After taking a brief Brexit, Sterling’s rally extends again today on optimism that risk of no deal Brexit is fading. Also, key figure of Brexiteer also expressed condition support for UK Prime Minister Theresa May’s Brexit deal. For now, with some key resistance levels already taken out, the Pound is rather unstoppable. Meanwhile Swiss Franc follows as the second strongest on escalation in tensions between Pakistan and India. The Franc is usually more sensitive to geo-tensions than Yen.

On other hand, Australian and New Zealand Dollar are the weakest ones for today so far. Yen is following s the third weakest. Dollar is mixed as markets are watching Trump-Kim summit in Vietnam, Trump gave warm greeting to his friend Kim and hailed “our relationship is a very special relationship”. Kim also said “we’ll have a very interesting dialogue”. as Testimony of USTR Robert Lighthizer will also be closely watched as he might reveal some of the little known substantial progress in trade talks with China. Fed Chair Jerome Powell will also have his second day of Congressional testimony.

Technically, USD/CHF’s break of 0.9981 support is a sign of rejection by 1.0128 resistance and further decline is now mildly in favor back to 0.9716 support. USD/CAD is looking at 1.3112 temporary low and break will target 1.3068 key support. GBP/JPY’s strong break of medium term trend line add to the case of underlying strength in the Pound. Next is 150 handle.

In Europe, currently, FTSE is down -0.79%. DAX is down -0.37%. CAC is down -0.08%. German 10-year yield is up -0.0092 at 0.129. Earlier in Asia, Nikkei closed up 0.50%. Hong Kong HSI dropped -0.05%. China Shanghai SSE rose 0.42%. Singapore Strait Times dropped -0.36%. Japan 10-year JGB yield rose 0.0019 to -0.024.

Swiss Franc jumps on Pakistan/India tension

Tensions at the border of Pakistan and India escalate today as both side they’ve shot down the other’s fighter jets. The tension started after a suicidal car bombing by Pakistan-based militants in Kashmir that killed at least 40 paramilitary policy on February 14. It escalated quickly on Tuesday after India launched air strike on a militant training base. Pakistan’s fighter planes have shot down two Indian jets as their entered the country’s airspace today. Swiss Franc surges broadly in response to the development.

Canada CPI slowed to 1.4%, CAD rise as CPI risks cleared

Canada headline CPI slowed to 1.4% yoy in January, down from 2.0% yoy, matched expectations. CPI core-common was unchanged at 1.9% yoy. CPI core-median was unchanged at 1.8% yoy. CPI core-trim was unchanged at 1.9% yoy. Energy costs declined 6.9%, while the growth in the price of services slowed to 2.7% as transitory pressures from the air transportation, telephone services and travel tours indexes dissipated. USD/CAD drops again as the CPI risk is now cleared. Rebound in oil price is helping the Loonie. WTI crude is now back above 56.7, comparing to this week’s low at 55.11.

Bundesbank Wedimann, growth to fall well short of 1.5% potential this year

Bundesbank President Jens Weidmann said today that German economy growth will “fall well short of the potential rate of 1.5 percent in 2019”. That’s because “there is much to suggest that the dip in growth here in Germany has persisted into the current year”. However, he emphasized that the prerequisites for growth remain intact, including low financing cost, expansion in employment market and rising wages. Thus, there is no reason for pessimism yet.

On ECB policies, he said that the central bank should looks through short term fluctuations in inflation caused by oil prices to temporary slowdown. He emphasized that ECB’s “price stability target is medium term, so we should look through these fluctuations”. Also, “it is clear that short-term fluctuations in oil prices — like the sharp decline at the end of 2018 — but also corrections in growth expectations for 2019, could temporarily influence the inflation outlook.”

Separately, it’s reported that German cabinet gave green-light for a second eight-year term for Weidmann, as the current term expires at the end of April.

