Yen remains the strongest one for today, extending this week’s rally on risk aversion. Following steep decline in the US, Asian markets open broadly lower and stay pressured. Threat of full-blown trade war continues to weigh on investors’ sentiments. New round of tariffs on Chinese imports is ready to be imposed during Chinese Vice Premier Liu He’s visit to Washington on May 9-10. It’s unsure how Liu could turn around the situation after China reneged on its own commitments in the negotiations.

In the currency markets, Australian Dollar is currently the second strongest for today, benefiting somewhat from the rally in AUD/NZD. Euro is the third strongest. Meanwhile, New Zealand Dollar is clearly the weakest one following RBNZ’s dovish rate cut. Dollar is paring some gains, as weighed down by decline in treasury yields. Over the week, though, Yen is the strongest, followed by Euro Dollar. Kiwi is the weakest, followed by Sterling and Canadian.

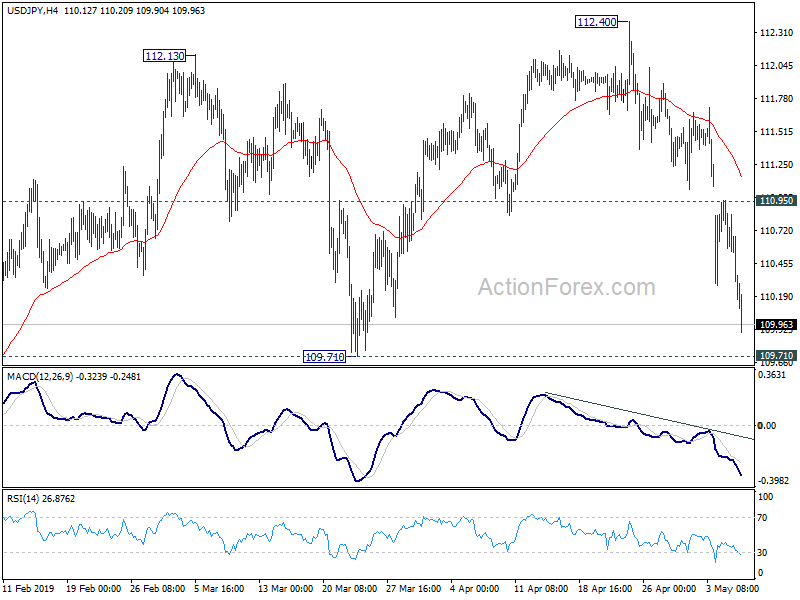

Technically, Yen crosses will remain the main focus for today. USD/JPY is on track to 109.71 support. Decisive break there will confirm near term bearish reversal. EUR/JPY has already taken out 123.39 support to indicate reversal. The question now it’s whether EUR/JPY would accelerate towards 118.62 low. GBP/JPY is now pressing 143.72 key support and looks set to take out it firmly to confirm bearish reversal too. EUR/USD, USD/CHF, USD/CAD and AUD/USD are staying in established range, awaiting breakout.

In Asia, Nikkei is back from holiday, trading down -1.72%. Hong Kong HSI is down -0.70%. China Shanghai SSE is surprisingly resilient and is down only -0.11%, staying above 2900 handle. Singapore Strait Times is down -0.95%. Japan 10-year JGB yield is down -0.0029 at -0.054. Overnight, DOW dropped -1.79%. S&P 500 dropped -1.65%. NASDAQ dropped -1.96%. 10-year yield dropped -0.052 to 2.448. Break of 2.463 support could now pave the way to 2.356 low.

RBNZ cuts OCR to 1.50%, projects below target inflation for longer, sees need for more easing

RBNZ lowers official cash rate by -25bps to 1.50% as widely expected. In the accompanying statement, RBNZ noted that:

There was a “consensus” that lower path of OCR relative to February MPS was “appropriate”. That reflects “weaker domestic spending” and “projected ongoing growth and employment headwinds”. A key downside risk to growth was “larger than anticipated slowdown in global economic growth, particularly in China and Australia, New Zealand’s largest trading partners.”

In the latest economic projections, RBNZ projected that inflation will stay below target for longer then in February MPS. CPI won’t breaks 2% level until 2022. CPI forecasts for 2019 and 2021 were both revised down. On growth, RBNZ sees slower GDP growth in 2019 and 2020. But GDP growth is expected to pick up solidly in 2021 before dipping in 2022. On the net, RBNZ sees the need for further rate cut with average OCR hitting 1.4% in 2021 before bottoming.

OCR year average (vs Feb projections): 2019 at 1.8% (unchanged); 2020 at 1.6% (revised down from 1.8%); 2021 at 1.4% (revised down from 1.8%); 2022 at 1.6% (revised down from 2.2%);

CPI (vs Feb projections): 2019 at 1.5% (revised down from 1.6%); 2020 at 1.9% (revised up from 1.7%); 2021 at 1.9% (revised down from 2.1%); 2022 at 2.1% (unchanged).

GDP growth(vs Feb projections): 2019 at 2.6% (revised down from 2.8%); 2020 at 2.6% (revised down from 2.9%); 2021 at 3.1% (revised up from 2.8%); 2022 at 2.5% (revised up from 2.3%).

More on RBNZ:

- RBNZ Cut Policy Rate to 1.5%, Resuming Rate Cut for the First Time since 2016

- First Impressions: RBNZ Cuts the OCR to 1.50%

- RBNZ Cut Rates To A Historic Low | NZD/USD

- RBNZ projects below target inflation for longer, sees need for more easing

BoJ Minutes: Firm domestic demand offset drag from overseas slowdown

Minutes of the March 14/15 BoJ meeting noted that members “concurred” that the economy will continue to its “moderate expansion”. “domestic demand was likely to follow an uptrend”, including fixed investment and private consumption. That should offset weakness in exports and product as dragged down by overseas slowdown.

