Dollar selloff takes center stage today as Trump continues with his verbal intervention on Fed policy. But Canadian Dollar is even weakest as down trend in WTI crude oil extends. Swiss Franc is for now the third worst performing one. On the other hand, New Zealand Dollar recovers as is trading as the strongest one. Sterling is the second strongest, followed by Yen, as risk sentiments somewhat stabilized in European session.

In short, Trump tweeted asking asked Fed policy makers to not just go by “meaningless numbers”. Instead, they should “feel the market”. For now, there is no clear follow through selling in Dollar yet. Traders would are eagerly awaiting Fed to release some numbers of economic projection tomorrow, before committing themselves.

Technically, USD/CHF’s break of 0.9911 support is a clear sign of weakness and it’s likely heading back to 0.9862 low. But USD/JPY is trading to find some footing around 112.23 support. EUR/USD, GBP/USD, AUD/USD and USD/CAD are bounded in familiar range. EUR/JPY has yet to break 127.61 support and this level will remain a focus in US session.

In other markets, WTI crude oil hit as low as 48.09 today and is now at 49.07. At the time of writing, FTSE is down -0.46%, DAX is up 0.32% and CAC is down -0.17%. Ranges are pretty narrow. German 10 year yield is down for another day, by -0.0171, at 0.243. Italy 10 year yield is up 0.021 at 2.970. Earlier in Asia, Nikkei closed down -1.82%. Singapore Strait Times dropped -2.21%. Hong Kong HSI dropped -1.05%. China Shanghai SSE dropped -0.82%. Japan 10 year JGB yield dropped another -0.0088 to 0.028.

Released in US session, US housing starts rose to 1.26M in November versus expectation of 1.23M. Building permits rose to 1.33M versus expectation of 1.27M. Canada manufacturing sales dropped -0.1% mom in October versus expectation of 0.3% mom.

German Ifo dropped for fourth month, economy faces a lean festive season

Germany Ifo Business Climate dropped for the fourth straight month to 101.0 in December, down fro 102.0 and missed expectation of 101.7. Current Assessment gauge dropped to 104.5, down from 105.5 and missed expectation of 104.9. Expectations gauge dropped to 97.3, down from 98.7 and missed consensus of 98.2.

Ifo President Clemens Fuest noted in the release that “concern is growing among German businesses”. And, “the German economy faces a lean festive season.” Ifo economist Klaus Wohlrabe said uncertainty had increased again and Brexit was at the top of the agenda. The German economy is cooling but there is no recession in sight.

Italy asked to save EUR 2.5-3B more before getting European Commission approval on 2019 budget

Corriere della Sera daily newspaper reported today that the European Commission has asked Italy to save EUR 2.5 – 3.0B in their 2019 budget before getting approval. However, having cut deficit target from 2.40% to 2.04% of GDP, Italian Economy Minister Giovanni Tria said both Deputy Prime Ministers Matteo Salvini and Luigi Di Maio opposed further cuts.

European Commissioner for Economic and Financial Affairs Pierre Moscovici said today that he’s “been working hard, almost day and night … so that Italy will not be sanctioned either:” He added that “we’re working non-stop as part of a dialogue so that Italy can carry out the policies it wants, while respecting the rules.”

SECO lowers Swiss 2019 growth and inflation forecasts significantly

The State Secretariat for Economic Affairs (SECO) lowered both 2018 and 2019 Swiss growth forecasts significantly. SECO cited that “this is mainly due to weak domestic demand”. Also, “In the wake of the decline in international growth, Swiss foreign trade decreased. The appreciation of the Swiss franc in the meantime additionally slowed exports, while domestic demand also failed to stimulate growth. ”

For 2018, growth projection is lowered to 2.6%, down from 2.9%. For 2019, growth projection is lowered to 1.5%, down from 2.0%. For 2020, growth is now estimated to be at 1.7%. On inflation, for 2018, CPI is projected to be at 1.0%, unrevised. For 2019, CPI is projected to be at 0.5%, down from prior estimate of 0.8%. For 2020, CPI is projected to pickup to 0.7%.

