Pound stays generally firm in Asian session after yesterday’s rally. UK and EU are getting closer to a Brexit deal and further progress could give Sterling another punch above. As for today, Yen and Swiss Franc are mildly firmer together with dollar. Meanwhile, Australian Dollar and New Zealand Dollars are the weakest. For the week, Sterling and Dollar are so far the strongest while Aussie and Kiwi are the weakest.

Technically, 1.2819 projection level in GBP/USD will be a major focus. Strong break there will confirm upside acceleration and affirm the case of medium term bullish reversal. USD/JPY is facing 109.31 resistance now. Solid break there will affirm the case of medium term bullish reversal too. EUR/AUD has taken out 1.6368 temporary top finally and resumed rise from 1.5905 towards 1.6680/6786 resistance zone. AUD/USD is looking at 0.6710 minor support to confirm overall weakness of Aussie. Break will target 0.6670 low.

In Asia, currently, Nikkei is up 1.27%. Hong Kong HSI is up 0.09%. China Shanghai SSE is down -0.28%. Singapore Strait Times is up 0.55%. Japan 10-year JGB yield is up 0.0075 at -0.164. Overnight, DOW rose 0.89%. S&P 500 rose 1.00%. NASDAQ rose 1.24%. 10-year yield rose 0.038 to 1.771.

Sterling firm despite DUP’s concerns on Johnson’s Brexit concessions

Sterling surged overnight on news that UK and EU are closing in on a Brexit deal in Brussels. The Pound remains firm in Asian session, awaiting further developments. It’s reported that both sides have hammered out most of the differences over the past 48 hours. UK Prime Minister Boris Johnson is said to have made several major concessions. Most notably, he now accepts that there will be customs checks between Northern Ireland and the rest of UK.

Johnson’s move got support from fellow Conservatives. Steve Baker, chairman of the pro-Brexit European Research Group, said “I’m happy to say it was a very constructive conversation” and “I’m optimistic it is possible to reach a tolerable deal which I will be able to vote for.” Irish Prime Minister Leo Varadkar also gave a nod and said “the negotiations are moving in the right direction.”

However, Northern Ireland’s DUP sounds very skeptical on it. Party leader Arlene Foster said “it would be fair to indicate gaps remain and further work is required.” Also, DUP needs “a deal that respects Northern Ireland’s constitutional position as per the Belfast Agreement within the U.K. and indeed respects the economic integrity of the U.K. single market.” Johnson will certainly need support from DUP before giving greenlight to such a deal.

New Zealand CPI slowed to 1.5%, RBNZ expected to cut further

New Zealand CPI rose 0.7% qoq in Q3, above expectation of 0.6% qoq. Annually, CPI slowed to 1.5% yoy, down from 1.7% yoy, but beat expectation of 1.4% yoy. The trimmed-mean measures – which exclude extreme price movements – ranged from 1.7% to 1.8% for the year. This indicates that underlying inflation is higher than the 1.5% overall increase in the CPI. On a quarterly basis, trimmed means ranged from 0.5% to 0.6%.

Separately, RBNZ Deputy Governor Geoff Bascand said in a speech that New Zealand remains vulnerable to external shocks. And, “lower rates still may be needed to achieve our inflation and maximum sustainable employment objectives”. He added that there is reasonable prospect for the cash rate to go lower.

Despite slightly stronger than expected inflation data, RBNZ is still generally expected to cut interest rate further from the current 1.00% level. The need for another shocking -50bps cut, like the one in August, is less likely though. The central bank is now expected to cut another -25bps in November, and probably another -25bps in February.

China warns of countermeasures after US House passed legislations supporting Hong Kong

US House of Representatives passed four measures on Tuesday, on unanimous voice vote, taking a hardline stance on China. In particular, three of the legislations were in support for Hong Kong following over four months of protests. China’s Foreign Ministry immediately responded by accusing the US of “sinister intentions” and warned of retaliation should the acts were passed in the Senate too.

The measures include the Hong Kong Human Rights and Democracy Act that requires the US secretary os state to certify Hong Kong’s autonomy status every year. The Protect Hong Kong Act bans commercial exports of military and crowd-control items to Hong Kong Government. A third measures is a non-binding resolution, condemning China’s interference” in Hong Kong’s affairs and support the city’s right to protest. The fourth measure was another non-binding resolution commending Canada for its actions related to a US request to extradite Meng Wanzhou, CFO of telecom giant Huawei.