Eurozone economic sentiment dropped to -0.2, business climate unchanged at 0.69

Eurozone Economic Sentiment Indicator dropped -0.2 to 106.1 in February, slightly above expectation of 106.0. The broadly unchanged reading resulted from “weaker industry and construction confidence in combination with more upbeat signals from the services sector, as well as, to a lesser extent, retail trade and consumers”. Meanwhile the ESI dropped in Franc (-0.9%) and Italy (-1.6), practically flat in Germany (-0.1) and Spain (0.0), but improved in the Netherlands (+3.0).

Business Climate Indicator is flat at 0.69 in February, slightly above expectation of 0.67. Eurostats noted “Managers’ production expectations, as well as their assessments of the stocks of finished products, overall- and export order books clouded over. Meanwhile, the appraisals of past production rebounded from last month’s sharp drop.”

Also from Eurozone, industrial confidence dropped to -4. Services confidence rose to 12.1. Consumer confidence was finalized at -7.4. M3 money supply rose 3.8% yoy in January.

Rees-Mogg could back May’s Brexit deal with reasonably effective time limit on Irish backstop

Jacob Rees-Mogg, a high profile Brexiteer Conservative, said that the could back Prime Minister Theresa May’s Brexit deal if there is a reasonably effective time limit on the Irish backstop.

Rees-Mogg told BBC ratio that “I can live with the de facto removal of the backstop…. I mean that if there is a clear date that says the backstop ends, and that is in the text of the treaty or equivalent of the text of the treaty”.

But he also insisted that the time limit should be “a short date, not a long date, then that would remove the backstop in the lifetime of parliament and that would have a reasonable effect from my point of view.”

BoJ Kataoka: Uncertainty heightened if current monetary easing is prolonged

BoJ board member Goushi Kataoka continued his call for more monetary stimulus in a speech to business leaders today. He argued that the central bank should ramp up its monetary easing to achieve inflation target earlier.

And he warned, “if the current monetary easing is prolonged, it would mean the period in which Japan’s economy faces various uncertainties will be longer. That means uncertainty on achieving our price target will heighten.”

Kataoka is a known dove who persistently vote against BoJ’s policy in push for more easing.

