Markets sentiments stabilized as more information was revealed regarding escalation of US-China trade tensions. The Chinese delegation will still travel to the US, with Vice Premier Liu He remaining as the lead negotiator. While there are still a lot of uncertainties with tariffs threats on, there is a least some hope for another about turn before new tariffs are imposed this Friday.

Meanwhile, RBA refrained from cutting interest rates pre-emptively. Australian Dollar is double supported and rebounds strongly today. Sterling is currently the second strongest one after Aussie, followed by Canadian. Dollar is now the weakest one for today, followed by Swiss Franc and then New Zealand Dollar. However, it should be note that the greenback is staying above last week’s close against all except Euro, Yen and Aussie. Yen remains the strongest one for the week. That is, risk aversion is not totally eased.

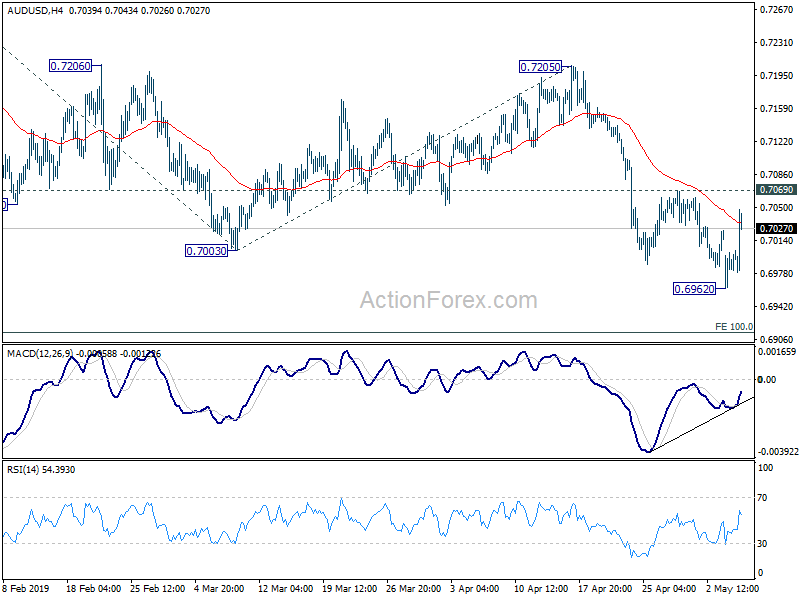

Technically, EUR/USD and USD/CHF remains bounded in tight range, maintains near term bearish outlook. USD/JPY is staying near term bearish. EUR/JPY continues to defend 123.39 key support but looks vulnerable. AUD/USD, despite today’s rebound, is held below 0.7069 resistance and stays near term bearish. Though, EUR/AUD’s break of 1.5920 minor support is an early sign of near term reversal.

Overnight, DOW closed down just -0.25% at 26438.48 after diving to as low as 26033.95, paring most of initial losses. S&P 500 dropped -0.50%. NASDAQ dropped -0.45%. 10-year yield dropped -0.031 to 2.500. In Asia, Hong Kong HSI is up 0.46%. China Shanghai SSE is up 0.69%. Singapore Strait Times is up 0.71%. Japan is still enjoying the 10-day holiday.

China VP Liu to visit US on May 9-10 despite new tariff threats

The Chinese Ministry of Commerce confirmed that Vice Premier Liu He will travel to the US on May 9-10 to resume trade negotiations despite re-escalated tariff threats. That’s a slight delay comparing to the original plan of traveling to the US on Wednesday. According to the MOFCOM’s statement, the visit was by invitation of US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin.

Lighthizer and Mnuchin noted erosion of commitment by China in trade talks

More information is now revealed on why US-China trade tensions suddenly heightened. US Trade Representative Robert Lighthizer complained China reneges on its commitment during that trade negotiations as “we felt we were on track to get somewhere”. For now, significant issues remain unresolved in trade negotiations. He specifically criticized that “over the course of last week we have seen an erosion of commitments by China” And, “that in our view is unacceptable.”

Treasury Secretary Steven Mnuchin also noted that in the new draft of the agreement sent over from China during the weekend, China pulled back on language in the text on a number of issues. Such changes had the “potential to change the deal very dramatically”. With the changes, China wanted to reopen areas that had already be negotiated. Mnuchin said “we are not willing to go back on documents that have been negotiated in the past”.

The drastic change in China’s commitment infuriated Trump, who announced to push US-China trade war to full blown level with a tweet on Sunday. He planned to raise tariffs on USD 200B of Chinese goods to 25% from 10%. Also, there will be 25% tariffs on currently “untaxed” USD 325B of Chinese goods shortly.

RBA stands pat at 1.50%, revised down growth and inflation forecasts

Australian Dollar rebounds after RBA left cash rate unchanged at 1.50%, rather than delivered a rate cut as some expected. While, keeping interest rate on hold, the central bank did lay down the criteria in labor market development as condition for policy action in response to subdued inflation.

RBA acknowledged that Q1 inflation data were “noticeably lower than expected”. And, “further improvement in the labour market was likely to be needed for inflation to be consistent with the target”. Thus, the central bank said it will be “paying close attention to developments in the labour market at its upcoming meetings.

With the new economic projections, RBA is expecting around 2.75% growth in 2019 and 2020. That’s a slightly downward revision from February’s around 3% in 2019 and by a little less in 2020.

Underlying inflation is expected to be at 1.75% this year and 2% in 2020. Headline inflation is expected to be at around 2% in 2019. There were also slight downward revision from February’s projection of 2% in 2019 and 2.25% in 2020.