On more thing to now is that SECO’s projection was based on assumption that the three month LIBOR interest rate will climb to -0.5% in 2020.

RBA minutes hint on prospect of dovish shift

Minutes of the December 4 RBA meeting maintained the same tone that “the next move in the cash rate was more likely to be an increase than a decrease”. But at the same time “there was no strong case for a near-term adjustment in monetary policy”.

For RBA, the “central scenario remained for steady growth in consumption, supported by continued strength in labour market conditions and a gradual pick-up in wages growth”. Also, “further falls in the unemployment rate were likely”. But it should be emphasized that was based on “expectation that the economy would continue to grow above trend”.

Also, the meeting took place before release of Q3 GDP, which showed merely 2.8%. That’s clearly lower than RBA’s own projection of 2.0%. And 2.8% could merely be described as being around trend, not above trend. Thus there is prospect of a dovish shift in RBA’s upcoming forecast in February Monetary Policy Statement.

Japan cabinet office lowered growth and inflation forecast, but consumption offers a bright spot

Japan Cabinet Office lowered fiscal 2018 and 2019 growth forecast notably in the new economic projections. The move was due to impact from natural disaster as well as increasing downside risks from US-China trade war. Inflation forecasts was also revised lower. Though, private consumption is expected to pick up down the road, providing a bright spot.

For fiscal 2018, which ends in March, growth is now expected to grow 0.9%, sharply lower from prior projection of 1.5%. For fiscal 2019, growth is projected to be at 1.3%, also down from prior projection of 1.5%.

On inflation, core CPI is projected to rise 1.0% in fiscal 2018, revised down from prior forecast of 1.1%. For fiscal 2019, core CPI is expected to climb slightly to 1.1%, also revised down from prior estimate of 1.5%.

In other projections, capital expenditure is forecast to rise 3.6% in fiscal 2018, then slow to 2.7% in fiscal 2019. Private consumption is expected to rise 0.7% in fiscal 2018 and accelerate to 1.2% in fiscal 2019.

China Xi pledged reform and open up markets, with no specifics

At the 40th anniversary of market liberalization, Chinese President Xi Jinping used one and a half hour to delivered some high level promises but failed to deliver any specifics. He said “we must, unswervingly, reinforce the development of the state economy while, unswervingly, encouraging, supporting and guiding the development of the non-state economy”.

He added that “Every step of reform and opening up is not easy. In the future, we will be inevitably faced with all sorts of risks and challenges, and even unimaginable tempestuous storms.” But he also emphasized that “opening brings progress while closure leads to backwardness.”

China growth to slow to 6-6.5% next year, with help from loose policy

Du Feilun, director of the Institute of Economic Research at the National Development and Reform Commission (NDRC), said the China’s growth would slow to 6.0-6.5% next year, with the help from moderately loose economic policy.

He said there is “immense” short-term pressure on the economy, from domestic challenges and trade war with the US”. However, “there is not too much upward pressure on prices, thus it provides a good environment for economic operations and a good space for monetary policy adjustments.”

He expected China’s aggregate economic policy to be “moderately loose next year to maintain steady growth”. But he didn’t expect China to return to the “old path” of massive stimulus.