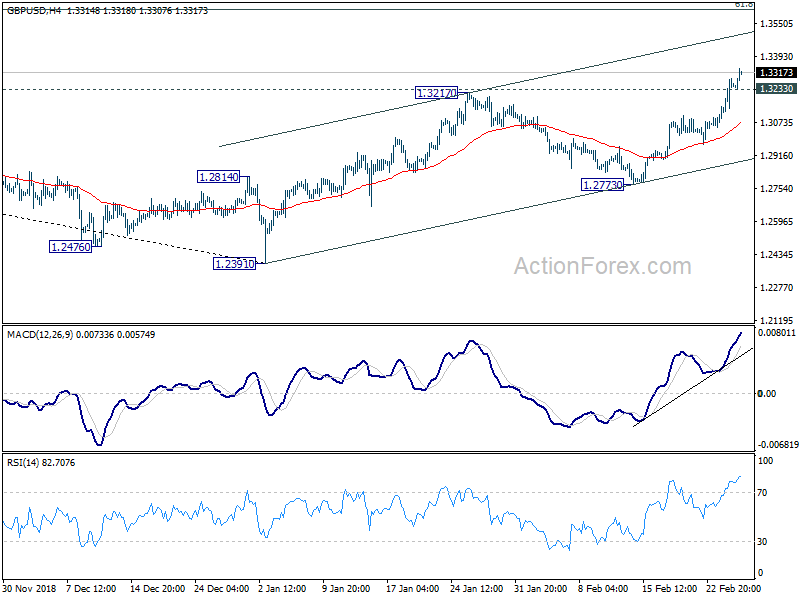

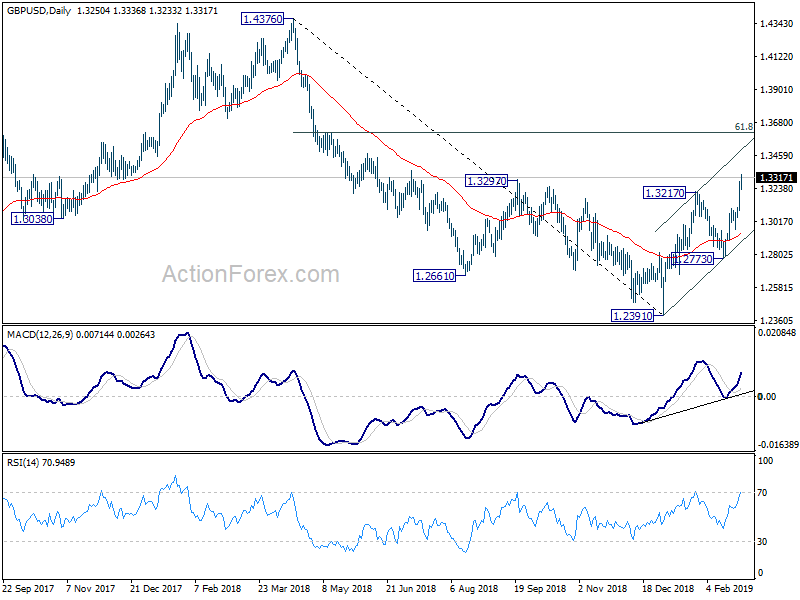

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3135; (P) 1.3212; (R1) 1.3328; More….

GBP/USD’s rally accelerates to as high as 1.3336 so far today and intraday bias remains on the upside. As noted before, whole decline from 1.4376 should have completed at 1.2391. Further rise should be seen to 61.8% retracement of 1.4376 to 1.2391 at 1.3618 next. Sustained break will pave the way to 1.4376. On the downside, below 1.3233 will turn bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, medium term decline from 1.4376 (2018 high) should have completed at 1.2391. Rise from 1.2391 is now seen as the third leg of the corrective pattern from 1.1946 (2016 low). Further rise could be seen through 1.4376 in medium term. On the downside, though, break of 1.2773 support will turn focus back to 1.2391 low and then 1.1946.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Jan | -914M | -300M | 264M | 12M |

| 00:01 | GBP | BRC Shop Price Index Y/Y Feb | 0.70% | 0.30% | 0.40% | |

| 00:30 | AUD | Construction Work Done Q4 | -3.10% | 0.50% | -2.80% | -3.60% |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 3.80% | 4.00% | 4.10% | |

| 10:00 | EUR | Eurozone Business Climate Feb | 0.69 | 0.67 | 0.69 | |

| 10:00 | EUR | Eurozone Economic Confidence Feb | 106.1 | 106 | 106.2 | 106.3 |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -0.4 | 0.1 | 0.5 | 0.6 |

| 10:00 | EUR | Eurozone Services Confidence Feb | 12.1 | 11 | 11 | |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -7.4 | -7.4 | -7.4 | |

| 13:30 | CAD | CPI M/M Jan | 0.10% | 0.10% | -0.10% | |

| 13:30 | CAD | CPI Y/Y Jan | 1.40% | 1.40% | 2.00% | |

| 13:30 | CAD | CPI Core-Common Y/Y Jan | 1.90% | 1.90% | 1.90% | |

| 13:30 | CAD | CPI Core-Median Y/Y Jan | 1.80% | 1.80% | 1.80% | |

| 13:30 | CAD | CPI Core-Trim Y/Y Jan | 1.90% | 1.90% | 1.90% | |

| 13:30 | USD | Advance Goods Trade Balance (USD) Dec | -79.5B | -75.3B | -71.6B | |

| 13:30 | USD | Wholesale Inventories M/M Dec F | 1.10% | 0.40% | 0.30% | |

| 15:00 | USD | Fed Powell testifies Before House Panel | ||||

| 15:00 | USD | Pending Home Sales M/M Jan | 0.80% | -2.20% | ||

| 15:00 | USD | Factory Orders Dec | 0.80% | -0.60% | ||

| 15:30 | USD | Crude Oil Inventories | 3.7M |

{kind=link}