Australian Dollar is lifted broadly today after stronger than expected GDP data. But the Aussie quickly pared gains as weighed down by stock market rout in Asia. At the time of writing, Hong Kong HSI leads the decline by falling -1.65%. China Shanghai SSE is down -0.92%, Singapore Strait Times is down -0.81% while Nikkei is down -0.25%. Yen has little reaction to risk aversion though, and is trading as the weakest one for today. Dollar follows as the second weakest as the rally attempt yesterday was halted by dovish comments from Fed Kashkari. Canadian Dollar is mixed as BoC rate decision is awaited.

One development to note is the broad based strength in US treasury yields, in particular at the long end. 30 year yield rose 0.059 to 3.069 overnight. 10 year yield rose 0.049 to 2.902. Five year yield rose 0.040 to 1.46%. Resurgence in US yields could put extra strains to emerging markets. US stocks closed down slightly with DOW dropped -0.05%, S&P 500 down -0.17% and NASDAQ down -0.23%. Problems in other parts of the world are not affecting US investors.

Technically, EUR/USD defended 1.1529 support well and recovered. There is no confirmation of completion of rebound from 1.1300. But the pair might have another go at this 1.1529 later today. USD/CHF’s rebound was also limited below 0.9775 resistance, thus, didn’t indicate reversal. Another development to watch is European Yen crosses. EUR/JPY and GBP/JPY recovered after yesterday’s dip. But upside were limited below 129.83 and 144.20 minor resistance levels. Thus, more decline is in favor in these two crosses. We’ll see if there is renewed selling in European session.

Fed Kashkari: We’re raising interest rates too aggressively

In an interview with MarketPlace, Minneapolis Fed President Neel Kashkari openly reiterated his view that Fed is “raising interest rates too aggressively”. And he warned that “we might keep raising interest rates and the economy can’t take it and we put the country into recession.” And for now, he added that “I don’t see any indication that we’re running above potential so let’s let it keep running and if we start to see signs that it’s overheating we can always raise rates then.” Kashkari admitted there an “honest disagreement about this very fundamental question” with his Fed colleagues.

He also pointed out Fed got “scarring” from financial crisis. And the bigger one was from the “inflation of the 1970s”. The scarring is the reason so biased towards high inflation. While Fed said it’s having a “a symmetric view of inflation”, in what it actually does, Kashkari said, “we are much more worried about high inflation than we are low inflation.”

On the cause of the next financial crisis, Kashkari said it could be “a spark in emerging markets” like Turkey. Or it could be Fed, overdueing interest rates or overdoing interest rates. And, “it could be something coming from the trade battles that are being taken right now.

Fed: US firms repatriated USD 300B offshore funds after tax cut, but not for investment

In a note titled “U.S. Corporations’ Repatriation of Offshore Profits“, Fed studied how companies used the cash holdings outside the US after the Tax Cuts and Jobs Act. Under the new act, tax disincentives on the repatriation of foreign earnings were eliminated. Fed found that US firms repatriated just over USD 300B in Q1 2018, roughly 30% of the estimated stock of offshore cash holdings. However, funds repatriated in Q1 have been associated with a dramatic increase in share buybacks only. And, evidence of an increase in investment is less clear at this stage.

After the passage of the TCJA, hare buybacks spiked dramatically for the top 15 cash holders, which accounted for roughly 80% of total offshore cash holdings. However, there is no obvious spike in investment among the top 15 cash holders in Q1 relative to the previous quarter. And, the top 15 cash holders were net sellers in 2018:Q1, with their total securities holdings, mostly in US fixed-income securities, falling by about 3 percent of their total assets.

Canada Trudeau firm on Chapter 19 as talk with US to resume

Canada-US trade talk is set to resume today. Ahead of that, Canadian Prime Minister Justin Trudeau appears to be firm on his negotiation stance. He reiterated that “No NAFTA is better than a bad NAFTA deal for Canadians and that’s what we are going to stay with.” And to him, “there are a number of things we absolutely must see in a renegotiated NAFTA.”

