Sterling trades broadly lower today after data showed unexpected GDP contraction in April. More importantly, the deterioration in manufacturing after Brexit stockpiling appeared to be much worse than expected. Other survey data indicated little recovery momentum in Q2 so far, which could be heading for a contraction. Meanwhile, Australian and New Zealand Dollar are among the weakest ones as China May imports contracted by most contracted by most since July 2016.

Dollar is generally firm as lifted by US-Mexico deal on migration. Trump revealed today that a part of the agreement will need a “vote by Mexico’s legislative body”. He then threatens Mexican lawmakers that “we do not anticipate a problem with the vote but, if for any reason the approval is not forthcoming, tariffs will be reinstated.” But in any case, tariffs threats are averted for now. Canadian and Euro are among the strongest too.

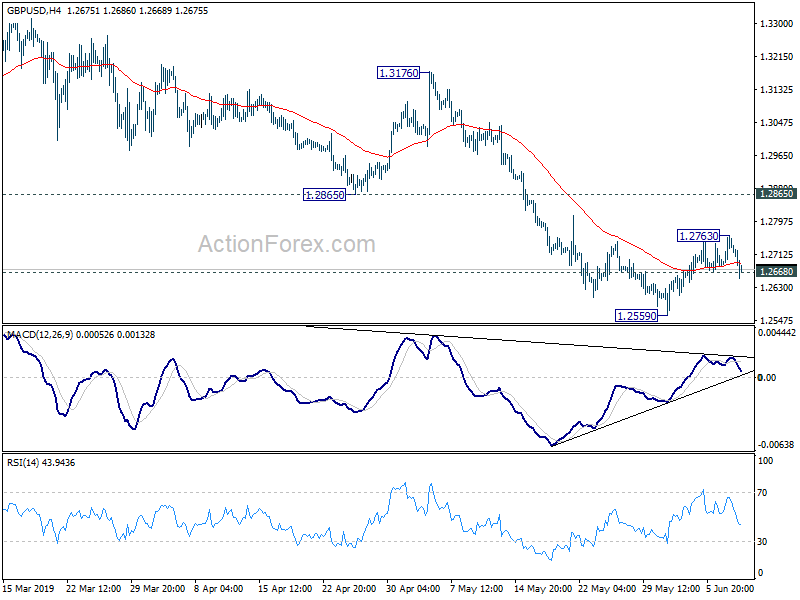

Technically, GBP/USD’s breach of 1.2668 minor support suggests that recovery from 1.2559 has completed earlier than expected at 1.2763. Intraday bias is back on the downside for retesting 1.2559 low. EUR/GBP’s break of 0.8902 temporary top indicates resumption of recent rise towards 0.9101 key resistance. AUD/USD breached 0.6962 minor support too and more downside is in favor. Though, we’d prefer deeper decline to confirm. USD/CHF and USD/JPY are staying in consolidation. EUR/USD is resilient, remains well above 1.1251 minor support. Thus, there is no clear sign of topping in EUR/USD yet.

In other markets, DOW is currently up 170pts or 0.66%. FTSE is up 0.48%. DAX is up 0.77%. CAC is up 0.18%. German 10-year yield is up 0.042 at -0.212. Earlier in Asia, Nikkei rose 1.20%. Hong Kong HSI rose 2.27%. China Shanghai SSE rose 0.86%. Singapore Strait Times rose 0.69%. Japan 10-year JGB yield dropped -0.005 to -0.121.

UK GDP contracted -0.4% in April, widespread weakness across manufacturing

UK GDP contracted -0.4% mom in April, much worse than expectation of -0.1% mom. Index of production dropped -2.7%, manufacturing dropped -3.9% and construction dropped -0.4%. Index of services and agriculture were flat mom. In the three months to April, GDP grew 0.3%, slowed from 0.5% in the period from January to March..

Head of GDP Rob Kent-Smith said: “GDP growth showed some weakening across the latest 3 months, with the economy shrinking in the month of April mainly due to a dramatic fall in car production, with uncertainty ahead of the UK’s original EU departure date leading to planned shutdowns. There was also widespread weakness across manufacturing in April, as the boost from the early completion of orders ahead of the UK’s original EU departure date has faded.”

