Dollar’s rally attempt faltered overnight as dragged down by steep decline in treasury yields. Dollar index did hit new high at 98.37 but closed sharply lower at 97.85. 10-year yield dropped -0.097 to close at 2.296, just inch above day low at 2.294. Concerns over prolonged US-China trade war dragged down sentiments as a whole. Trump repeatedly tried to sound upbeat on the negotiations but nobody is listening. The Markit PMIs for US released overnight showed deep deterioration in confidence. Upcoming data from the US will be crucial to market outlook beyond Q2.

In the currency markets, Dollar is trading to regain some ground today but lacks follow through buying. For now, Yen is the strongest one for today and looks set to extend recent rally. Australian Dollar is the weakest one for today on talks that RBA could cut as many as three times this year. For the week, Swiss Franc and Yen remain the strongest ones on risk aversion. Sterling is the weakest as Prime Minister Theresa May will most surely step down in June while risk of no-deal Brexit is on the rise. Canadian Dollar is second weakest for the week on free fall in oil prices.

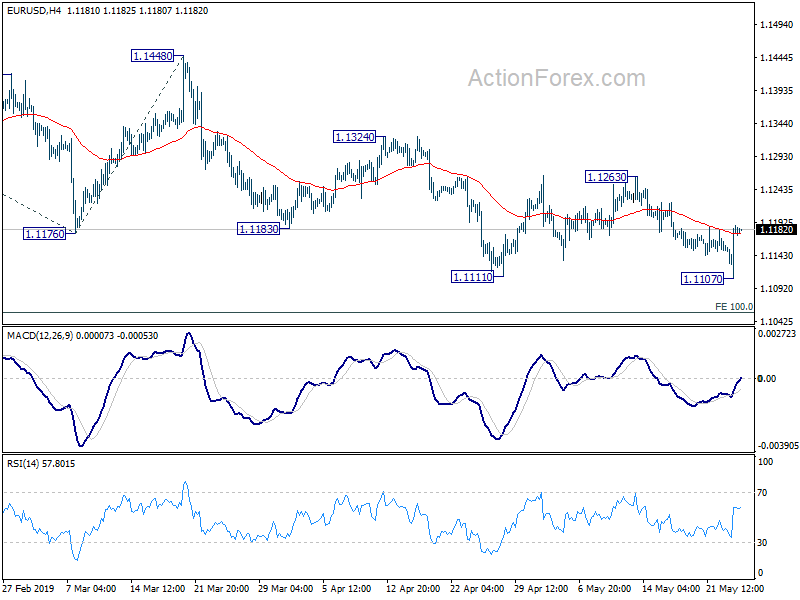

Technically, EUR/USD is staying in consolidation from 1.1111 as it recovered strongly after dipping to 1.1107. More recovery would be seen but we don’t expect a break of 1.1263 resistance ahead. USD/CHF decline resumed by taking out 1.0050 and is set to take on 1.0016. fibonacci support. USD/JPY’s break of 109.81 minor support support suggests recent fall is ready to resume through 109.02 low. Ideally, we should also see EUR/JPY breaking through 122.08 temporary low to confirm Yen strength.

In Asia, currently, Nikkei is down -0.43%. Hong Kong HSI is up 0.21%. China Shanghai SSE is down -0.04%. Singapore Strait Times is down -0.29%. Japan 10-year JGB yield is down -0.0104 at -0.07. Overnight, DOW dropped -1.11%. S&P 500 dropped -1.19%. NASDAQ dropped -1.58%. 10-year yield dropped -0.097 to 2.296.

Trump: China trade deal happening fast, dangerous Huawei can be included

Trump sounded upbeat on US-China trade negotiation again even though, for now, there is still no more meeting scheduled. He said a the White House, “it’s happening, it’s happening fast and I think things probably are going to happen with China fast because I cannot imagine that they can be thrilled with thousands of companies leaving their shores for other places.”

He also said Huawei is “very dangerous” if “you look at what they’ve done from a security standpoint, from a military standpoint”. But even though it’s that dangerous Trump said “If we made a deal, I could imagine Huawei being possibly included in some form or some part of it”.

But separately, the Commerce Department laid out a proposal in a Federal Register notice yesterday, on punishing currency manipulating countries with tariffs. Commerce Secretary Wilbur Ross said “this change puts foreign exporters on notice that the Department of Commerce can countervail currency subsidies that harm US industries” And, “foreign nations would no longer be able to use currency policies to the disadvantage of American workers and businesses.”

Fed officials expressed concerns over persisting trade tensions

Some Fed officials expressed their concerns over trade tensions and the impact on confidence and the economy at a Dallas Fed conference yesterday.

Dallas Fed President Robert Kaplan said “I’m watching very carefully how these trade tensions unfold because I have a concern.. whether that could cause some deceleration in the rate of growth.” And, “new development over the last month has been increased trade tensions and more business uncertainty, and it’s going to take a little while to sort out how that might unfold, or how long that might last.”

San Francisco Fed President Mary Daly said for now “the data is good, but the mood is teetering”. The economy’s momentum would be an upside risk to growth ” if we get a relaxation or a reduction in the uncertainty”. However, she warned that if uncertainties persist, “that’s a downside to the economy, because the uncertainty has real effects, but it also has effects on confidence, and that confidence feeds back into investment.”

Richmond Fed President Thomas Barkin and Atlanta Fed President Raphael Bostic also warned that uncertainties around trade could hurt growth.