One of them is the Chapter 19 dispute resolution mechanism, which Trump is keen to scrap. Trudeau said “we will not sign a deal that is bad for Canadians, and quiet frankly, not having a Chapter 19 to ensure the rules are followed would be bad for Canadians.”

Separately, Mexican Economy Minister Ildefonso Guajardo said he hope there will be “white smoke” for this Friday, as there will be an agreement between the US and Canada. That would pave the way to completing the original trilateral NAFTA.

BoC to stand pat today, and signal October move

Bank of Canada rate decision is a major focus today. Speculation of a September hike cooled drastically as NAFTA negotiation stalled last week. Markets are now generally expecting BoC to hold the overnight rate unchanged at 1.50% today. Instead, markets are expecting BoC to signal a move in October. That signal is a key to Canadian Dollar’s near term movement. Meanwhile, negotiation with US will also resume today. But based on Prime Minister Justin Trudeau’s firm stance on Chapter 19 dispute resolution mechanism, it’s unlikely to a break through any time soon.

Suggested readings on BoC and Loonie:

- BOC Preview – Growth Upbeat, Just Not Justifies Another Rate Hike Until October

- BoC To Hold Rates Steady But Signal October Hike? Trade Developments Another Loonie Driver

- The Drivers of the Loonie

Australia GDP grew 0.9% qoq, 3.4% yoy, Aussie lifted briefly

Australian Dollar was lifted notably by better than expected GDP data in Asian session. Q2 GDP rose 0.9% qoq, 3.4% yoy, comparing to expectation of 0.8% qoq, 2.8% yoy. That’s marked the 27th year without recession, and it’s the strongest in almost six years. Chief Economist for the ABS, Bruce Hockman, said: “Growth in domestic demand accounts for over half the growth in GDP, and reflected strength in household expenditure.”

Looking at the details, domestic demand rose 0.6% qoq, government expenditure rose 1.0% qoq, new dwelling investments rose 3.6% qoq. However, employee compensation grew only 0.7% qoq “due to a rises in the number of wage and salary earners and wage rates.”

The lift to Aussie is relatively brief however. While the GDP figure was strong, it’s not enough to trigger even a rethink of interest path of RBA. Policymakers are looking for sign of pick up of wage growth.

Also released, Australia AiG performance of services index dropped -1.4 to 52.2 in August. New Zealand ANZ commodity price dropped -1.1% in August. China PMI services dropped to 51.5 in August, down from 52.8.

Elsewhere

Services PMI will be the main focuses in European session. Eurozone will release services PMI final. UK will also release services PMI. Later in the day, US will release trade balance. Canada will release trade balance and labor productivity, as well as BoC rate decision.

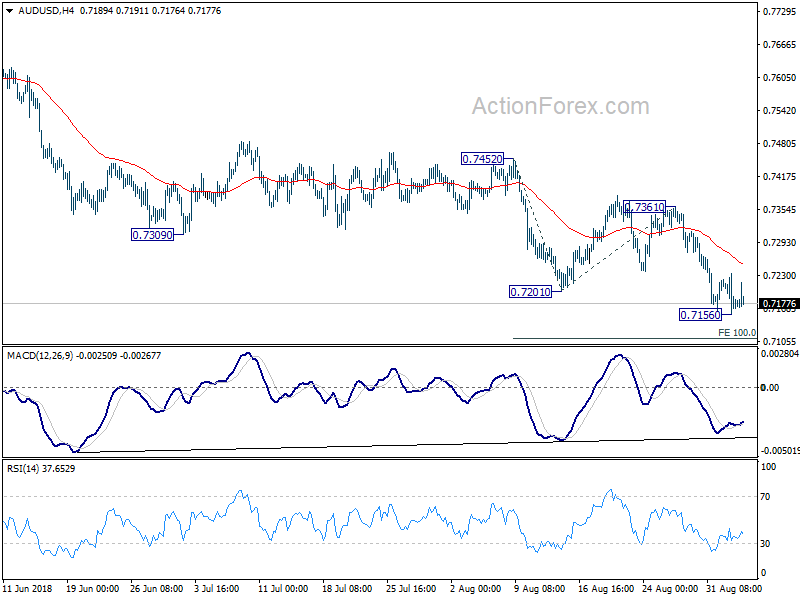

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7144; (P) 0.7190; (R1) 0.7222; More…

Despite dipping to 0.7156, AUD/USD quickly lost momentum again and recovered. Intraday bias stays neutral first and more consolidation might be seen. In case of stronger recovery, upside should be limited well below 0.7361 resistance to bring fall resumption. On the downside, break of 0.7156 will target 100% projection of 0.7452 to 0.7201 from 0.7361 at 0.7110. Break will target 161.8% projection at 0.6955.

