US stocks closed generally higher overnight even though the rally looks a bit stretched. Positive sentiments continue in Asian session today. Yen is naturally one of the weakest on risk appetite. But Australian and New Zealand Dollar are also among the weakest, continuing recent decoupling with risk markets. We’ll see if such decoupling is developing into a long-lasting trend. Meanwhile, Canadian Dollar and Euro are so far the strongest ones for today.

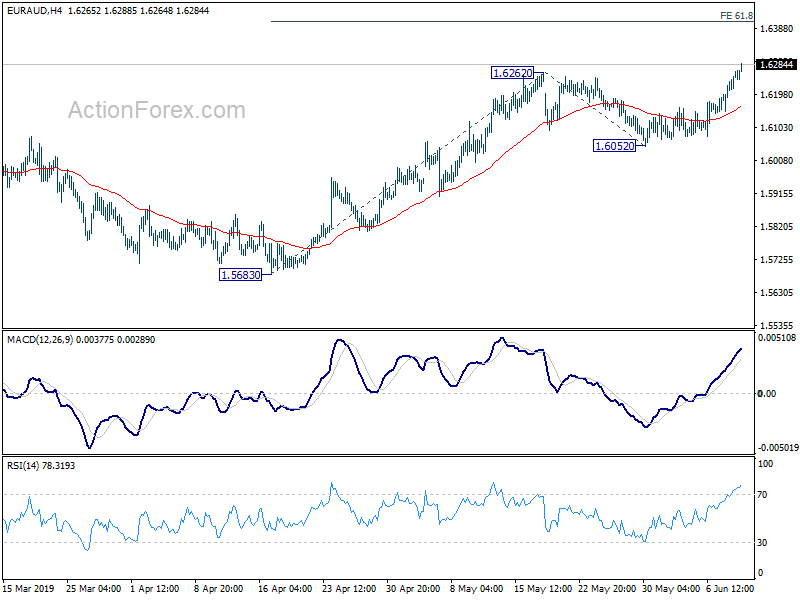

Technically, EUR/AUD’s break of 1.6262 indicates resumption of recent rise from 1.5683 and could be targeting 1.6765 high eventually. AUD/USD’s recovery from 0.6864 should have completed at 0.7022 and deeper fall would be seen back to retest this low. EUR/USD is so far very resistant despite Dollar’s rebound attempts. Euro is partly helped by rises in crosses in particular against Sterling and Aussie. For now, as long as 1.1251 minors support holds, EUR/USD’s rebound from 1.1107 is still in favor to continue.

In Asia, currently, Nikkei is up 0.28%. Hong Kong HSI is up 0.86%. China Shanghai SSE is up 2.01%. Singapore Strait Times is up 0.50%. Japan 10-year JGB yield is up 0.010 at -0.111. Overnight, DOW rose 0.30%. However, it actually closed below open, suggesting temporary topping. S&P 500 rose 0.47%. NASDAQ rose 1.05%. 10-year yield rose 0.059 to 2.143.

Trump expects to meet Xi at G20, or raise tariffs

Trump said yesterday that he and Chinese President Xi are “scheduled to have a meeting” at the G20 summit in Osaka. He added, “We’re expected to meet and if we do that’s fine, and if we don’t — look, from our standpoint the best deal we can have is 25% on $600 billion.”

And, “if we don’t have a deal and don’t make a deal, we’ll be raising the tariffs, putting tariffs on more than — we only tax 35% to 40% of what they said then they had another 60% that’ll be taxed.”

He repeated, “China is going to make a deal because they’re going to have to make a deal”. Also, “at the same time it could be very well that we do something with respect to Huawei as part of our trade negotiation with China. China very much wants to make a deal. They want to make a deal much more than I do, but we’ll see what happens.”

Australia business condition dropped as private sectors continue to lose momentum

Australian NAB Business Condition dropped again in May to 1, down from 3. Private sector continues to lose momentum. Goods distribution industries remain particularly weak, and manufacturing is not far behind. Business Confidence jumped from 0 to 7, in a post-election spike, as well as on RBA rate cut expectations. However, forward looking indicators suggest more weakness lies ahead.

