Dollar suffers steep selloff in early US session after shockingly poor retail sales data. The release of December’s sales was delayed due to government shutdown. And we’ve finally got some clues on how bad the US economy performed on double whammy on shutdown and trade war. Nevertheless, for now, Canadian Dollar is even worse as pressured by poor manufacturing sales. Sterling follows as second weakest as Brexit debate resumes in the Commons. Dollar is just the third weakest.

New Zealand Dollar remains the strongest one for today, feeling the residual support from RBNZ. Euro overtakes Australian Dollar as the second strongest. Germany GDP stagnated in Q4 but after all, it did avoid a technical recession, same as Japan. Yen is trying to fight back as stocks are possibly reversing. We pointed out earlier that stocks and bonds had no positive reaction to the so-called positive news regarding US-China trade talks. Both China and Hong Kong stocks closed lower. Japan JGB yield ended with a decline. German 10-year yield is also currently down. Is a 60-days extension in trade truce something good for the economy? Remember that the current tariffs will likely be in place in case of extension. Such an act is only prolonging the damages.

Technically, EUR/USD and USD/CHF looks set to turn into consolidation after Dollar’s pull back. GBP/USD is still in near term decline. AUD/USD is staying in near term consolidation. USD/CAD looks set to resume rebound from 1.3068 and focus is immediately on 1.3329 resistance. EUR/GBP is eyeing 0.8821 resistance and break will resume rebound from 0.8617. The most interesting development is in USD/JPY. Deep decline now argues that prior stronger than expected rise was just false dawn. We’ll see.

In other markets, FTSE is currently up 0.30%. DAX is down -0.11%. CAC is up 0.39%. German 10-year yield is down -0.035 at 0.092, below 0.1 handle. Earlier in Asia, Nikkei dropped -0.02%. Hong Kong HSI dropped -0.23%. China Shanghai SSE dropped -0.05%. Singapore Strait Times rose 0.26%. Japan 10-year JGB yield dropped -0.0039 to -0.01, staying negative.

US retail sales suffered largest drop in nine-years, jobless claims rose

Dollar is sold off sharply in early US session after way worse than expected December retail sales data. Headline sales dropped -1.2% versus expectation of 0.1% mom rise. That’s also the largest decline in nine years since September 2009. Ex-auto sales dropped -1.8% versus expectation of 0.0% mom.

Initial jobless claims rose 4k to 239k in the week ending February 9, above expectation of 225k. Four-week moving average of initial claims rose 6.75k to 231.75k, highest since January 27, 2018. Continuing claims rose 37k to 1.773M in the week ending February 2. Four-week moving average of continuing claims rose 9k to 1.750M.

Also from the US, headline PPI slowed to 2.0% yoy in January, down from 2.5% yoy and missed expectation of 2.1% yoy. PPI core slowed to 2.6% Yoy, down from 2.7% yoy but beat expectation of 2.5% yoy.

From Canada, manufacturing sales dropped -1.3% mom in December versus expectation of 0.7% mom. New housing price index was flat mom in December.

BoE Vlieghe: Monetary easing more likely than tightening in case of no-deal Brexit

BoE MPC member Gertjan Vlieghe said in a speech that the net balance of economic news for the UK has been to the “downside”. Thus, the appropriate pace of monetary tightening is “somewhat slower” than he judged a year ago.

A quarter point hike per year is a “reasonable central case” if global growth does not slow materially further, path to Brexit is in line with government’s state objective, and pay growth continues at current pace. Though, if a no-deal Brexit is avoided, he expects Sterling to appreciate. And the exact degree of future monetary tightening will depend on appreciation of the Pound.

However, a no-deal outcome is “likely to lead to some economic disruption, which could possibly be severe”. There are some paths that are possible, but “not all are equally likely”. In his view, “an easing or an extended pause in monetary policy is more likely to be the appropriate policy response than a tightening.” But he emphasized that BoE will have to “judge in real time” how well inflation expectations remain anchored, and how households and businesses are reacting to the disruptions.

Eurozone GDP grew 0.2% qoq in Q4, matched expectations

Eurozone GDP grew 0.2% qoq in Q4, unchanged from Q3 and matched expectations. Annually, GDP grew 1.2% yoy. Over the whole year 2018, GDP grew 1.8%. Employment grew 0.3% qoq, above expectation of 0.2% qoq. EU 28 GDP grew 0.3% qoq, 1.4% yoy. Over 2018, EU 28 GDP grew 1.9%.

German economy stagnated in Q4, but narrowly escaped recession

Germany GDP stagnated in Q4 and grew 0.0% qoq. But that was enough to narrow escape a technical recession following -0.2% contraction in Q3. Over the year, GDP grew 0.9% yoy in Q4. For the whole year of 2018, GDP grew 1.5% calendar adjusted.

