Dollar received no support from better than expected ADP employment data. Instead, it’s weighed down by dovish comments from a Fed official. The greenback is trading as the second weakest for today in early US session. It’s just slightly better than Sterling, which continues to be pressured by Brexit uncertainties. Yen pared back much of the “flash crash” gains but remains the strongest one for today, thanks to risk aversion. It’s now followed by Canadian Dollar as the second strongest, as WTI crude oil is back at 47.5, trying to extend recent rebound.

European stocks are weighed down by Apple’s revenue downgrade and worries over China’s slow down. At the time of writing, DAX is down -0.89% while CAC is down -0.81%. But FTSE reversed earlier loss and is up 0.12%. German 10 year yield is up 0.0092 at 0.177, much better than yesterday’s low of 0.150. Earlier in Asia, Hong Kong HSI closed down -0.26%, China Shanghai SSE dropped -0.04%, Singapore Strait Times dropped -0.86%. Focus will now turn to US markets.

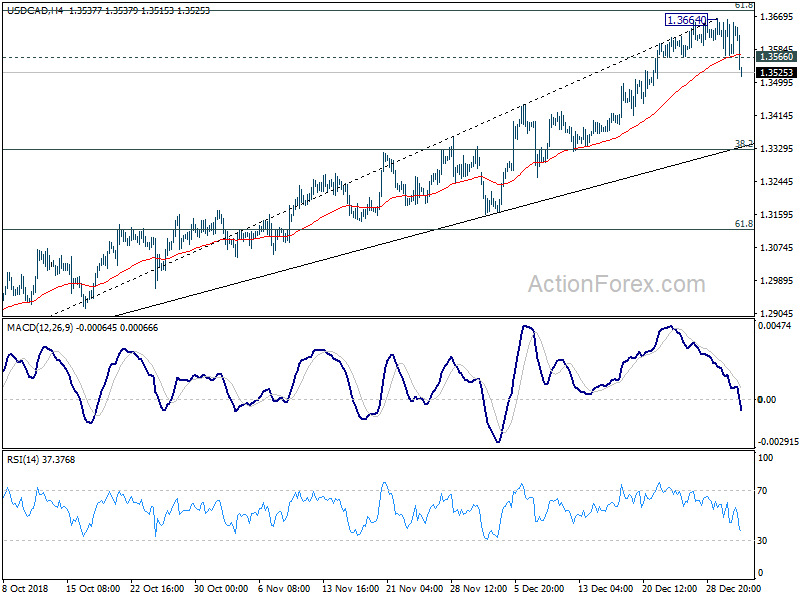

Technically, Yen and Aussie pairs are in consolidation after earlier spike move. Such consolidation should extend for a while. EUR/USD is staying in range of 1.2700/1496. USD/CHF is in range of 0.9789/9963. EURGBP back in range of 0.8927/9086 despite a brief rally attempt. Breakouts are still being awaited. USD/CAD’s sharp fall today and break of 1.3566 now suggests short term topping ahead of 1.3685 fibonacci level. Deeper pull back is now in favor in the near term.

Fed Kaplan: My base case is no action on interest rate in 2019 at all

Dallas Fed President Robert Kaplan said in a Bloomberg interview that he favored pausing the rate hike cycle until the uncertainties are cleared. He pointed to concerns over global growth, weakness in interest-sensitive industries and tighter financial conditions and warned “there’s three big issues that I see reflected in the markets that are consistent with what I’m seeing in the economy and discussions with contacts.”

He added that “I think those three issues — I’m sure — are affecting the markets, but they’re also affecting my thinking about monetary policy. It’s going to take some time so see the depth and breadth of those three issues.”

Thus he said, “my own view is we should not take any further action on interest rates until these issues are resolved, for better, for worse.” And, “I would be an advocate of taking no action and — for example — in the first couple of quarters this year, if you asked me my base case, my base case would be take no action at all.”

US ADP added 271k jobs, low unemployment will get even lower

US ADP report shows 271k growth in private sector jobs in December, up from 157k and beat expectation of 175k. Ahu Yildirmaz, vice president and co-head of the ADP Research Institute, said in the release that “we wrapped up 2018 with another month of significant growth in the labor market.” And, “Although there were increases in most sectors, the busy holiday season greatly impacted both trade and leisure and hospitality. Small businesses also experienced their strongest month of job growth all year.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Businesses continue to add aggressively to their payrolls despite the stock market slump and the trade war. Favorable December weather also helped lift the job market. At the current pace of job growth, low unemployment will get even lower.”

US initial jobless claims rose 10k to 231k

US initial jobless claims rose 10k to 231k in the week ending December 29, above expectation of 215k. Four-week moving average of initial claims dropped -500 to 218.75k. Continuing claims rose 32k to 1.74M in the week ending December 22. Four-week moving average of continuing claims rose 26k to 1.7035M.

