for the BoC to remain cautious about changing policy rates too quickly in one direction or another. We continue to expect the BoC to remain on hold for the rest of 2026 with our current base case forecast expecting the next move to be a hike, but not until 2027 and contingent on growth and the labour market improving into year end.

Canada’s trade report for April on Tuesday is expected to show exports rising 1.1%, while imports remain unchanged, widening the overall surplus to $2.5 billion. Oil prices climbed more than 7% from the prior month, boosting the energy trade balance. Vehicle shipments are also expected to increase, consistent with seasonally adjusted car and truck production data.

Canadian household net worth growth likely remained positive in Q1 2026, though the pace likely slowed from prior quarters in the National Balance Sheet Accounts next Friday. We look for a moderate increase in asset values, supported by a similar rebound in housing values. The CREA Home Price Index rose 0.7% in Q1 (not seasonally adjusted) following three consecutive quarterly declines. Financial asset growth likely paused after robust gains in prior quarters as the S&P 500 declined in Q1 while the S&P/TSX Composite continued to outperform. For liabilities, debt is expected to have grown at a similar pace to Q4, offsetting some asset gains. The debt service ratio is expected to edge slightly higher as debt payments rise and interest income declines alongside lower interest rates.

Headline U.S. CPI growth likely continued to edge higher as prices at the pump continued to increase into May — potentially rising to above a 4% rate for the first time in 3 years. Core will be watched closely given April’s 0.4% m/m jump was driven by a mechanical spike in housing costs related to the government shutdown, though underlying core services inflation (excluding shelter) showed signs of continued acceleration.

{kind=link}