We affirm our previously published view that the RBA will remain on hold in June, but increase rates in coming months given inflation risks.

- We affirm our existing expectation that the RBA Monetary Policy Board (MPB) will hold the cash rate steady at its June meeting next week. Although inflation remains above target, the previous three rate increases have given the MPB time to assess cross-cutting trends of weak consumers and housing markets versus high inflation pressures and a secular boom in data centres and related investment. The recent run of inflation and labour market data has been a bit mixed, supporting the case for a pause.

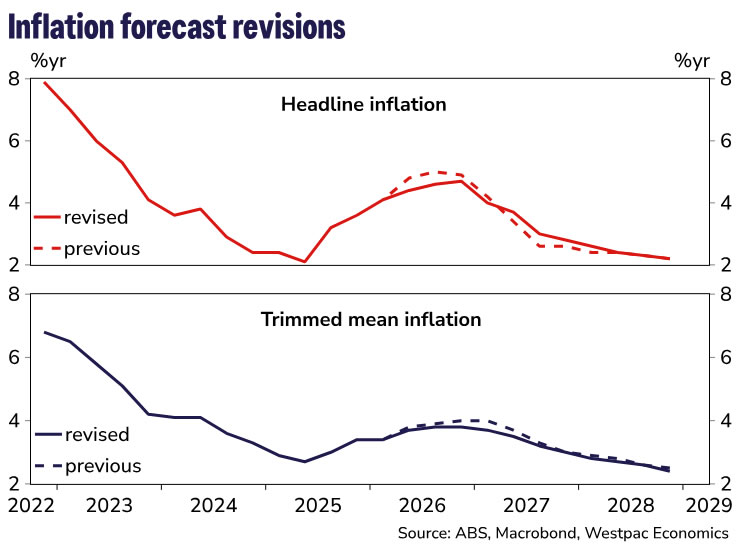

- We update our inflation forecasts below, ahead of the release of our June Market Outlook publication later today. A lower peak for oil, and thus petrol and diesel, prices lowers the peak for headline inflation from 5.0% to 4.7%. Trimmed mean inflation is revised marginally lower across Q2, Q3 and Q4, lowering the peak in the year-ended rate from 4.0%yr to 3.8%yr. We continue to see significant pass-through from higher fuel costs into some other prices. In addition, the larger-than-expected increase in award wages will add a little to some market services components of the CPI, where labour costs are particularly important and many workers are on awards.

- This slightly lower track for underlying inflation is still higher than the RBA’s own forecasts. If we are right about the inflation profile from here, the RBA will be surprised on the upside. We therefore retain our view that further rate hikes will occur in the following meetings (August and September). This is consistent with the RBA’s priority to get inflation down. While ever inflation trends are this far away from the 2.5% target midpoint and showing little tendency to decline, the MPB will regard soft outcomes for the consumer and housing sectors as being a necessary part of the transmission of monetary policy.

- The risks are clearly on the downside, though, in the sense that zero or one further hike is much more likely than three hikes. A more extended pause would be associated with a smaller overall hiking cycle.

While markets are increasingly pricing a faster resolution, our base case for the reopening of the Strait of Hormuz and Gulf oil supply normalisation remains broadly unchanged. We continue to assume shipping rises to around 10% of normal levels by end-June, with full normalisation not occurring until mid-2027.

Q2 average Brent spot and dated prices are tracking below our baseline assumptions of US$110 and US$125 respectively, reflecting a decline in supply risk premia following the ceasefire and a less tight crude balance than anticipated. Stronger-than-expected US exports and weaker Chinese import demand have provided a near-term buffer, though prices have remained volatile amid shifting headlines.