On prices, members reiterated that CPI ‘continued to show relatively weak developments compared to the economic expansion and the labor market tightening.” But CPI is still “likely to increase gradually” toward 2% target.

On monetary policy, members agreed that it was “appropriate” to persistently continue with the powerful monetary easing under the current guideline. On member warned of the “side effects” of maintaining current easing. One member warned that if downside risks were materializing, BoJ should be prepared to make policy responses. One member also noted the importance to “preemptive policy responses” in case of phase shift in developments.

Also from Japan, monetary base rose 3.1% yoy in April versus expectation of 3.6% yoy.

China trade surplus shrank again as exports contracted in April

China’s trade surplus shrank again in April to USD 13.84B, down from USD 32.67B and missed expectation of USD 34.56B. Exports dropped -2.7% yoy versus expectation of 3.0% yoy. On the other hand, imports rose 10.3% yoy versus expectation of -3.0% yoy.

In CNY terms, trade surplus narrowed sharply to CNY 93.57B, down from 221.23B, missed expectation of CNY 216.75B. Exports grew merely 3.1% yoy versus expectation of 8.0% yoy. Imports rose 10.3% yoy versus expectation of 3.0% yoy.

Elsewhere

UK BRC retail sales monitor rose 3.7% yoy in April versus expectation of 2.4% yoy. Swiss will release unemployment rate in European session. Germany will release industrial production. ECB will also publish monetary policy meeting accounts. Later in the day Canada housing starts will be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.98; (P) 110.43; (R1) 110.70; More…

USD/JPY drops sharply to as low as 109.90 so far today. Intraday bias remains on the downside for 109.71 support next. As noted before, rebound from 104.69 has completed at 112.40 on bearish divergence condition in daily MACD. Decisive break of 109.71 will confirm this bearish case and target retesting 104.69 low. On the upside, break of 110.95 resistance is needed to confirm completion of the fall. Otherwise, outlook will now remain cautiously bearish in case of recovery.

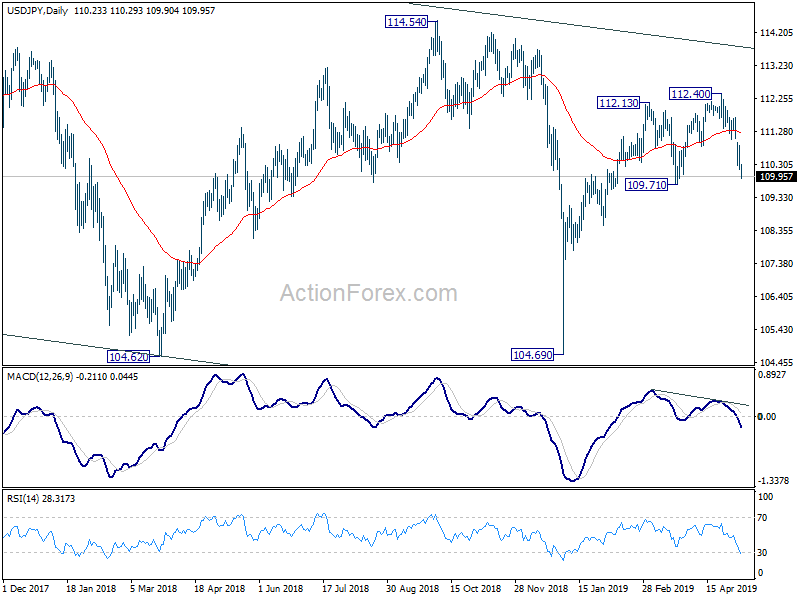

In the bigger picture, medium term outlook in USD/JPY remains a bit mixed as it’s staying inside falling channel from 118.65, but there are signs of bullish reversal. On the upside, break of 114.54 resistance will revive the case the corrective fall from 118.65 has completed with three waves down to 104.69. And whole rise from 98.97 (2016 low) is resuming for 118.65 and above. However, sustained break of 109.71 will raise the chance that fall from 118.65 is still in progress for another low below 104.62.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Apr | 3.70% | 2.40% | -1.10% | |

| 23:50 | JPY | BOJ Minutes Mar | ||||

| 23:50 | JPY | Monetary Base Y/Y Apr | 3.10% | 3.60% | 3.80% | |

| 02:00 | NZD | RBNZ Rate Decision | 1.50% | 1.50% | 1.75% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 03:00 | CNY | Trade Balance (USD) Apr | 13.8B | 33.7B | 32.6B | |

| 03:00 | CNY | Imports (USD) Y/Y Apr | 4.00% | -2.00% | -7.60% | |

| 03:00 | CNY | Exports (USD) Y/Y Apr | -2.70% | 3.00% | 14.20% | |

| 03:00 | CNY | Trade Balance (CNY) Apr | 94B | 235B | 221B | |

| 03:00 | CNY | Imports Y/Y (CNY) Apr | 10.30% | -3.00% | -1.80% | |

| 03:00 | CNY | Exports Y/Y (CNY) Apr | 3.10% | 8.00% | 21.30% | |

| 05:45 | CHF | Unemployment Rate Apr | 2.40% | 2.40% | ||

| 06:00 | EUR | German Industrial Production M/M Mar | -0.50% | 0.70% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:15 | CAD | Housing Starts Apr | 194K | 193K | ||

| 14:30 | USD | Crude Oil Inventories | 9.9M |

{kind=link}