Swiss Franc and Yen are trading as the strongest for today so far. Both like lifted by somewhat dovish yet balanced central bank decisions. There are no clear indication of imminent policy easing from SNB nor BoJ yet. On other hand, commodity currencies are generally lower as led by Australian, which is pressured by rise in unemployment rate. Sterling closely follows after BoE rate decision trigger little reactions.

Dollar is also slightly softer, following yesterday’s post FOMC rebound. If we purely look at Fed’s dot plot and projections, the mid-cycle adjustment should be completed after yesterday’s rate cut. But decisions would remain heavily dependent on upcoming developments. Focuses are quickly turning to the deputy-level US-China trade talks in Washington.

In Europe, FTSE is currently up 0.66%. DAX is up 0.45%. CAC is up 0.64%. German 10-year yield is up 0.003 at -0.507. Earlier in Asia, Nikkei rose 0.38%. Hong Kong HSI dropped -1.07%. China Shanghai SSE rose 0.46%. Singapore Strait Times dropped -0.25%. Japan 10-year JGB yield dropped -0.0447 to -0.226.

US-China deputy level trade talks to focus heavily on agricultural purchases

Chinese Vice Finance Minister Liao Min is leading a delegation of around 30 Chinese officials to meet with US Deputy Trade Representative Jeffrey Gerrish at the USTR office near White House today. It’s reported that the discussions will focus heavily on agricultural purchases, with some focuses on intellectual property protections and forced technology transfer.

US Commerce Secretary Wilbur Ross said today that “we will find out very, very shortly in the next couple of weeks” on what China exactly wants. But he emphasized that “what we need is to correct the big imbalances, not just the current trade deficit… It’s more complicated than just buying a few more soybeans.”

US initial jobless claims rose 2k to 208k

US initial jobless claims rose 2k to 208k in the week ending September 14, slightly below expectation of 210k. Four-week moving average of initial claims dropped -0.75k to 212.25k. Continuing claims dropped -13k to 1.661m in the week ending September 7. Four-week moving average of continuing claims dropped -3.75k to 1.678m.

Philadelphia Fed Manufacturing index dropped to 12, prices increased notably

Philadelphia Fed Manufacturing Business Outlook Survey Current Index dropped from 16.8 to 12.0 in September, above expectation of 10.8. The survey’s indicators were mixed as the indexes for general activity and new orders fell, while the indexes for shipments and employment increased. Meanwhile, price indexes increased notably.

On the cost side, nearly 38 percent of the firms reported increases in the prices paid for inputs this month, up from 25 percent in August. The prices paid index increased 20 points to 33.0, its highest reading since December 2018. With respect to prices received for firms’ own manufactured goods, 26 percent of the firms reported higher prices, up from 16 percent in August. The diffusion index for prices received increased 8 points to 20.8, its highest reading since March.

BoE kept rate unchanged at 0.75% by unanimous votes

BoE kept bank rate unchanged at 0.75% and held asset purchase target at GBP 435B as widely expected. Both decisions were made by unanimous votes.

The central bank noted that since last meeting US-China trade war has “intensified” and global growth outlook has “weakened”. Monetary policy has been “loosened” in major many economics. Domestically, Brexit developments are making data “more volatile”. Underlying growth has “slowed” but remains “slightly positive”. Brexit uncertainties continued to “weigh on business investment”. But consumption growth has remained “resilient”.

BoE also reiterated that “monetary policy response would not be automatic and could be in either direction.”. In case of smooth Brexit, “increases in interest rates, at a gradual pace and to a limited extent, would be appropriate”.

Also from UK, retail sales including auto/fuel dropped -0.2% mom in August versus expectation of 0.0% mom. Retail sales excluding auto/fuel dropped -0.3% mom versus expectation of 0.0% mom.

Ireland Coveney hasn’t seen any credible proposal on Irish backstop alternatives yet

Irish Foreign Minister Simon Coveney emphasized that EU needs to get “credible proposal” on Irish backstop alternatives. But “we simply haven’t seen yet”, he added. He also said the meeting between Prime Minister Leo Varadkar and DUP’s Arlene Foster was “positive and friendly”. But he emphasized “it is important that its not interpreted as some sort of breakthrough, because I don’t think it is.”

Separately, a European Commission spokesperson said that there is not precise deadline for UK regarding Brexit proposals, but “every day counts”. She added, “we mentioned the European Council in October as a milestone in our calendar so in order to properly prepare a European Council the sooner we make progress the better, but I don’t have a precise date to give you”.