In April, UK industrial production dropped -2.7% mom, -1.0% yoy, much worse than expectation of -1.0% mom, 0.9% yoy. Manufacturing production dropped -3.9% mom, -0.% yoy, also way below expectation of -1.4% mom, 2.0% yoy. The contraction in manufacturing sector was the worst since June 2002 and the impact of Golden jubilee shutdowns. Also from UK, visible trade deficit narrowed to GBP -12.1B in April versus expectation of GBP -13.1B.

NIESR: UK GDP to contract -0.2% in Q2 on production and construction

NIESR said the UK economy is course to contract by -0.2% in Q2, “mainly driven by the production and construction sectors”. That would be a “marked slowdown” from Q1 when growth was boosted by pre-Brexit “stockbuilding”. It added that recent surveys suggests “there has not been a material recovery in output in May”.

Garry Young, Head of Macroeconomic Modelling and Forecasting, said “The latest GDP data were weaker than expected, partly reflecting shifts in production around the original Brexit departure date, including a 24 per cent fall in car manufacturing. The underlying picture is also quite weak, with Brexit-related uncertainty at home and trade tensions abroad dragging on investment spending and economic growth”.

EU Moscovic: G20 in Osaka maybe an important moment for US-China trade resolution

European Economic and Financial Affairs Commissioner Pierre Moscovic said the “road map” is set for G20 to go with “intensified” global trade tension. The two things include ” reforming the World Trade Organization” and “finding bilateral solutions”. Moscovic said G20 members “expect the United States and China to find a way to get to an agreement. Maybe the Osaka summit will be an important moment for that.”

Over the weekend, G20 Finance Ministers the Central bank Governors said in the post-meeting communique that “trade and geopolitical tensions have intensified.” The group pledged to “continue to address these risks, and stand ready to take further action.” However, the originally proposed language of “recognize the pressing need to resolve trade tensions” was dropped.

Italy PM Conte: EU’s EDP would compromise our economic sovereignty

Italian Prime Minister Giuseppe Conte warned of the long lasting impact of EU’s “Excessive Deficit Procedures” in a Corriere della Sera interview. He said if the EDP is opened, it’s “not just a question of a fine”. Italy will be ” subjected to checks and checks for years… compromising our sovereignty in the economic field”. And, the result could “put the savings of Italians at risk.”

China’s trade surplus widened on sharp contraction in imports

China’s import unexpectedly contracted by -8.5% yoy in May. That’s the large contraction since July 2016, indicating underlying weakness in the economy. Exports did unexpectedly rose 1.1% yoy. But that was likely because of front-loading ahead of new US tariffs. Trade surplus, thus, widened to USD 41.7B. Meanwhile, trade with US continued to deteriorate. From January to May, imports dropped US dropped -29.6% yoy while, exports dropped -8.4% yoy, leaving a surplus at USD 110.5B.

In May, in USD term: Exports rose 1.1% yoy to USD 213.9B. Imports dropped -8.5% yoy to USD 172.2B. Total trade dropped -3.4% yoy to USD 386.0B. Trade surplus came in at USD 41.7B, above expectation of USD 23.2B.

From January to May: Exports rose 0.4% yoy to USD 985.3B. Imports dropped -3.7% yoy to USD 827.9B. Total trade dropped -1.6% yoy to USD 1786.2B. Trade surplus was at USD 130.5B.

With EU, YTD: Exports rose 8.0% yoy to USD 167.2B. Imports rose 2.4% yoy to USD 112.9B Total trade rose 5.7% yoy to USD 280.1B. Trade surplus was at USD 54.3B.

With US, YTD: Exports dropped -8.4% yoy to USD 160.1B. Imports dropped -29.6% yoy to USD 49.6B. Total trade dropped -14.5% yoy to USD 209.7B. Trade surplus was at USD 110.5B.

With AU, YTD: Exports rose 3.1% yoy to USD 18.3B. Imports rose 7.7% yoy to USD 46.7B. Total trade rose 6.4% yoy to USD 64.9B. Trade deficit was at USD -28.4B.

From Japan, Q1 GDP growth was finalized at 0.6% qoq, revised up from 0.5% qoq. GDP deflator, however, was revised down to 0.1% yoy, from 0.2% yoy. Bank lending including trusts rose 2.6% yoy in May, excluding trusts rose 2.8% yoy. Current account surplus widened to JPY 1.60T in April.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2697; (P) 1.2730; (R1) 1.2772; More….