UK PM May said to announce exit date today, Sterling decline slowing but no bottoming

It’s widely reported that UK Prime Minister Theresa May will finally announce her exit date on Friday. The resignation as Conservative Leader could take effect on June 10, paving the way for leadership contest. May could stay on as caretaker Prime Minister until a new one is elected, which may take up to six week’s time.

At this point, Boris Johnson is the favorite among pro-Brexit Conservatives, for winning back support that swung to Nigel Farage’s Brexit party. But there are also deep concerns with centrist and pro-EU party members that Johnson will eventually take UK into a no-deal Brexit that he prefers.

Other possible candidates include Michael Gove, Foreign Minister Jeremy Hunt, former Leader of the House of Commons Andrea Leadsom, former Brexit Minister Dominica Raab.

Sterling’s decline slowed a little bit today but there is no clear sign of bottoming yet. We’d expect more downside in the Pound until at least it becomes clear who’ll be the next Prime Minister.

Westpac forecasts three RBA cuts this year, QE becomes attractive in 2020

AUD/USD recovered overnight as Dollar was dragged down by heavy decline in treasury yields. US 10-year yield ended down as much as -0.097 at 2.296, showing steep downside acceleration. However, recovery in AUD/USD was relatively limited and it’s indeed back under pressure today as Westpac now forecasts three rate cuts by RBA this year, with possibility to start QE in 2020.

On the economy, Westpac sees unemployment rate drifting up to 5.4% by year end, growth as 2.2% for 2019 and underlying inflation at merely 1.4%. Housing market is expected to stay weak despite some stabilization. After RBA Governor Philip Lowe’s speech earlier this week Westpac believed that a June cut is a certain, and the second will come in August. Based on the weak outlook, a third in November to 0.75% is expected too.

Westpac also noted that some form of Quantitative Easing is an option for RBA if there is need to ease policy further. For now, RBA’s own research suggests that policy transmission mechanism will still have some effect at a cash rate below 1%. However, in 2020, the case for QE will become more attractive.

On the data front

New Zealand trade surplus narrowed to NZD 433M in April, above expectation of NZD 400M. Japan national CPI core accelerated to 0.9% yoy in April, up from 0.8% yoy and matched expectations. UK retail sales will catch some attention today but main focus will be on May’s announcement. US will release durable goods orders in US session.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1130; (P) 1.1159; (R1) 1.1210; More…..

EUR/USD breached 1.1111 to 1.1107 but recovered strongly since then. The development suggests that consolidation from 1.1111 is extending and intraday bias remains neutral first. While further rise cannot be ruled out, upside should be limited by 1.1263 resistance to bring down trend resumption eventually. ON the downside, firm break of 1.1107 will resume the larger down trend from 1.2555. Next target will be 100% projection of 1.1448 to 1.1183 from 1.1324 at 1.1059. However, sustained break of 1.1263 resistance will now and early sign of trend reversal and turn bias to the upside for 1.1448 key resistance.

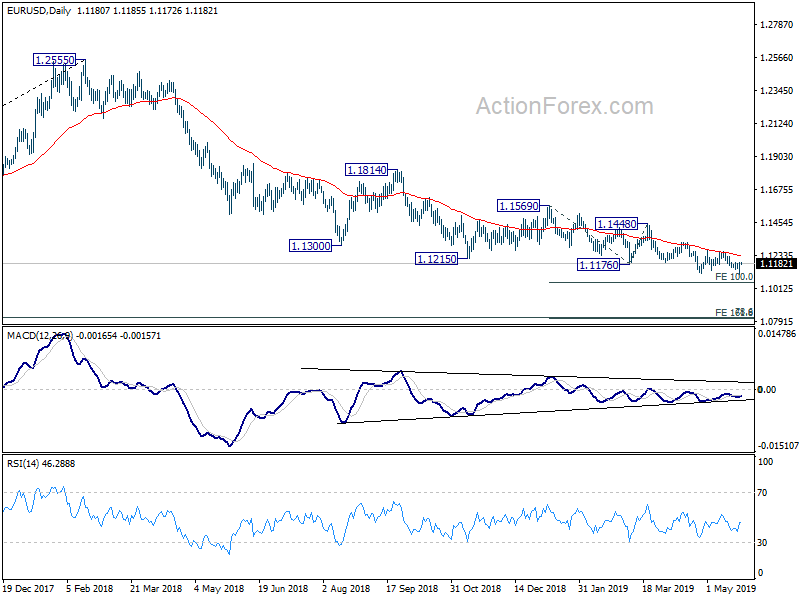

In the bigger picture, down trend from 1.2555 (2018 high) is still in progress. Such decline would target 78.6% retracement of 1.0339 (2016 low) to 1.2555 (2018 high) at 1.0813 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1448 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Apr | 433M | 400M | 922M | 824M |

| 23:30 | JPY | National CPI Core Y/Y Apr | 0.90% | 0.90% | 0.80% | |

| 5:30 | JPY | All Industry Activity Index M/M Mar | -0.20% | -0.20% | ||

| 8:30 | GBP | Retail Sales Ex Auto Fuel M/M Apr | -0.50% | 1.20% | ||

| 8:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Apr | 4.30% | 6.20% | ||

| 8:30 | GBP | Retail Sales Inc Auto Fuel M/M Apr | -0.40% | 1.10% | ||

| 8:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Apr | 4.50% | 6.70% | ||

| 10:00 | GBP | CBI Reported Sales May | 6 | 13 | ||

| 12:30 | USD | Durable Goods Orders Apr P | -2.00% | 2.60% | ||

| 12:30 | USD | Durables Ex Transportation Apr P | 0.20% | 0.30% |

{kind=link}