Risk sentiments stabilized somewhat in Asian session today. While major Asian indices are down, losses are so far limited. Late buying in the US overnight argues that the markets are not in a crash yet despite all the talks on trade war escalation. DOW has indeed reached as low as 24938.24 but recovered to close at 25126.41, defended 25000 handle and down only -0.87%. Nevertheless, it’s now a given that US-China trade war to staying for now. And, it should be just a matter of time when data finally show the deterioration in global economic outlook.

In the currency markets, Australian Dollar leads commodity currencies higher today. Yen and Dollar are so far the weakest ones. For the week, Australian Dollar is also the strongest, followed by Dollar and then Yen. Sterling is the weakest one for the week so far, followed by Euro and then Swiss Franc.

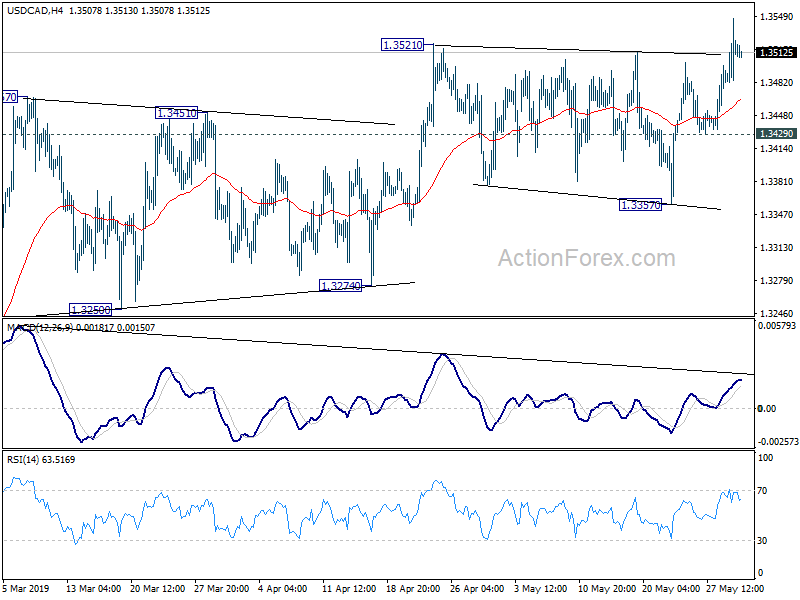

Technically, USD/CAD’s breach of 1.3521 suggests that recent rise from 1.3068 is resuming, even though upside momentum is weak. USD/JPY recovered ahead of 109.02 support. Thus, recent fall from 112.40 is not ready to resume yet. More upside on USD/JPY could help lift EUR/JPY and GBP/JPY for mild recoveries. EUR/GBP is struggling in tight range below 0.8840 resistance. GBP/USD is also holding above 1.2605 temporary low. It looks like both EUR/GBP and GBP/USD will continue consolidative trading for a while. But a downside breakout in the Pound in either one might trigger breakout in the other too.

In Asia, Nikkei is currently down -0.46%. Hong Kong HSI is down -0.51%. China Shanghai SSE Is down -0.68%. Singapore Strait Times is down -0.80%. Japan 10-year JGB yield is up 0.015 at -0.078. Overnight, DOW dropped -0.87%. S&P 500 dropped -0.69%. NASDAQ dropped -0.79%. 10-year yield dropped -0.032 to 2.236.

China: US Provoking trade dispute is naked economic terrorism, economic homicide, economic bullying

Rhetorics from Chinese officials regarding trade war with US continued to be hard-line. The ruling Communist Party is clearly preparing their citizens for the “new long march” in prolonged trade war.

Chinese Vice Foreign Minister Zhang Hanhui said today “we oppose a trade war but are not afraid of a trade war.” He went further to accuse the US that “this kind of deliberately provoking trade disputes is naked economic terrorism, economic homicide, economic bullying.”

He added: “This trade clash will have a serious negative effect on global economic development and recovery… We will definitely properly deal with all external challenges, do our own thing well, develop our economy… At the same time, we have the confidence, resolve and ability to safeguard our country’s sovereignty, security, respect and security and development interests.”

Yesterday, stock markets were rocked by news that China is going to weaponize its rare earths in the trade war. The state-run China Daily newspaper said today “it would be naive to think that China does not have other countermeasures apart from rare earths to hand”. “As Chinese officials have reiterated, they have a ‘tool box’ large enough to fix any problem that may arise as trade tensions escalate, and they are ready to fight back ‘at any cost’.”