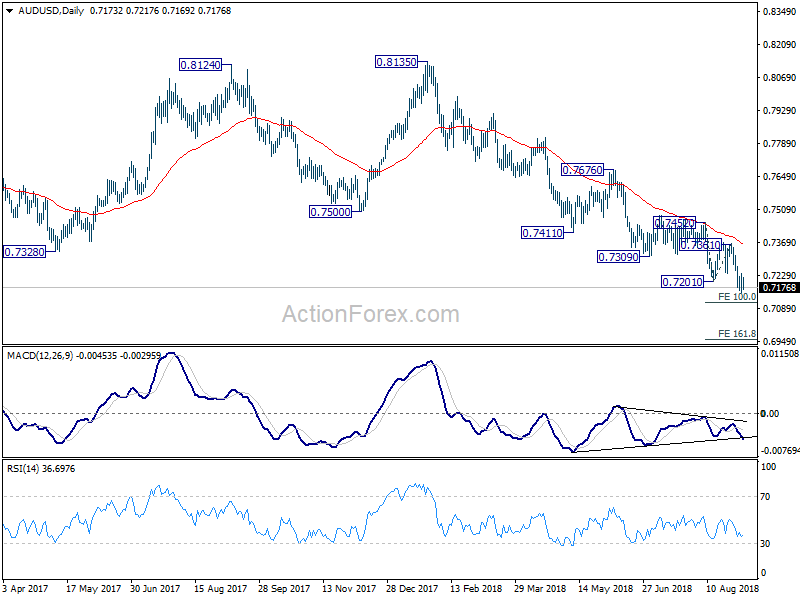

In the bigger picture, rebound from 0.6826 (2016 low) is seen as a corrective move that should be completed at 0.8135. Fall from there would extend to have a test on 0.6826. There is prospect of resuming long term down trend from 1.1079 (2011 high). But we’ll look at downside momentum to assess at a later stage. On the upside, break of 0.7452 resistance, however, will indicate medium term bottoming, on bullish convergence condition in daily MACD. In that case, a medium term correction should be seen first before down trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Service Index Aug | 52.2 | 53.6 | ||

| 1:00 | NZD | ANZ Commodity Price Aug | -1.10% | -3.20% | -3.30% | |

| 1:30 | AUD | GDP Q/Q Q2 | 0.90% | 0.80% | 1.00% | 1.10% |

| 1:30 | AUD | GDP Y/Y Q2 | 3.40% | 2.80% | 3.10% | |

| 1:45 | CNY | China PMI Services Aug | 51.5 | 52.7 | 52.8 | |

| 7:45 | EUR | Italy Services PMI Aug | 53.2 | 54 | ||

| 7:50 | EUR | France Services PMI Aug F | 55.7 | 55.7 | ||

| 7:55 | EUR | Germany Services PMI Aug F | 55.2 | 55.2 | ||

| 8:00 | EUR | Eurozone Services PMI Aug F | 54.4 | 54.4 | ||

| 8:30 | GBP | Services PMI Aug | 53.9 | 53.5 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Jul | -0.10% | 0.30% | ||

| 12:30 | CAD | Trade Balance (CAD) Jul | -0.8B | -0.6B | ||

| 12:30 | CAD | Labor Productivity Q/Q Q2 | 0.20% | -0.30% | ||

| 12:30 | USD | Trade Balance (USD) Jul | -47.6B | -46.3B | ||

| 14:00 | CAD | BoC Rate Decision | 1.50% | 1.50% |

{kind=link}