Looking at the details, positive contributions mainly came from domestic demand. Development of foreign trade did not make a positive contribution to growth in the fourth quarter. According to provisional calculations, exports and imports of goods and services increased nearly at the same rate in the quarter-on-quarter comparison.

German Economy Ministry said in its monthly bullet that Brexit and trade dispute are still causing uncertainty. Also, indicators point to subdued development of exports in the coming months. Nevertheless, construction boom is likely to continue given increase in orders and private consumption is likely to continue doing well.

Japan GDP rebounded with weak momentum, but avoided recession

Japan GDP grew 0.3% qoq in Q3, rebounding from Q3’s -0.6% qoq contraction. The good news is that Japan avoided a technical recession of two consecutive quarters of contraction. But growth was disappointing and missed expectation of 0.4% qoq. GDP deflator dropped -0.3% yoy, slightly better than expectation of -0.4% yoy.

Japanese Economy Minister Toshimitsu Motegi said in a statement that “the economy is in gradual recovery as growth is led by private demand”. However, “China-bound exports of information-related materials have weakened as the Chinese economy slowed”. He added that the government needs to “monitor uncertainty over global economic outlook including Chinese economy as well as fluctuations in financial markets.”

China trade balance: Import from US plunged -41%, from EU rose…

January trade data from China showed a better picture. Exports grew 9.1% yoy versus expectation of -3.3% yoy. Import dropped only -1.5% yoy versus expectation of -10.2% yoy. Trade surplus narrowed to USD 39.2B, above expectation of USD 32.0B. However, it should be noted that the trade data for the first two months of the year are generally distorted by Lunar New Year holidays. Thus, while the data are positive, it’s premature to declare that the slow down in China has bottomed. Nevertheless, it’s worth noting that exports to the US since tariff war began were not so much affected. But import from the US plunged, quite notably in Jan by -41%.

In USD terms, total trade rose 4.0% yoy to USD 396B. Import dropped -1.5% yoy to USD 178.4B. Exports rose 9.1% yoy to USD 217.6B. Trade surplus rose to USD 39.2B.

With EU, total trade rose 12.4% yoy to USD 64.5B. Import rose 8.2% yoy to 25.9B. Export rose 15.3% yoy to USD 38.6B. Trade surplus was at USD 12.7B.

With US, total trade dropped -13.9% yoy to USD 45.8B. Import dropped -41% yoy to USD 9.2B. Exports dropped -2.4% yoy to USD 36.5B. Trade surplus was at USD 27.3B.

With AU, total trade rose 10.8% yoy to USD 14.4B. Import rose 7.6% yoy USD 10.1B. Export rose 19.1% yoy to USD 4.3B. Trade deficit was at USD 5.8B.