GBP/USD’s breach of 1.2668 minor support suggests that corrective recovery from 1.2559 has completed at 1.2763 already. Intraday bias is turned back to the downside for retesting 1.2559 low first. Break will extend the decline from 1.3381 for 1.2391 low first. On the upside, in case of another rise, upside should be limited by by 1.2865 support turned resistance to bring fall resumption eventually.

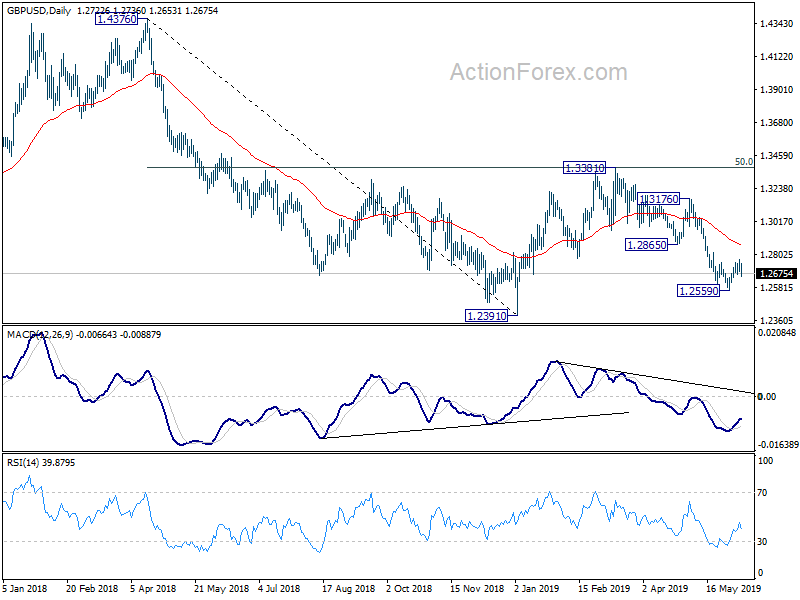

In the bigger picture, medium term decline from 1.4376 (2018 high) is possibly ready to resume. Decisive break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Current Account Total (JPY) Apr P | 1.60T | 1.44T | 1.27T | |

| 23:50 | JPY | GDP Q/Q Q1 F | 0.60% | 0.60% | 0.50% | |

| 23:50 | JPY | GDP Deflator Y/Y Q1 F | 0.10% | 0.20% | 0.20% | |

| 23:50 | JPY | Bank Lending incl Trusts Y/Y May | 2.60% | 2.40% | 2.40% | |

| 23:50 | JPY | Bank Lending Ex-Trusts Y/Y May | 2.80% | 2.50% | ||

| 02:00 | CNY | Trade Balance (USD) May | 41.7B | 23.2B | 13.8B | |

| 02:00 | CNY | Imports (USD) Y/Y May | -8.50% | -3.30% | 4.00% | |

| 02:00 | CNY | Exports (USD) Y/Y May | 1.10% | -3.80% | -2.70% | |

| 02:00 | CNY | Trade Balance (CNY) May | 279B | 136B | 94B | |

| 02:00 | CNY | Imports Y/Y (CNY) May | -2.50% | 5.80% | 10.30% | |

| 02:00 | CNY | Exports Y/Y (CNY) May | 7.70% | 4.70% | 3.10% | |

| 05:00 | JPY | Eco Watchers Survey Current May | 44.1 | 45.5 | 45.3 | |

| 08:30 | GBP | GDP M/M Apr | -0.40% | -0.10% | -0.10% | |

| 08:30 | GBP | Index of Services 3M/3M Apr | 0.20% | 0.20% | 0.30% | |

| 08:30 | GBP | Industrial Production M/M Apr | -2.70% | -1.00% | 0.70% | |

| 08:30 | GBP | Industrial Production Y/Y Apr | -1.00% | 0.90% | 1.30% | |

| 08:30 | GBP | Manufacturing Production M/M Apr | -3.90% | -1.40% | 0.90% | |

| 08:30 | GBP | Manufacturing Production Y/Y Apr | -0.80% | 2.00% | 2.60% | |

| 08:30 | GBP | Construction Output M/M Apr | -0.40% | 0.50% | -1.90% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Apr | -12.1B | -13.1B | -13.7B | -15.4B |

| 12:15 | CAD | Housing Starts May | 202K | 220K | 235K | 233K |

| 12:30 | CAD | Building Permits M/M Apr | 14.70% | 1.80% | 2.10% | 2.80% |

{kind=link}