Australia retail sales rose 0.3%, trade surplus narrowed to AUD 4.95B

Australia retail sales rose 0.3% mom in March, above expectation of 0.2% mom. February’s growth was revised up from 0.8% mom to 0.9% mom. In seasonally adjusted terms, there were rises in Victoria (0.7%), Queensland (0.6%), New South Wales (0.2%), Tasmania (0.4%), South Australia (0.1%), and the Northern Territory (0.7%). The Australian Capital Territory was relatively unchanged (0.0%) and Western Australia (-0.7%) fell in seasonally adjusted terms in March 2019.

Trade surplus narrowed to AUD 4.95B in March, down from AUD 5.14B but beat expectation of AUD 4.49B. Goods and services exports dropped -2% to AUD 39.34B. Good and services imports dropped -1% to AUD 34.39B.

Japan PMI manufacturing finalized at 50.2, recent drop in momentum potentially subsided for now

Japan PMI manufacturing was finalized at three-month high at 50.2 in April, back above 50 too. Markit noted that new orders and output continued to fall, but to lesser extends. Meanwhile, employment growth picked up and business confidence improved.

Joe Hayes, Economist at IHS Markit said: “A pick-up in the Japan Manufacturing PMI to a three-month high will be a welcome sign that the recent drop in momentum has potentially subsided for now. New orders and output both declined in April, but to lesser extents, while business confidence continued to climb from its near-record low in February. Given the difficulties faced by firms in semi-conductor and automobile-related industries in recent months, it bodes well that anecdotal evidence indicated that stronger optimism was in part driven by more upbeat forecasts for these two key Asian industries.”

Fed Harker and Kaplan see low inflation as transitory

Philadelphia Fed President Patrick Harker said yesterday that he saw current fall in inflation as “transitory. And he continued to see “one increase at most this year, possibly one, at most”, regarding interest rates.

But he also emphasized that “If any component of the outlook were to affect my view on the appropriate path of monetary policy, it would be inflation.” For now, “we’re not there yet”. Harker said “it would take more data to convince me” to change the policy path.

On trade, Harker also warned that tariff is “not a healthy thing for the economy overall”. And trade tensions are part of an “umbrella of uncertainty” that is weighing on businesses and markets.

Separably, Dallas Fed President Robert Kaplan said current dip in inflation should be just transitory. And, he’s not inclined to cut interest rate to deal with current sluggish inflation. Though, to him, there is no bias to move interest rate in either direction.

Kaplan also noted that trade uncertainty is impacting on firms’ supply chains. And it has chilling effect on US industries. Though, trade uncertainty is not yet having material impact on US GDP. He’s also concerned with deceleration in global economy.

Elsewhere

Germany factory orders rose 0.6% mom in March, lower than expectation of 1.5% mom. Swiss foreign currency reserves rose to CHF 772B in April versus expectation of CHF 756B. Canada will release Ivey PMI later in the day.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6972; (P) 0.6987; (R1) 0.7013; More…

Intraday bias in AUD/USD is turned neural with today’s strong rebound. Though, as long as 0.7069 resistance holds, near term outlook stays cautiously bearish and deeper decline is expected. On the downside, break of 0.6962 will resume the fall from 0.7295 to 100% projection of 0.7295 to 0.7003 from 0.7205 at 0.6913. Decisive break there will indicate further downside acceleration and pave the way to retest 0.6722 low. However, considering bullish convergence condition in 4 hour MACD, firm break of 0.7069 will indicate near term bottoming and turn bias back to the upside for 0.7205 resistance and above.

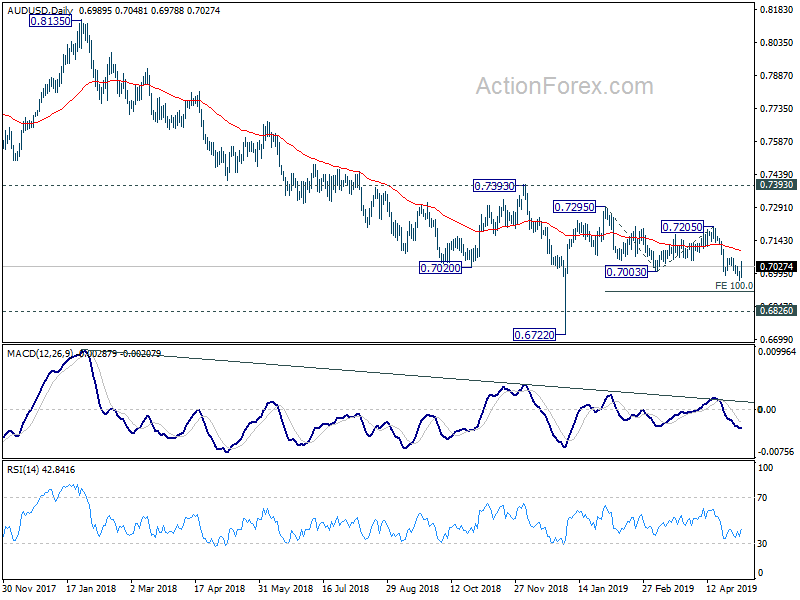

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | PMI Manufacturing Apr F | 50.2 | 49.5 | 49.5 | |

| 1:30 | AUD | Trade Balance (AUD) Mar | 4.95B | 4.49B | 4.80B | 5.14B |

| 1:30 | AUD | Retail Sales M/M Mar | 0.30% | 0.20% | 0.80% | 0.90% |

| 3:00 | NZD | RBNZ 2-Year Inflation Expectation Q2 | 2.00% | 2.00% | ||

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.25% | 1.50% | |

| 6:00 | EUR | German Factory Orders M/M Mar | 0.60% | 1.50% | -4.20% | -4.00% |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Apr | 772B | 756B | 756B | |

| 9:00 | EUR | EU Economic Forecasts | ||||

| 14:00 | CAD | Ivey PMI Apr | 51.5 | 54.3 |

{kind=link}