New Zealand and Australian Dollar are trading as the strongest ones today so far, following rebound in Asian stocks. Nevertheless, both currencies are generally limited below last week’s highs, indicating unconvincing upside momentum for now. Indeed, sentiments did turn more positive on US-China trade talks. But there are enough risks for investors to worry about. An imminent one is UK Prime Minister Theresa May’s political downward spiral and whether she’d be ousted very soon. For today, Yen is the weakest one, followed by Dollar.

Technically, AUD/USD is still struggling in very tight range around 0.7199 support. It’s more likely to head downwards on breakout, then upwards. GBP/USD’s decline extends in Asia today but EUR/GBP and GBP/JPY are held in tight range. More time is needed to digest this week’s selloff in Pound. A focus for today is whether EUR/USD and EUR/JPY would finally have a downside breakout in recently established range. 1.1267 in EUR/USD and 127.49 in EUR/JPY are the levels to watch.

In other markets, US stocks ended mixed overnight. DOW closed down -0.22% at 24370.24. S&P 500 also dropped -0.04% to 2636.78. But NASDAQ closed up 0.16% at 7031.83. 10-year yield rose up 0.023 at 2.879. But yield curve flattened at the long end with 30 year yield closed flat at 3.129. Also, 3-year yield (2.763) and 5-year yield (2.743) remains inverted. In Asia, Nikkei is trading up 1.96%, Hong Kong HSI up 1.54%, China Shanghai SSE up 0.20%, Singapore Strati Times up 0.88%. 10 year JGB yield is also up 0.0052 at 0.051. Investors seem cautiously optimistic.

Trump: Fed Powell’s a great guy, just far too aggressive

In a Reuters interview, Trump toned down his rhetorics against Fed chair Jerome Powell and said he’s a “great guy”. Though, Trump still disagree to Fed’s “foolish” rate hike next week.

Trump said, “Well, I think that would be foolish but what can I say? What can I say? You know, I put a man there. What can I say? If they do that, I’d be disappointed and I think a lot of people would be disappointed.” On Powell, Trump said, “I think he’s trying to do what he thinks is best. I disagree with him – I think he’s a great guy. But, I think he’s trying to get it right but I think he’s being too aggressive, far too aggressive, actually far too aggressive.”

Trump may intervene in Huawei case for trade deal

On trade negotiation with China, Trump said the Chines are “back in the market” buying “tremendous amounts of soybeans”. He added there maybe another meeting of “top people on both sides”. And, if necessary, Trump is open to another meeting with Xi “who I like a lot and get along with very well”.

Trump went further and said that he could intervene in the Huawei case if it’s good for the trade deal. He said “If I think it’s good for the country, if I think it’s good for what will be certainly the largest trade deal ever made – which is a very important thing – what’s good for national security – I would certainly intervene if I thought it was necessary.”

Separately, Huawei’s top executive Meng Wanzhou, arrested by Canada on December 1 on US request, was granted bail by a Canadian court yesterday.

UK PM May’s EU tour ended with nothing, to face leadership challenge ahead

Pressures have been mounting on UK Prime Minister Theresa May after she called off the Brexit parliamentary vote. Her meeting with European leaders appeared to be fruitless. After the meeting with May, European Council president Donald Tusk tweeted that “Clear that EU27 wants to help. The question is how.”

Domestically, the campaign to oust May seems to be gathering momentum. BBC cited multiple sources saying that the required 48 letters to 1922 Committee chair Graham Brady for leadership challenge have been reached. And, the vote on May’s leadership could happen at the first opportunity, that is, as soon as tonight in the UK.

Former UK PM Major: Revoke Brexit notice now, the clock must be stopped

Former UK Prime Minister John Major urged the current government to revoke Brexit notice to the EU now. He said, “We need to revoke article 50 with immediate effect. The clock, for the moment, must be stopped.”

He added, “It’s clear we now need the most precious commodity of all: time. Time for serious and profound reflection by both parliament and people. There will be a way through the present morass, there always is.”

Also, he said Brexit will weaken UK’s position in the world. He argued that “We are a more valued ally for America because of our influence in Europe and we are more valued by Europe because of our close relationship with America.” And, “Britain, shorn of both these long-standing allies, will be seen by the world as a mid-sized, middle-ranking power that is no longer super-powered by her alliances.”

Australia Westpac consumer sentiment rose 0.1%, RBA to hold through 2020

Australia Westpac consumer sentiment rose 0.1% to 104.4 in December, up from 104.3.

Westpac Chief Economist Bill Evans noted in the release that the disappointment of just 0.3% Q3 GDP growth is “likely to prompt the RBA to lower its growth forecasts for 2018 and 2019.” Also, “the atmospherics of a central bank forecasting strongly above trend growth is likely to change to one talking more about near trend growth.”

And markets pricing have largely moved towards Westpac’s rate forecast. That is RBA will keep OCR unchanged at 1.50% “over the course of both 2019 and 2020”.

NAB delays RBA hike expectations, falling house price has bigger impact

NAB becomes another bank to delay RBA rate hike expectations. It now expects the first hike to happen in second half of 2020. It noted that “ages pressure remains weak and hence inflationary pressure has remained low.” And, core inflation would continue to “track below RBA’s target band” through all of 2019.