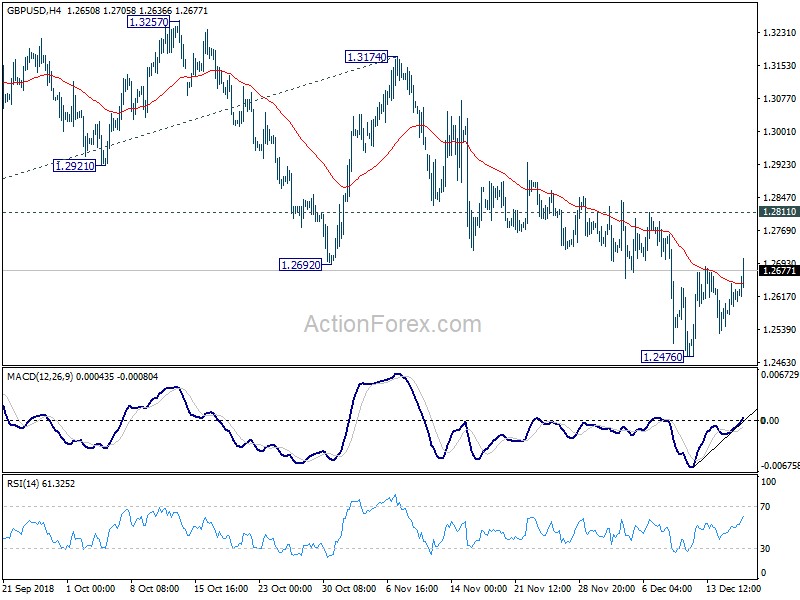

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2574; (P) 1.2611; (R1) 1.2650; More…

GBP/USD rebounds to as high as 1.2705 today but after all, it’s in consolidation from 1.2476. Intraday bias remains neutral for the moment. And even in case of further rise, upside should be limited by 1.2811 resistance to bring fall resumption. On the downside, break of 1.2476 will extend larger down trend from 1.4376 to 61.8% projection of 1.4376 to 1.2661 from 1.3174 at 1.2114. However, firm break of 1.2811 will be an early signal of trend reversal and turn focus back to 1.3174 resistance.

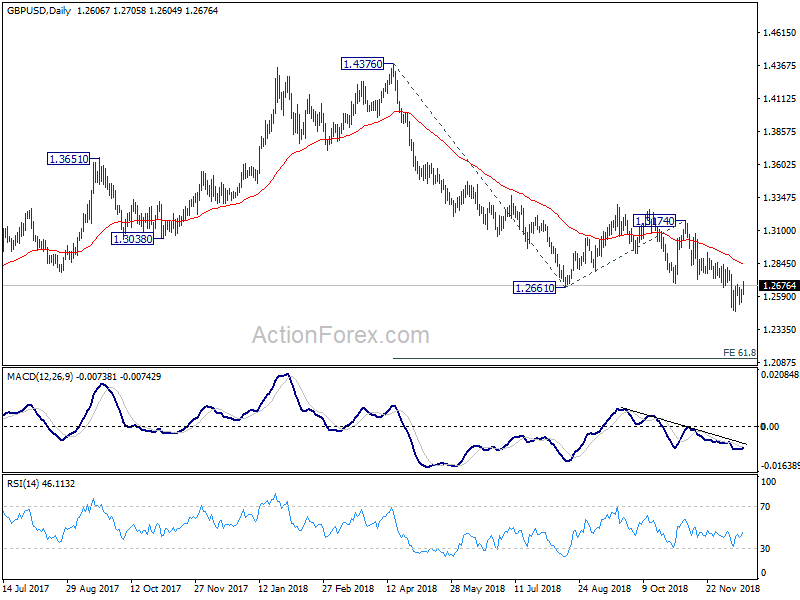

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA. The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend from 2.1161 (2007 high). And this will now remain the preferred case as long as 1.3174 structural resistance holds. GBP/USD should now target a test on 1.1946 first. Decisive break there will confirm our bearish view.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Dec | -24.1 | -37.1 | ||

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 09:00 | EUR | German IFO Business Climate Dec | 101 | 101.7 | 102 | |

| 09:00 | EUR | German IFO Current Assessment Dec | 104.7 | 104.9 | 105.4 | 105.5 |

| 09:00 | EUR | German IFO Expectations Dec | 97.3 | 98.2 | 98.7 | |

| 13:30 | CAD | Manufacturing Sales M/M Oct | -0.10% | 0.30% | 0.20% | |

| 13:30 | USD | Housing Starts Nov | 1.26M | 1.23M | 1.23M | 1.22M |

| 13:30 | USD | Building Permits Nov | 1.33M | 1.27M | 1.26M | 1.27M |

{kind=link}