UK Brexit Minister Barclay: No deal Brexit likely if MPs reject the deal

UK Brexit Minister Stephen Barclay warned that “no deal will be far more likely if MPs reject the PM’s Brexit deal later this month.” And, he urged fellow MPs to “put the national interest first and vote for this deal so we can get on with delivering Brexit and building the UK’s prosperous future as an outward-looking global trading nation, outside the EU.” And he also emphasized that people “people did not vote for the disruption and uncertainty of no deal.”

Foreign Minister Jeremy Hunt also said “there will be some tough negotiations to follow in the years ahead but I think getting this clearer language on the backstop will help to get it through Parliament.” And, there will be “devastating social consequences” if a second EU referendum was triggered.

UK PMI construction dropped to 52.8, slowdown in housing and commercial activity growth

UK construction PMI dropped to 52.8 in December, down from 53.4 and missed expectation of 52.9 slightly. Markit noted that “business activity expands at weakest pace for three months”, “softest rise in commercial work since May 2018”, but “rebound in business optimism amid hopes of infrastructure boost in 2019”.

Tim Moore, Economics Associate Director at IHS Markit, said in the release that “UK construction firms signalled a slowdown in housing and commercial activity growth during December, which more than offset a strong performance for civil engineering at the end of 2018.” And “Subdued domestic economic conditions and an intense headwind from political uncertainty resulted in the weakest upturn in commercial work for seven months.”

Also relesed in European session, Eurozone M3 rose 3.7% yoy in November. Swiss PMI manufacturing rose 0.1 to 57.8 in December.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3547; (P) 1.3605; (R1) 1.3642; More…

USD/CAD’s break of 1.3566 minor support suggests short term topping at 1.3664, ahead failing 1.3685 fibonacci level. Intraday bias is now back on the downside for pull back to 38.2% retracement of 1.2781 to 1.3664 at 1.3327. We’d expect downside to be contained there to bring rebound. But on the upside, firm break of 1.3664 is now needed to confirm up trend resumption. Otherwise, risk will stay on the upside even in case of recovery.

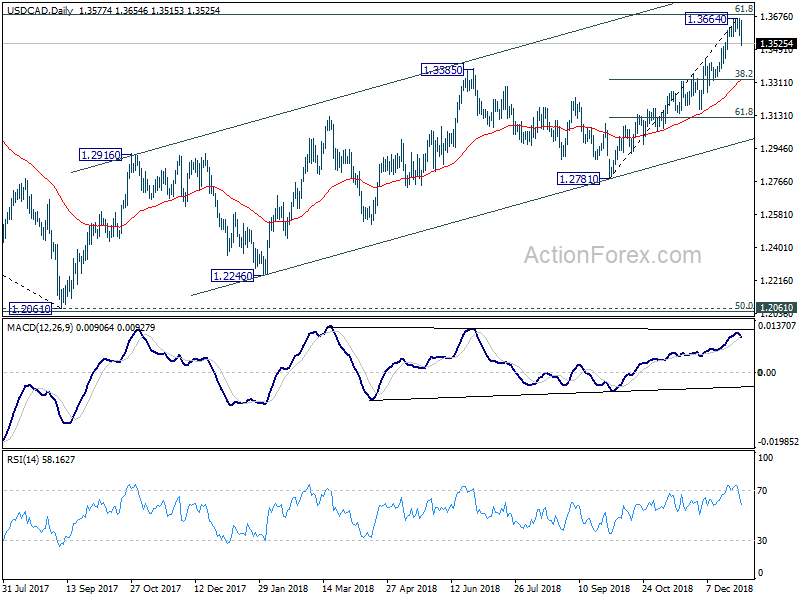

In the bigger picture, up trend from 1.2061 (2017 low) is still in progress and should target 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685. At this point, the structure is not clearly impulsive yet. Hence, we’d be cautious on topping between 1.3685/3793. But in any case, medium term outlook will stay bullish as long as channel support (now at 1.2993) holds. Sustained break of 1.3793 will pave the way to retest 1.4689 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | CHF | PMI Manufacturing Dec | 57.8 | 56.9 | 57.7 | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Nov | 3.70% | 3.80% | 3.90% | |

| 09:30 | GBP | UK Construction PMI Dec | 52.8 | 52.9 | 53.4 | |

| 12:30 | USD | Challenger Job Cuts Y/Y Dec | 35.30% | 51.50% | ||

| 13:15 | USD | ADP Employment Change Dec | 271K | 175k | 179k | 157K |

| 13:30 | USD | Initial Jobless Claims (DEC 29) | 231K | 215K | 216K | 221K |

| 15:00 | USD | Construction Spending M/M Nov | 0.40% | -0.10% | ||

| 15:00 | USD | ISM Manufacturing Dec | 58.4 | 59.3 | ||

| 15:00 | USD | ISM Prices Paid Dec | 58 | 60.7 | ||

| 15:00 | USD | ISM Employment Dec | 58.4 |

{kind=link}