Sterling recovers mildly today but remains the weakest one on political turmoil in the UK. There is no clear sign of a come back in the Pound and it remains vulnerable for more selloff, even before weekly close. The markets are rather quiet in Asian overall. Australia, New Zealand and US Dollar are trading as the weakest ones, without much follow through momentum. Yen and Canadian Dollar are the strongest ones. For the week, Sterling is the worst performer, followed by Swiss Franc and then Dollar. New Zealand and Australian Dollar are the strongest.

Technically, selloff in the Pound halted ahead of near term support levels. But theses levels, 1.2692 in GBP/USD, 142.76 in GBP/JPY and 0.8939 in EUR/GBP could be taken out easily on another round of selling. Dollar is engaging in corrective pull back and downside is so far limited. But both USD/JPY and USD/CAD are now risking deeper fall. In particular, 112.94 in USD/JPY is a key near term level to defend.

In other markets, DOW rebounded overnight and closed up 0.83% at 25289.27. S&P 500 rose 1.06% and NASDAQ added 1.72%. 30 year yield closed up 0.014 at 3.368. But 10 year yield closed down slightly by -0.002 at 3.118. In Asia, Nikkei is currently down -0.08%. Hong Kong HSI is up 0.28%. China Shanghai SSE is up 0.88%. Singapore Strait Times is up 0.97%. Gold’s recovery continues and is now back above 1215. WTI crude oil is hovering round 57, consolidating in tight range above 58.84 temporary low.

UK PM May insisted her Brexit plan’s the right one, ready to see through leadership challenge

Sterling recovers mildly today but remains the weakest one for the week on political turmoil in the UK. Four ministers, including Brexit Minister Dominic Raab resigned in protest to Prime Minister Theresa May’s draft Brexit agreement. But May insisted in a press briefing that “I believe with every fibre of my being that the course I have set out is the right one for our country and all our people.” She added that “I am going to do my job of getting the best deal for Britain and I’m going to do my job of getting a deal that is in the national interest.”

ERG leader Jacob Rees-Mogg has formally requested a no-confidence vote on May. And for now, at least 14 Conservative MPs had openly said they had joined in the call. Four-eight letters are needed to trigger a leadership challenge. May’s response regarding the challenge was “Am I going to see this through? Yes.”

Even if May can survive the leadership contest, it remains very doubtful if she can get enough votes through the parliament. Conservative Brexit-supporting MP Mark Francois, put it this way. “It is … mathematically impossible to get this deal through the House of Commons. The stark reality is that it was dead on arrival.”

US still planning to raise tariffs on Chinese goods on Jan despite planned Trump-Xi meeting

US Commerce Secretary Wilbur Ross said in an interview that all the exchanges with China right now are just “preparatory”. And the “big-event” is the meeting between Trump and Xi at the G-20 in Argentina on Nov 30/Dec 1. He added both leaders will certainly not get into “intimate details”. And, it’s going to be “big picture”. If things go well, the meeting will “set the framework for going forward”.

However, Ross also noted that the US is still planning, on Jan 1, to raise tariffs on USD 200B in Chinese imports from 10% to 25%. And “We certainly won’t have a full formal deal by January. Impossible.”

Separately, it’s reported that the document China sent to the US this week included 142 items regarding US requests on trade. The items are divided into three categories: issues for further negotiation, issues China is already working on, and issues that are non-negotiable. It’s believed that some items on the non-negotiable lists were unacceptable to Trump, while the US is skeptical on others due to China’s history of failing promises.

Fed Kashkari sees no need for more rate hikes, Bostic wants to keep going to neutral

Minneapolis Fed President Neel Kashkari reiterated yesterday that he didn’t see the need to continue raising interest rates. And, he saw no signs of overheating while low wage growth suggests the labor market are more slack. He also pointed to slowdown in other major economies, in the context that Japan and Germany GDP contracted in Q3. He questioned “right now, the U.S. economy seems to be the strongest engine of the major economies around the world — is that going to last, especially if the Fed keeps raising rates? It’s hard to know.”

On the other hand, Atlanta Fed President Raphael Bostic maintained his support to keep raising interest rates to neutral, even though they “not too far”. He said “I don’t think we are too far from a neutral policy, and neutral is where we want to be”. And, “We may not be there quite yet, but I am inclined to think that a tentative approach as we proceed would be appropriate.”

BusinessNZ PMI improved, not large but important to broader economic narrative

New Zealand BusinessNZ Performance of Manufacturing Index rose 1.6 to 53.3 in October, indicating faster expansion rate. That’s also the highest level since May. BusinessNZ noted “the October result was a welcome change from where the survey has sat for the previous four months.” And, while “the improvement in the PMI is not large, but we see it as important to the broader economic narrative”.

