The Federal Reserve has been handed valuable breathing room by two consecutive downside inflation surprises, but the same cannot be said for other major central banks. Softer-than-expected US CPI and PPI confirmed that inflation pressures eased materially through the end of the second quarter, allowing policymakers to remain patient rather than rush into another rate increase. Yet that benign inflation picture is already being challenged by renewed escalation in the Middle East, with Brent crude holding around $85 after fresh US military action against Iran revived concerns over global energy supplies.

June’s inflation data painted a consistent picture of cooling price pressures before oil prices rebounded. Consumer inflation undershot expectations, while producer prices unexpectedly fell -0.3% on the month. The weakness was concentrated in final demand goods, which declined 1.4%—their largest monthly fall since July 2022—as energy prices dropped sharply. Taken together, the reports suggest the Fed now has considerable room to maintain its data-dependent approach. Markets have largely abandoned expectations of an imminent rate hike, with attention shifting instead to whether the latest oil rally proves temporary or develops into a more persistent inflation shock over coming months.

That question has become increasingly difficult to answer after the conflict between the US and Iran intensified again. US Central Command launched another wave of strikes on Iranian military targets on Wednesday morning after President Donald Trump warned that attacks would become progressively heavier unless Tehran cooperates in peace negotiations. The stated objective was to further degrade Iranian capabilities used to threaten commercial shipping through the Strait of Hormuz. Trump’s remarks also suggested military operations could extend into next week without diplomatic progress, reinforcing expectations that geopolitical risks will remain elevated. Although Brent has climbed sharply, its gains have been measured rather than disorderly, indicating markets still expect both sides to keep the conflict within manageable limits rather than allow a full-scale regional war.

That distinction is particularly important for Europe. With the ECB meeting just days away, policymakers are once again confronting the risk that higher energy prices could delay the return of inflation toward target. Bundesbank President Joachim Nagel warned today that the renewed conflict demonstrates how “the situation remains extremely volatile” and reiterated that monetary policy should “react with caution, but act decisively if necessary.”

Currency markets increasingly reflect these diverging policy dynamics rather than classic risk sentiment. New Zealand Dollar continues to outperform after hawkish RBNZ commentary, Canadian Dollar is benefiting from stronger oil prices and the prospect of a firmer BoC, while Dollar, Yen and Swiss Franc lag despite escalating geopolitical tensions. The message is that softer US inflation has bought the Fed time, but higher oil prices are beginning to tighten the policy constraints elsewhere.

Silver Risks Falling to $50 as Dollar Holds Firm and Solar Demand Shifts

Silver’s failure to rally after a softer-than-expected US CPI report suggests the market is facing more than just a temporary macro headwind. A resilient US Dollar, muted buying interest and the emergence of copper substitution in solar manufacturing are combining to weaken the outlook, leaving $50 increasingly in focus if key support gives way. Read more.

USD/CAD to Test Key Support Around 1.4 as Three Tailwinds Boost Loonie Ahead of BoC

The Canadian Dollar is drawing support from three independent macro drivers ahead of the Bank of Canada’s policy decision: softer-than-expected US inflation has weakened the Dollar, Brent crude above $86 is improving Canada’s terms of trade, and markets are increasingly pricing a more hawkish BoC outlook. Together, they have pushed USD/CAD toward the key 1.40 support zone, where today’s policy communication could determine the next major move. Read More.

US PPI Misses Forecasts as Energy Prices Drive Biggest Goods Decline Since 2022

US producer prices unexpectedly fell 0.3% in June, reinforcing the softer inflation message from Tuesday’s CPI report. The decline was driven by a 6.4% drop in energy prices, including a 12.0% plunge in gasoline, producing the largest fall in final demand goods since July 2022. Together, the reports suggest inflation cooled materially before the latest rebound in oil prices. Read More.

Eurozone Industrial Production Unexpectedly Falls -0.2% MoM as Manufacturing Recovery Stalls

Eurozone industrial production fell -0.2% in May, missing expectations for growth and signalling that the region’s manufacturing recovery remains uneven. While energy output rose 2.2% and capital goods production increased 0.3%, declines in intermediate goods and durable consumer goods pulled overall factory output lower. Read More.