We have lowered our price assumptions through Q2–Q4 2026, with the largest downgrade in Q3 (–US$13/bbl) and a smaller adjustment in Q4, while leaving 2027 broadly unchanged. Prices are likely to fall, potentially below US$90/bbl, on confirmation of a deal and the resumption of shipping, before it becomes evident that the pace of normalisation in traffic and Gulf production will be gradual. The Q2 buffer from US exports is unlikely to persist, while some recovery in Chinese demand is expected. Beyond 2026, we continue to assume a gradual normalisation in shipping and production, alongside a rebuild in global strategic reserves from H2 2027.

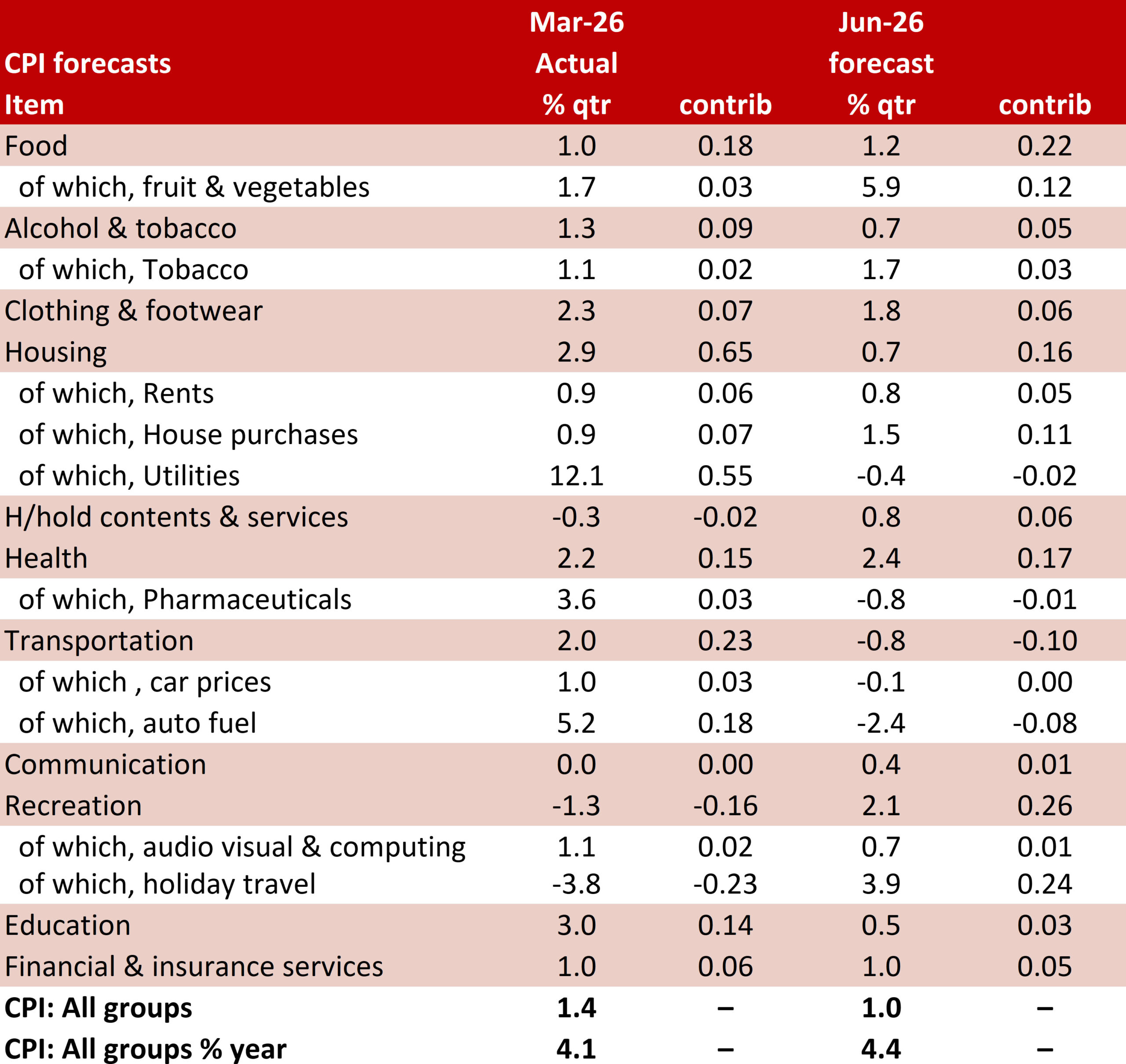

Petrol and diesel price assumptions have been revised materially lower across Q2–Q4 2026, reflecting the softer oil price backdrop. The largest adjustments occur in Q3, where petrol is down around 20c/l and diesel close to 100c/l, averaging $2.05/l and $2.39/l respectively.

Following on from these revisions, we have lowered the near-term inflation profile which is partly offset by a stronger wages outlook feeding into market services.

Headline inflation is expected to reach 4.4%yr in Q2 and peak later at 4.7%yr in Q4 (previously 5.0%yr in Q3). Base effects see a more gradual easing thereafter in year-ended terms, with inflation reaching 2.8%yr by end-2027 and 2.2%yr by end-2028.

Trimmed mean inflation has also been revised lower, reaching 3.7%yr in Q2 before peaking at 3.8%yr in Q3 and holding through Q4 (down from 4.0%yr). The quarterly path for the remainder of 2026 is 1.0%, 1.1% and 0.9% – the H2 2026 profile sits slightly above that implied by the RBA’s May Statement on Monetary Policy forecasts. Trimmed mean inflation is expected to return to the RBA’s target band by end-2027 (3.0%yr) and ease to 2.4%yr by end-2028.

While the near-term profile is lower, the risk of second-round effects from higher fuel costs to broader prices remains. Current policy measures are dampening the pass-through, but with most of these set to expire by the end of June, the bulk of the impact from higher freight costs still lies ahead. Additionally, the impact of higher fertiliser costs will likely feed through in the second half of this year with industry surveys showing growers are scaling back planting schedules in response to higher input costs. Drier weather conditions, with the risk of a more severe El Niño, also adds upside pressure.