And, there would be a “moderation in growth back to potential of around 2.3 to 2.5%”. And, “falling house prices suggest a bigger impact on housing construction than previously incorporated and additional concerns about the consumer, though low rates and unemployment are important offsets.”

Elsewhere

Japan domestic CGPI rose 2.3% yoy in November, below expectation of 2.4% yoy. Machine orders rose 7.6% mom in October, below expectation of 10.2% mom. Eurozone will release industrial production in European session. Later in the day, US CPI will be the major focus.

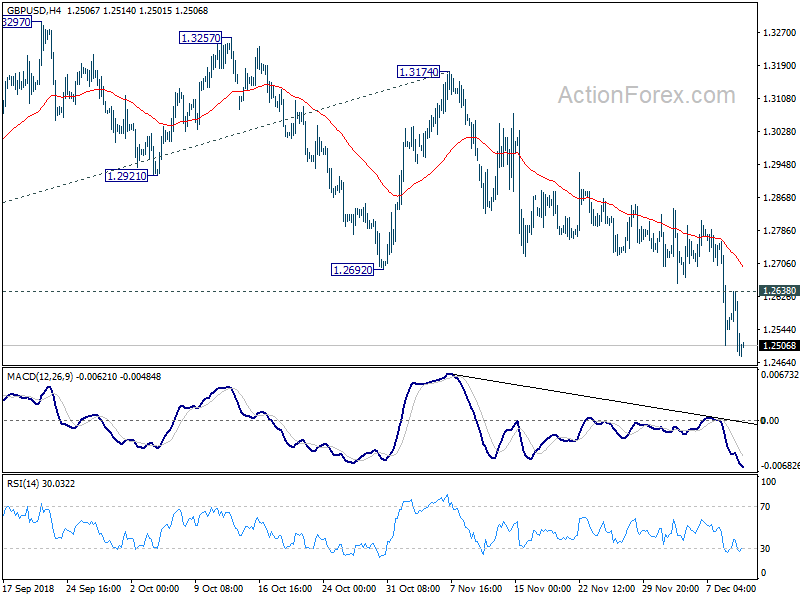

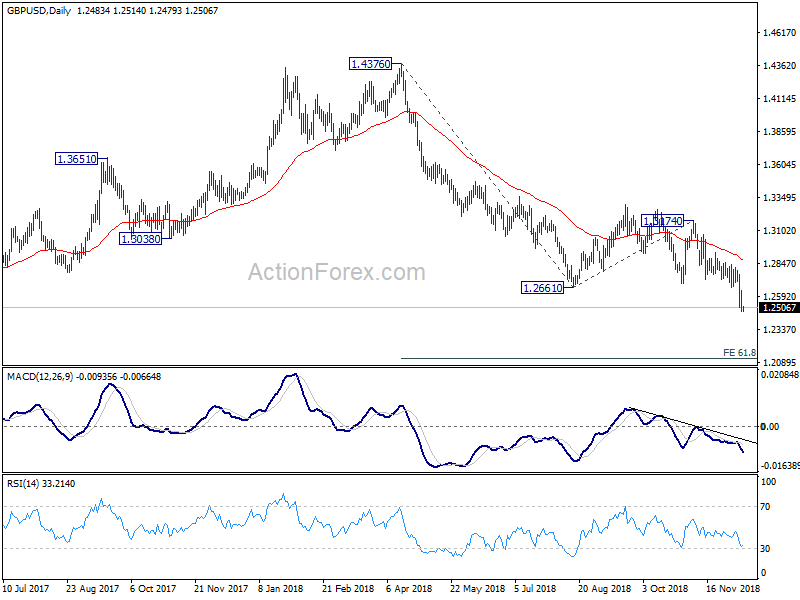

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2458; (P) 1.2609; (R1) 1.2710; More…

GBP/USD’s decline resumed after brief consolidation and reaches as low as 1.2479 so far. Intraday bias remains on the downside. Current fall is part of the down trend from 1.4376. Next target will be 61.8% projection of 1.4376 to 1.2661 from 1.3174 at 1.2114. On the upside, above 1.2638 minor resistance will turn intraday bias neutral and bring consolidation first, before staging another decline.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will now remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should now target a test on 1.1946 first. Decisive break there will confirm our bearish view.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 0.10% | 2.80% | ||

| 23:50 | JPY | Domestic CGPI Y/Y Nov | 2.30% | 2.40% | 2.90% | 3.00% |

| 23:50 | JPY | Machine Orders M/M Oct | 7.60% | 10.20% | -18.30% | |

| 4:30 | JPY | Tertiary Industry Index M/M Oct | 1.90% | 0.90% | -1.10% | -1.20% |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.20% | -0.30% | ||

| 13:30 | USD | CPI M/M Nov | 0.10% | 0.30% | ||

| 13:30 | USD | CPI Y/Y Nov | 2.20% | 2.50% | ||

| 13:30 | USD | CPI Core M/M Nov | 0.20% | 0.20% | ||

| 13:30 | USD | CPI Core Y/Y Nov | 2.20% | 2.10% | ||

| 15:30 | USD | Crude Oil Inventories | -7.3M | |||

| 19:00 | USD | Monthly Budget Statement Nov | -100.5B |

{kind=link}