Dollar strengthens broadly today and breaks near term support against Euro. There is no clear sign of strength in other pairs yet. More is needed to the greenback to prove itself. Meanwhile, markets remain relatively mixed elsewhere. Canadian Dollar is the strongest yet New Zealand Dollar and Australian Dollar are two of the weakest ones. At the same time, Yen is the second worst performing for today.

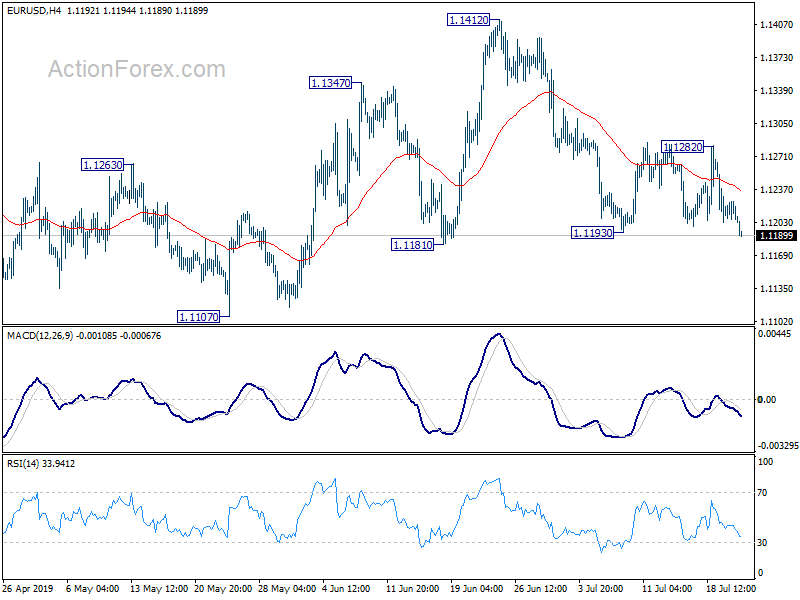

Technically, EUR/USD’s break of 1.1193 suggests resumption of fall from 1.1412. 1.1181 support is next focus, and break will pave the way to retest 1.1107 low. 1.3143 resistance in USD/CAD will be a focus today. Break there will suggest short term bottoming after defending 1.3052/68 cluster support zone. Strong rebound would likely follow for the near term.

In Asia, currently, Nikkei is up 1.20%. Hong Kong HSI is up 0.16%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.29%. Japan 10-year JGB yield is down -0.004 at -0.138. Overnight, DOW rose 0.07%. S&P 500 rose 0.28%. NASDAQ rose 0.71%. 10-year yield dropped -0.005 to 2.043.

RBA Kent: Without rate cuts, Aussie dollar might have been higher

RBA Assistant Governor Kent said in the Q&A of a speech that the exchange rate transmission from interest rate cuts have been “broadly working as you would expect.” Though, the Australian Dollar exchange rate was supported by a “welcome” increase in commodity prices, as well as dovish turn in other major central banks. That came even after the central bank’s back-to-back rate cuts in June and July.

Kent emphasized that “doesn’t mean the reductions in the cash rate here have not had their effect on the exchange rate in the normal way, it’s just that there have been other forces.” And, “you could say well, absent reductions in the cash rate, the Aussie dollar might have been higher.”

On monetary policy, he said RBA is “a long way away from something like” quantitative easing. He noted elsewhere, QE was started “in the depths of the financial crisis when the credit system was quite impaired”. But “that’s not the sort of thing I think people have at the back of their minds here.” And monetary policies should be tailored to “your own economic circumstances”.

Japan FM Aso: We won public trust for sales tax hike

In Japan, Kyodo news reported today that Chief Cabinet Secretary Yoshihide Suga and Finance Minister Taro Aso will likely retain their posts in a cabinet reshuffle. Prime Minister Shinzo Abe said he has noted decided on the cabinet yet, after winning a solid majority in the upper house election on Sunday. The new cabinet will likely be announced in September.

Separately, Aso said after a cabinet meeting that the election gave the ruling coalition a stable political footing. Hence, he said, “I believe we won public trust for the sales tax hike”.

This somewhat echoed Abe’s comment yesterday that based on a stable political basis, the Abe cabinet will take more aggressive and bold economic measures than ever.”

On the data front

The calendar is rather light today. UK will release CBI trends total orders. US will release house price index and existing home sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1202; (P) 1.1213; (R1) 1.1221; More…

EUR/USD’s break of 1.1193 suggests resumption of fall from 1.1412. Intraday bias is back on the downside for 1.1107 low. At this point, we’re not expecting a break there yet. Thus, focus will be on bottoming signal around 1.1107. Though, break of 1.1282 resistance is needed to signal completion of fall from 1.1412. Otherwise, further decline is in favor even in case of recovery.

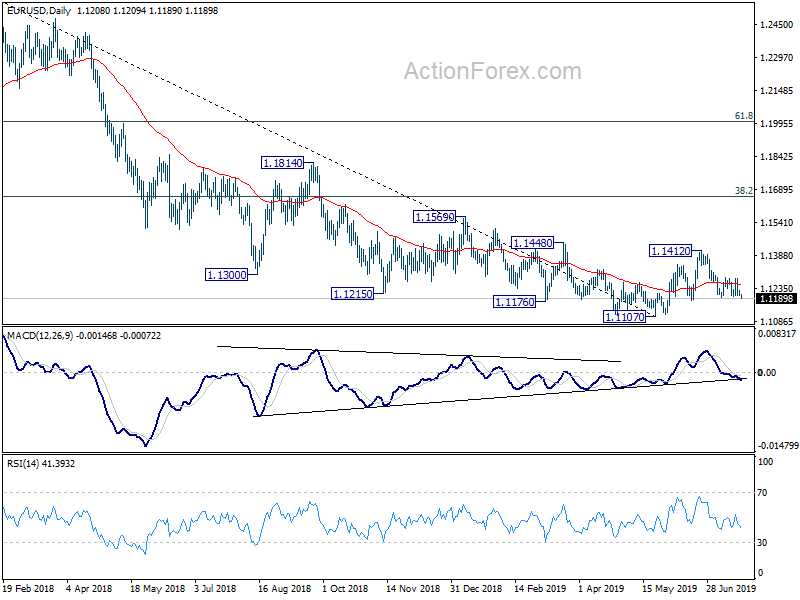

In the bigger picture, on the one hand, 1.1107 is seen as a medium term bottom on bullish convergence condition in weekly MACD. On the other hand, rejection by 55 week EMA retains medium term bearishness. Outlook stays neutral for now. On the downside, break of 1.1107 will resume the down trend from 1.2555 (2018 high) to 78.6% retracement of 1.0339 to 1.2555 at 1.0813. Meanwhile, break of 1.1412 will resume the rebound to 38.2% retracement of 1.2555 to 1.1107 at 1.1660.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 10:00 | GBP | CBI Trends Total Orders Jul | -15 | -15 | ||

| 13:00 | USD | House Price Index M/M May | 0.30% | 0.40% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul A | -7.2 | -7.2 | ||

| 14:00 | USD | Existing Home Sales Jun | 5.35M | 5.34M |

{kind=link}