China’s Foreign Ministry warned in a brief statement, “if the relevant bill is finally passed into law, not only will it hurt Chinese interests and China-US relations, but also seriously damage US interests. Regarding the wrong decision of the US, the Chinese side will have to enact effective countermeasures, firmly safeguard Chinese sovereignty, security and development interests”.

IMF downgrades global growth forecast to 3% on trade war

IMF warned in the World Economic Outlook that the global economy is in a “synchronized slowdown”. And, thus, global growth forecast for 2019 was downgraded by -0.2% to 3.0%, lowest since global financial crisis. For 2020, growth forecast was also downgraded by -0.1% to 3.4%. IMF said, “growth continues to be weakened by rising trade barriers and increasing geopolitical tensions”. US-China trade tensions alone would “reduce the level of global GDP by 0.8 percent by 2020.”

IMF also warned: “At 3 percent growth, there is no room for policy mistakes and an urgent need for policymakers to support growth. The global trading system needs to be improved, not abandoned. Countries need to work together because multilateralism remains the only solution to tackling major issues, such as risks from climate change, cybersecurity risks, tax avoidance and tax evasion, and the opportunities and challenges of emerging financial technologies.”

Looking ahead

Inflation data will be the major focuses for today. UK will release CPI, RPI and PPI. Given current Brexit optimism, any upside surprises there would give the Pound another lift. Eurozone will release trade balance and September CPI final. Later in the day, Canada will also release CPI. There is prospect of another rebound in Loonie on upside surprises, as recent strong job data already dented chance of BoC rate cut. US will release retail sales, business inventories and NAHB housing index.

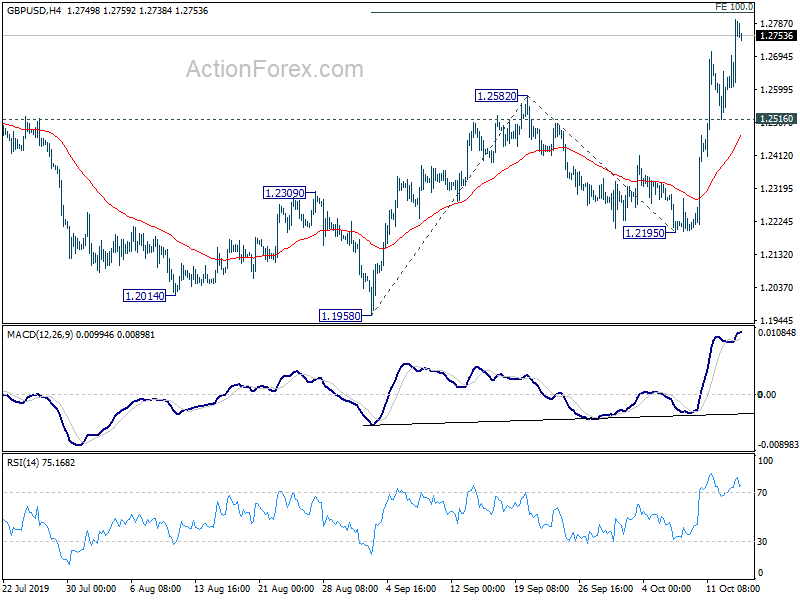

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2659; (P) 1.2729; (R1) 1.2856; More….

Intraday bias in GBP/USD remains on the upside for the moment. Rise from 1.1958 is targeting 100% projection of 1.1958 to 1.2582 from 1.2195 at 1.2819. Break will target 161.8% projection at 1.3205 next. On the downside, below 1.2516 minor support will turn intraday bias neutral again. But retreat should be contained well above 1.2195 support for another rally.