Alan Oster, NAB Group Chief Economist noted “business confidence saw a sharp increase in the month following the Federal election and a confirmation from the RBA that rates would be cut in June. We think this will be a short-term spike given other forward-looking indicators saw further deterioration in the month. Forward orders declined further and in addition to being well below average are negative. Capacity utilisation has also pulled back in 2019 to date and is now a touch below average”.

“While confidence, at least at face value was a positive outcome, business conditions deteriorated further. Trading conditions and profits are particularly weak. The employment index which we are watching closely, partially reversed some of its decline last month, but is only around average”.

Looking ahead

UK employment data will be the major focus in European session. Eurozone will also release Sentix investor confidence. Later in the day, US will release PPI inflation.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6182; (P) 1.6225; (R1) 1.6294; More…

EUR/AUD’s break of 1.6262 resistance indicates resumption of recent rally from 1.5683. Intraday bias is back on the upside for 61.8% projection of 1.5683 to 1.6262 from 1.6052 at 1.6410 first. Break will target 100% projection at 1.6631 next. On the downside, break of 1.6052 support is now needed to indicate short term topping. Otherwise, outlook will remain cautiously bullish in case of retreat.

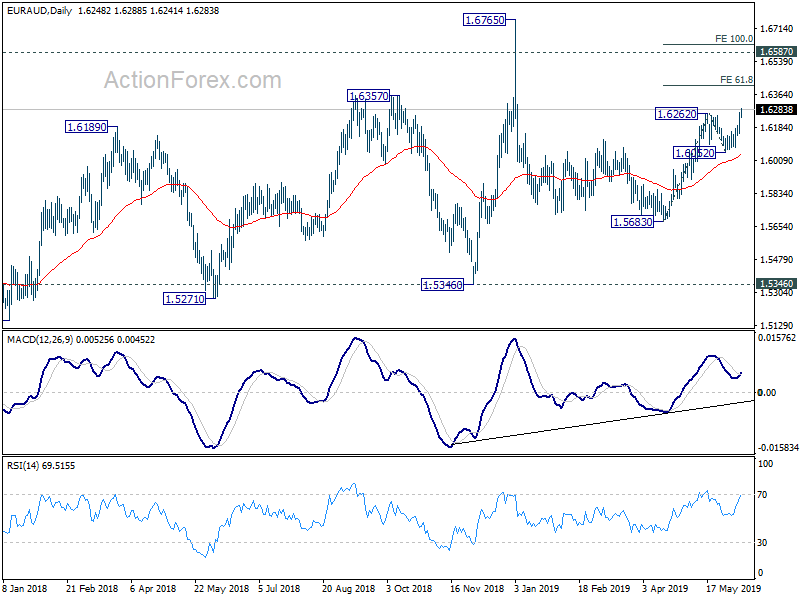

In the bigger picture, as long as 1.5346 support holds, outlook will still remain bullish. Up trend from 1.1602 (2012 low) is expected to resume sooner or later. Break of 1.6765 will target 61.8% retracement of 2.1127 (2008 high) to 1.1602 at 1.7488 next. However, firm break of 1.5346 key support will indicate trend reversal, with bearish divergence condition in weekly MACD, and turn outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | NAB Business Conditions May | 1 | 3 | ||

| 1:30 | AUD | NAB Business Confidence May | 7 | 0 | ||

| 6:00 | JPY | Machine Tool Orders Y/Y May P | -33.40% | |||

| 8:30 | GBP | Jobless Claims Change May | 12.3K | 24.7K | ||

| 8:30 | GBP | Claimant Count Rate May | 3.00% | |||

| 8:30 | GBP | Average Weekly Earnings 3M Y/Y Apr | 3.00% | 3.20% | ||

| 8:30 | GBP | Weekly Earnings ex Bonus 3M Y/Y Apr | 3.10% | 3.30% | ||

| 8:30 | GBP | ILO Unemployment Rate 3Mths Apr | 3.80% | 3.80% | ||

| 8:30 | EUR | Eurozone Sentix Investor Confidence Jun | 2.5 | 5.3 | ||

| 10:00 | USD | NFIB Small Business Optimism May | 101.9 | 103.5 | ||

| 12:30 | USD | PPI M/M May | 0.10% | 0.20% | ||

| 12:30 | USD | PPI Y/Y May | 1.90% | 2.20% | ||

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.10% | ||

| 12:30 | USD | PPI Core Y/Y May | 2.30% | 2.40% |

{kind=link}