Swiss Franc rebounds on SNB’s less dovish than expected hold

Swiss Franc notably after SNB left policy rate unchanged at -0.75%. The central bank reiterated the commitment to “intervene in the foreign exchange market as necessary, while taking the overall currency situation into consideration”. The so-called exemption threshold for negative interest rates was raised from 20 times of minimum reserve to 25 times. The overall announcement is seen as much less dovish than expected.

Both GDP and CPI forecasts were lowered. GDP growth is expected to reach 0.5-1% this year, down from 1.5% projected in June. CPI is revised lower to 0.4% for this year, down from 0.6% previously. Inflation is expected to ease further to 0.2% in 2020 (previous: 0.7%) before recovering to 0.6% in 2021 (previous 1.1%).

Also from Swiss, trade surplus narrowed to CHF 1.59B in August, below expectation of CHF 3.22B.

BoJ stands pat, global downside risks increasing

BoJ left monetary policy unchanged as widely expected. Under the yield curve control framework, short-term policy rate is kept at -0.1%. The central bank will continue JGB purchases to keep 10-year yield at around 0%. Annual monetary base expansion will be kept at around JPY 80T.

On the outlook, BoJ expects that the economy is “likely to continue on a moderate expanding trend, despite being affected by the slowdown in overseas economies”. Domestic demand is “expected to follow an uptrend”. Exports are “projected to show some weakness”, but still be on a “moderate increasing trend”. CPI is likely to increase “gradually toward 2 percent”.

Risks include US macroeconomic policies, protectionism, emerging markets, global adjustments in IT goods, Brexit and geopolitical risks. BoJ warned that “downside risks concerning overseas economies seem to be increasing, and it also is necessary to pay close attention to their impact on firms’ and households’ sentiment in Japan.”

Australia employment grew 34.7k, unemployment rate rose to 5.3%

Australian employment grew 34.7k in August, well above expectation of 20k. Full-time employment rose 7.2k while part-time employment added 14.7k. Unemployment rate rose 0.1% to 5.3%, above expectation of 5.2%. At the same time, participation rate rose 0.1% to 66.2%.

In seasonally adjusted terms, from July 2019 to August 2019, the largest increases in employment were in Victoria (up 20,300 persons) and New South Wales (up 16,700 persons). The largest decrease was in Queensland (down 7,200 persons). The seasonally adjusted unemployment rate increased by 0.4 pts in South Australia (7.3%) and Tasmania (6.4%), and by 0.1 pts in Victoria (4.9%). Decreases were recorded in New South Wales (down 0.2 pts to 4.3%) and Western Australia (down 0.1 pts to 5.8%), with Queensland recording no change.

New Zealand GDP grew 0.5%, services led

New Zealand GDP grew 0.5% qoq in Q2, above expectation of 0.4% qoq. Services industries grew 0.7%, accelerated from 0.3%. Services growth was also wide-spread, in 8 out of 11 industries. Primary industries expanded 0.7%, rebound from two consecutive declines. However, goods-producing industries fell -0.2%, following 1.9% rise back in Q1.

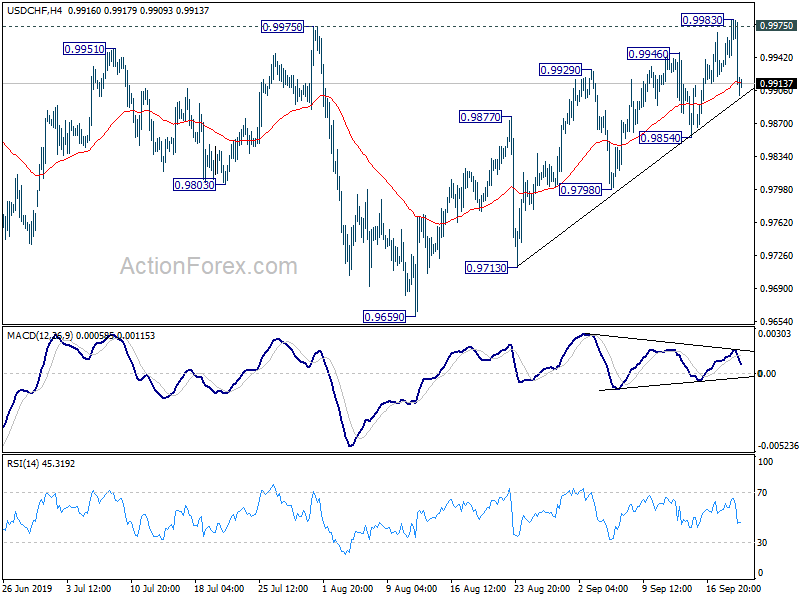

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9940; (P) 0.9962; (R1) 0.9997; More…

USD/CHF drops sharply after failing to sustain above 0.9975 key resistance. But it’s holding above 0.9854 support. Intraday bias remains neutral first. On the upside, decisive break of 0.9975 will confirm completion of fall form 1.0237. Further rally would then be seen to retest this high. On the downside, though, break of 0.9854 will turn intraday bias to the downside for 0.9659 low.