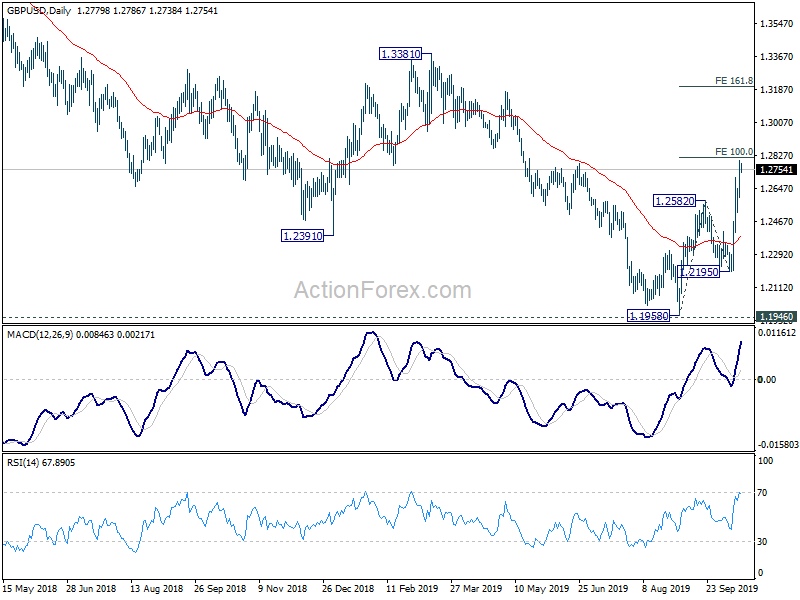

In the bigger picture, current development affirms the case of medium term bottoming at 1.1958, ahead of 1.1946 (2016 low). At this point, rise from 1.1958 is seen as the third leg of consolidation from 1.1946. Further rise would be seen back towards 1.4376 resistance. For now, this will remain the favored case as long as 1.2195 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | 0.70% | 0.60% | 0.60% | |

| 21:45 | NZD | CPI Y/Y Q3 | 1.50% | 1.40% | 1.70% | |

| 23:30 | AUD | Westpac Leading Index M/M Sep | -0.08% | -0.28% | ||

| 8:30 | GBP | DCLG House Price Index Y/Y Aug | 1.20% | 0.70% | ||

| 8:30 | GBP | CPI M/M Sep | 0.20% | 0.40% | ||

| 8:30 | GBP | CPI Y/Y Sep | 1.80% | 1.70% | ||

| 8:30 | GBP | Core CPI Y/Y Sep | 1.70% | 1.50% | ||

| 8:30 | GBP | RPI M/M Sep | -0.10% | 0.80% | ||

| 8:30 | GBP | RPI Y/Y Sep | 2.70% | 2.60% | ||

| 8:30 | GBP | PPI – Input M/M Sep | 0.30% | -0.10% | ||

| 8:30 | GBP | PPI – Input Y/Y Sep | -1.80% | -0.80% | ||

| 8:30 | GBP | PPI – Output Y/Y Sep | 1.30% | 1.60% | ||

| 8:30 | GBP | PPI – Output M/M Sep | 0.10% | -0.10% | ||

| 8:30 | GBP | PPI – Core Output M/M Sep | 0.10% | 0.20% | ||

| 8:30 | GBP | PPI – Core Output Y/Y Sep | 1.90% | 2.00% | ||

| 9:00 | EUR | Trade Balance (EUR) Aug | 18.6B | 19.0B | ||

| 9:00 | EUR | CPI M/M Sep F | 0.20% | 0.10% | ||

| 9:00 | EUR | CPI Y/Y Sep F | 0.90% | 0.90% | ||

| 9:00 | EUR | CPI – Core Y/Y Sep F | 1.00% | 1.00% | ||

| 12:30 | USD | Retail Sales M/M Sep | 0.30% | 0.40% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Sep | 0.20% | 0.00% | ||

| 12:30 | CAD | CPI M/M Sep | 0.00% | -0.10% | ||

| 12:30 | CAD | CPI Y/Y Sep | 2.00% | 1.90% | ||

| 12:30 | CAD | CPI Core – Common Y/Y | 1.80% | 1.80% | ||

| 12:30 | CAD | CPI Core – Median Y/Y | 2.10% | 2.10% | ||

| 12:30 | CAD | CPI Core – Trimmed Y/Y | 2.10% | 2.10% | ||

| 14:00 | USD | Business Inventories Aug | 0.30% | 0.40% | ||

| 14:00 | USD | NAHB Housing Market Index Oct | 68 | 68 |