China’s Economy Slows to 4.3%, Weakest Growth Since 2022 Despite June Data Beat

China’s economy expanded 4.3% year-on-year in the second quarter, missing expectations and marking its weakest growth since 2022. While industrial production accelerated to 5.3% and retail sales returned to growth at 1.0% in June, the recovery remained uneven as fixed asset investment deteriorated and property investment fell 18% in the first half of the year. Read More.

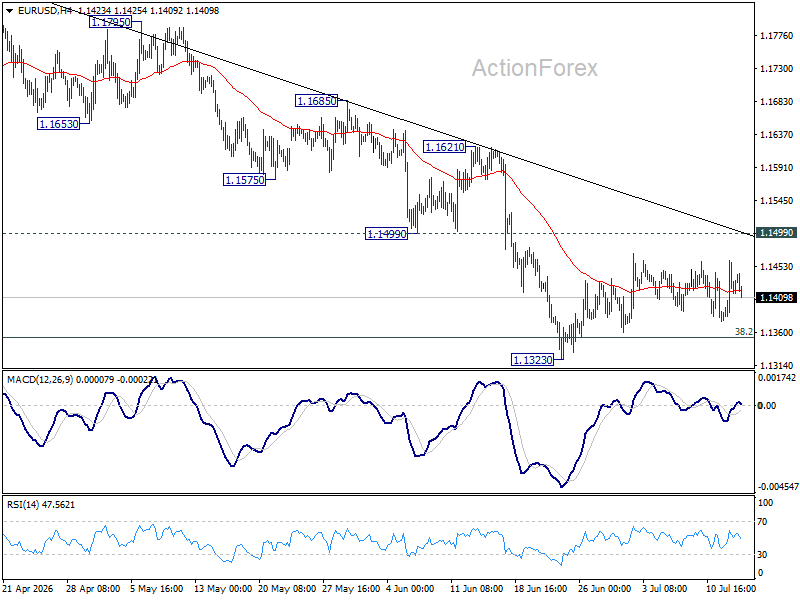

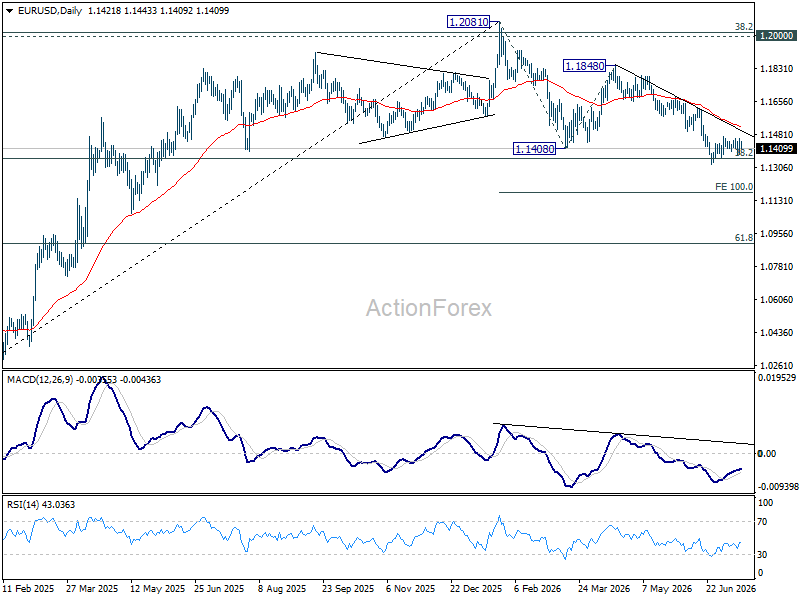

EUR/USD Daily Outlook

Intraday bias in EUR/USD remains neutral for the moment as consolidations continue above 1.1323. With 1.1499 support turned resistance intact, further decline is expected. On the downside, break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. However, decisive break of 1.1499 will turn bias back to the upside for 1.1621 resistance.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

{kind=link}