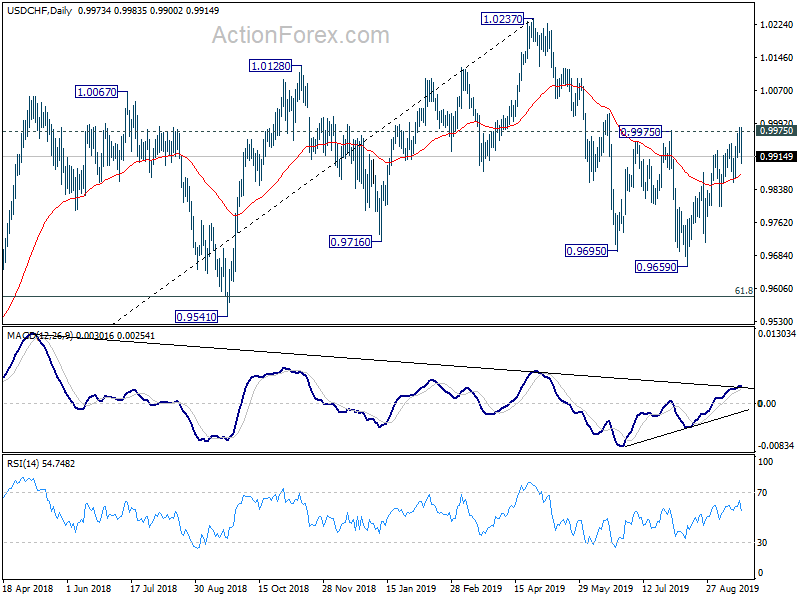

In the bigger picture, the structure of the fall from 1.0237 suggests that it’s a corrective move. Break of 0.9975 will argue that such correction has completed at 0.9659, ahead of 61.8% retracement of 0.9186 to 1.0237 at 0.9587. But decisive break of 1.0237 is needed to indicate up trend resumption. Otherwise, medium term outlook will stay neutral first. Meanwhile, break of 0.9695 support will extend the correction to 0.9541 support instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | 0.50% | 0.40% | 0.60% | |

| 01:30 | AUD | Employment Change Aug | 34.7K | 20K | 41.1K | |

| 01:30 | AUD | Unemployment Rate Aug | 5.30% | 5.20% | 5.20% | |

| 04:30 | JPY | All Industry Activity Index M/M Jul | 0.20% | 0.40% | -0.80% | -0.70% |

| 06:00 | CHF | Trade Balance (CHF) Aug | 1.59B | 3.22B | 3.63B | 3.69B |

| 07:30 | CHF | SNB Policy Rate | -0.75% | -0.75% | -0.75% | |

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 20.5B | 20.3B | 18.4B | |

| 08:30 | GBP | Retail Sales Inc Auto Fuel M/M Aug | -0.20% | 0.00% | 0.20% | 0.40% |

| 08:30 | GBP | Retail Sales Inc Auto Fuel Y/Y Aug | 2.70% | 2.90% | 3.30% | 3.40% |

| 08:30 | GBP | Retail Sales Ex Auto Fuel M/M Aug | -0.30% | 0.00% | 0.20% | 0.40% |

| 08:30 | GBP | Retail Sales Ex Auto Fuel Y/Y Aug | 2.20% | 2.60% | 2.90% | 3.10% |

| 11:00 | GBP | BoE Bank Rate | 0.75% | 0.75% | 0.75% | |

| 11:00 | GBP | BoE Asset Purchase Target Sep | 435B | 435B | 435B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–0–09 | 0–0–09 | 0–0–09 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–09 | 0–0–09 | 0–0–09 | |

| 12:30 | CAD | ADP Payroll Estimates Aug | 49.3K | 73.7K | 30.2K | |

| 12:30 | USD | Current Account Balance (USD) Q2 | -128B | -127B | -130B | -136B |

| 12:30 | USD | Philadelphia Fed Business Outlook Sep | 12 | 10.8 | 16.8 | |

| 12:30 | USD | Initial Jobless Claims (SEP 14) | 208K | 210K | 204K | 206K |

| 14:00 | USD | Leading Index Aug | 0.10% | 0.50% | ||

| 14:00 | USD | Existing Home Sales Aug | 5.39M | 5.42M | ||

| 14:30 | USD | Natural Gas Storage | 75B | 78B |

{kind=link}