Looking at the details, the key sub-indicators of production (52.8) and new orders (56.7) both improved with their highest results since May and April respectively. Also, after dipping into contraction during various times in 2018, employment (52.4) improved for a second consecutive month. The proportion of positive comments (58.3%) also increased, with demand for products from offshore customers noted throughout.

Looking ahead

Eurozone October CPI final is the main feature in European session. US will release industrial production later in the day. Canada will release international securities transactions and manufacturing sales.

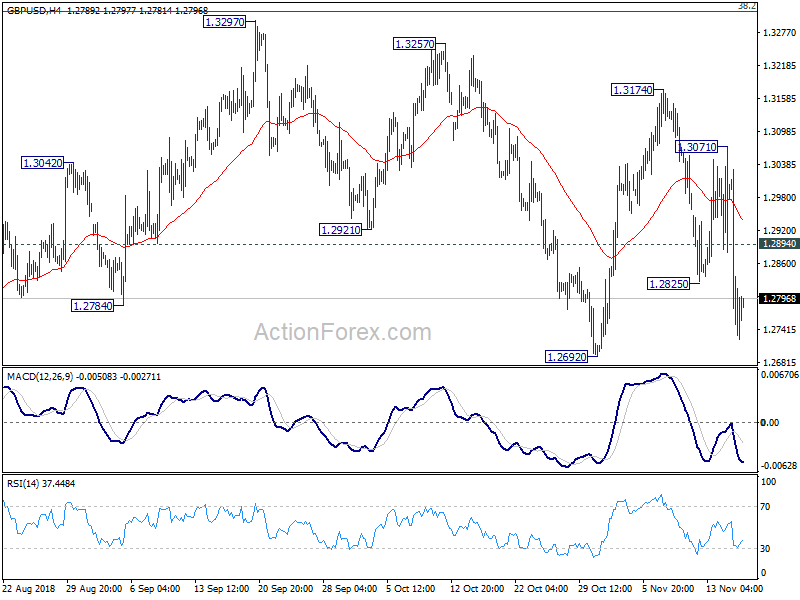

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2656; (P) 1.2843; (R1) 1.2963; More…

Intraday bias in GBP/USD remains on the downside for 1.2692 support. first. Break will target 1.2661 low next. Decisive break there will resume larger down trend from 1.4376. On the upside, break of 1.2894 minor resistance will probably bring another rebound. But upside should be limited by 1.3316 fibonacci level. Overall, price actions from 1.2661 are viewed as a consolidation pattern. Down trend from 1.4376 should resume after completion of the consolidation.

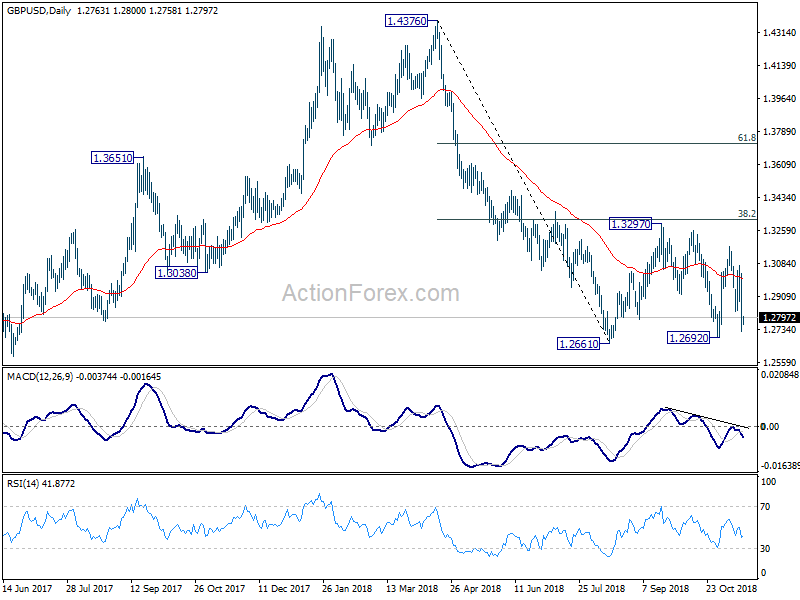

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing PMI Oct | 53.5 | 51.7 | 51.9 | |

| 10:00 | EUR | Eurozone CPI M/M Oct | 0.20% | 0.50% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 2.20% | 2.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 1.10% | 1.10% | ||

| 13:30 | CAD | International Securities Transactions (CAD) Sep | 2.82B | |||

| 13:30 | CAD | Manufacturing Sales M/M Sep | -0.40% | |||

| 14:15 | USD | Industrial Production M/M Oct | 0.20% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 78.30% | 78.10% | ||

| 21:00 | USD | Net Long-term TIC Flows Sep | 131.8B |

{kind=link}