BoC stood pat and struck a neutral tone

Yesterday, BoC kept overnight rate unchanged at 1.75% as widely expected. The central bank assessed that economic developments were broadly in line with the April MPR, including growth and inflation. While refraining from the comment that interest rate would need to increase, BOC also attempted to temper market speculations that a rate cut would be needed.

BOC concluded that recent slowdown in the economy was driven by “temporary” factor, while “global trade risks” have undeniably increased”. Policymakers judged the “degree of accommodation being provided by the current policy interest rate remains appropriate”, while they pledged to monitor incoming data on future adjustment of the monetary policy.

Despite BOC’s effort to temper the need of a rate cut, the market is obviously unconvinced. Market participants continue to price in about 30% chance of rate cut later this year and USDCAD surged to the highest level since January.

More in Market Not Convinced by BOC’s Intentionally Neutral Tone

BoJ Sakurai: Shouldn’t recklessly seek to hit price target with additional easing

BoJ board member Makoto Sakurai said the central bank “shouldn’t recklessly seek to achieve our price target with additional easing”. Instead, the best monetary policy approach was to “patiently maintain” the current stimulus program. He acknowledged that “achievement of our price target is being delayed”. But that’s because “the relationship between monetary policy and price moves are changing and becoming more complex.”

Sakurai also said BoJ should be very mindful of the negative effects of the ultra-loose monetary policy. He added, “while financial institutions’ capital-to-asset ratios are sufficient from a regulatory standpoint, what’s important to note is that they are declining as a trend.” Hence, “the BoJ must make appropriate policy decisions by scrutinizing the merits and demerits, including the risk our policy is building up financial imbalances.”

Australia building approvals dropped -4.7% mom, capital expenditure dropped -1.7%

Australia dwelling approvals contracted by -4.7% mom in seasonally adjusted terms in April. That’s well below expectation of 0.0% mom. Regionally, the decline was driven by falls in Tasmania (19.1%), Victoria (16.1%), Western Australia (6.7%) and South Australia (3.3%). Private dwellings excluding houses fell 6.5% while private house approvals decreased 2.6%.

Seasonally adjusted new capital expenditure dropped -1.7% in Q1, also way below expectation of 0.5% qoq. Buildings and structures fell -2.8% while equipment, plant and machinery fell -0.5%

Looking ahead

The calender is empty in European session with Swiss, France and Germany on bank holiday. Later in the day, US will release GDP revision, trade balance, jobless claims, wholesale inventories and pending home sales. Canada will release current account balance.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3485; (P) 1.3516; (R1) 1.3551; More…

USD/CAD rose to as high as 1.3546 and the breach of 1.3521 resistance suggests that larger rise from 1.3068 is resuming. Intraday bias is back on the upside for retesting 1.3664 high. For now, break of 1.3429 support is needed to be the first sign of near term reversal. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, USD/CAD is staying well inside medium term rising channel (support at 1.3321). Thus, the up trend from 1.2061 (2017 low) should be in progress. On the upside, decisive break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will pave the way to 78.6% retracement at 1.4127 next. This will remain the favored case as long as 1.3068 support holds. However, sustained break of the channel support will be the first sign of medium term reversal. Firm break of 1.3068 would confirm.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Apr | -7.90% | -6.90% | -7.40% | |

| 1:30 | AUD | Private Capital Expenditure Q1 | -1.70% | 0.50% | 2.00% | 1.30% |

| 1:30 | AUD | Building Approvals M/M Apr | -4.70% | 0.00% | -15.50% | -13.40% |

| 12:30 | CAD | Current Account Balance Q1 | -17.9B | -15.5B | ||

| 12:30 | USD | GDP Annualized Q/Q Q1 S | 3.10% | 3.20% | ||

| 12:30 | USD | GDP Price Index Q1 S | 0.90% | 0.90% | ||

| 12:30 | USD | Initial Jobless Claims (MAY 25) | 214k | 211k | ||

| 12:30 | USD | Continuing Claims (MAY 18) | 1676k | |||

| 12:30 | USD | Advance Goods Trade Balance Apr | -72.0B | -71.4B | ||

| 12:30 | USD | Wholesale Inventories M/M Apr P | 0.10% | -0.10% | ||

| 14:00 | USD | Pending Home Sales M/M Apr | 0.50% | 3.80% | ||

| 14:30 | USD | Natural Gas Storage | 100B | |||

| 15:00 | USD | Crude Oil Inventories | 4.7M |

{kind=link}