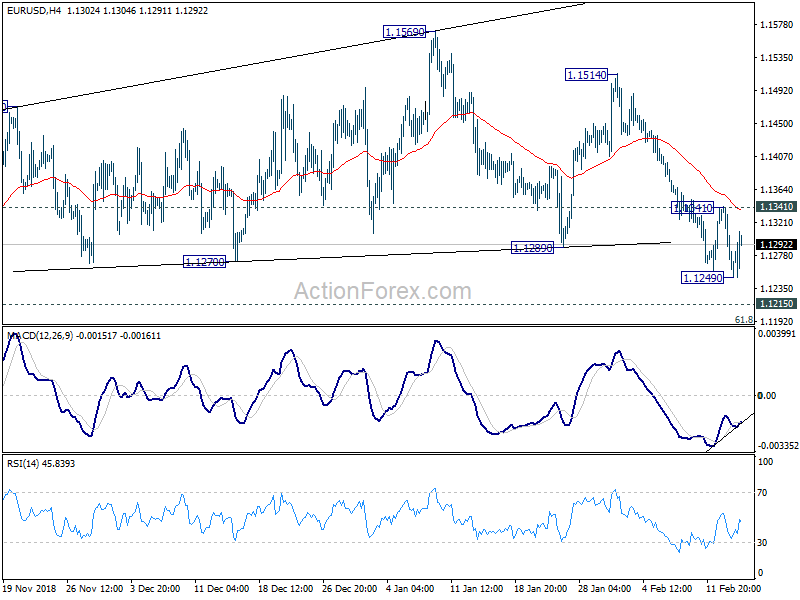

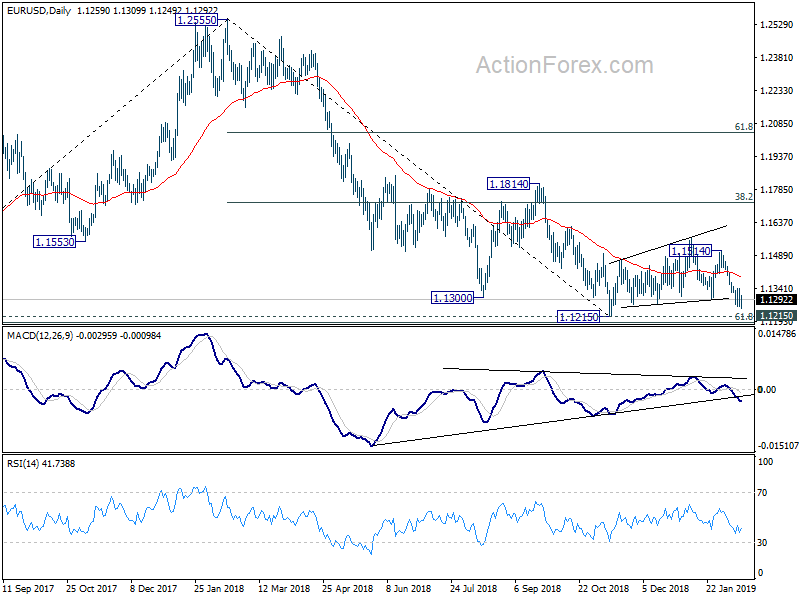

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1233; (P) 1.1288; (R1) 1.1315; More…..

EUR/USD dipped to 1.1249 earlier today but quickly recovered, with 4 hour MACD crossed above signal line again. Intraday bias turned neutral first. Further decline is still expected with 1.1341 minor resistance intact. We’d holding on to the view that consolidation from 1.1215 has completed. Below 1.1249 will target 1.1215 first. Break will resume larger down trend from 1.2555 to 1.1186 fibonacci level. However, considering bullish convergence condition in 4 hour MACD, break of 1.1341 resistance will dampen out view and suggest short term bottoming. Intraday bias will be turned back to the upside to extend the consolidation from 1.1215 with another rising leg.

In the bigger picture, as long as 1.1814 resistance holds, down trend down trend from 1.2555 medium term top is still in progress and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. However, break of 1.1814 will confirm completion of such down trend and turn medium term outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q4 P | 0.30% | 0.40% | -0.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 P | -0.30% | -0.40% | -0.30% | |

| 00:00 | AUD | Consumer Inflation Expectation Feb | 3.70% | 3.50% | ||

| 00:01 | GBP | RICS House Price Balance Jan | -22.00% | -20.00% | -19.00% | |

| 02:00 | CNY | Trade Balance (USD) Jan | 39.2B | 32.0B | 57.1B | |

| 02:00 | CNY | Trade Balance (CNY) Jan | 271B | 235B | 395B | |

| 07:00 | EUR | German GDP Q/Q Q4 P | 0.00% | 0.10% | -0.20% | |

| 07:30 | CHF | Producer & Import Prices M/M Jan | -0.70% | -0.40% | -0.60% | |

| 07:30 | CHF | Producer & Import Prices Y/Y Jan | -0.50% | -0.20% | 0.60% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.20% | 0.20% | 0.20% | |

| 10:00 | EUR | Eurozone Employment Q/Q Q4 P | 0.30% | 0.20% | 0.20% | |

| 13:30 | CAD | Manufacturing Sales M/M Dec | -1.30% | 0.70% | -1.40% | -1.70% |

| 13:30 | CAD | New Housing Price Index M/M Dec | 0.00% | 0.00% | 0.00% | |

| 13:30 | USD | Initial Jobless Claims (FEB 09) | 239K | 225K | 234K | 235K |

| 13:30 | USD | PPI M/M Jan | -0.10% | 0.10% | -0.20% | -0.10% |

| 13:30 | USD | PPI Y/Y Jan | 2.00% | 2.10% | 2.50% | |

| 13:30 | USD | PPI Core M/M Jan | 0.30% | 0.20% | -0.10% | 0.00% |

| 13:30 | USD | PPI Core Y/Y Jan | 2.60% | 2.50% | 2.70% | |

| 13:30 | USD | Retail Sales Advance M/M Dec | -1.20% | 0.10% | 0.20% | 0.10% |

| 13:30 | USD | Retail Sales Ex Auto M/M Dec | -1.80% | 0.00% | 0.20% | 0.00% |

| 15:00 | USD | Business Inventories Nov | 0.20% | 0.60% | ||

| 15:30 | USD | Natural Gas Storage | -237B |

{kind=link}