They key downside risks to our profile stem from weaker consumer demand that limits firms’ ability to pass through higher costs and a faster-than-expected normalisation of shipping through the Strait of Hormuz.

The RBA faces a difficult set of trade-offs in its near-term monetary policy decisions. As well as the more benign developments in energy prices and the conflict more broadly, some domestic data releases have been softer than generally expected. Consumer spending looks to have stalled, tax changes have induced uncertainty in the housing market, and sentiment surveys have weakened. Weak GDP reads are likely in coming quarters.

At the same time, Australia started the year with inflation too high, and the second-round inflation response to higher energy prices is becoming more evident in the data. While the RBA has already tightened policy in response to the lift in inflation that pre-dated the Middle East conflict, business surveys and other information suggest that the pass-through of higher energy prices to other prices has been significant and front-loaded. Contention for resources to construct the pipeline of data centres – an investment boom largely impervious to interest rates – will add to cost pressures.

We continue to expect that the RBA will pause at its June meeting as it assesses the data flow. However, we believe it will remain focused on getting inflation back down to target and will be less swayed by some of this softer data than some observers might assume. Indeed, it is likely that it views the softer data as being a necessary part of the transmission of restrictive monetary policy. Trimmed mean inflation is drifting up, and even after revising the outlook for the somewhat better oil price trajectory, our base case remains higher than the RBA’s May forecasts through the rest of this year. Pass-through is starting to become evident in categories such as home-building costs, dining out and postal and courier services.

Because our inflation forecast is above the RBA’s most recent published forecast, it implies that the RBA will receive an upside surprise in coming months. This implies further rate hikes as the second-round inflation impact of the energy price shock emerge. Given the weaker outlook for the household sector, risks are skewed to the downside, in the sense that zero or one hike from here is much more likely than three hikes. We still regard our two-hike track as the most appropriate base case view, given the inflation outlook.

{kind=link}