Yen rises notably today as focuses turn back to US-China trade negotiations after central bank activities and economic data releases. There are renewed concerns that even if a phase one deal could be reached, the next phase(s) would be very difficult. Dollar remains generally soft and is currently trading as the weakest for today. Below target inflation reading provide no support to the greenback, as it’s weighed down by post FOMC selloff. Canadian Dollar is also soft after worse than expected GDP data. European majors are generally mixed.

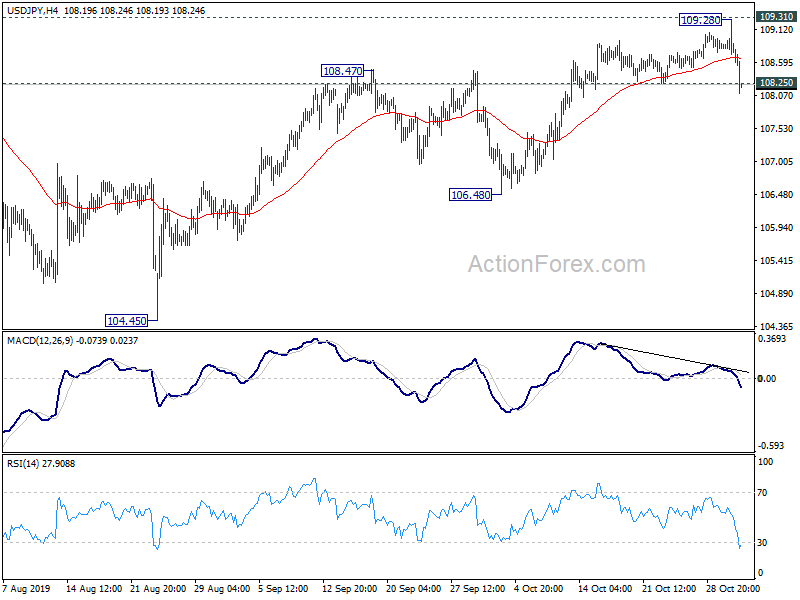

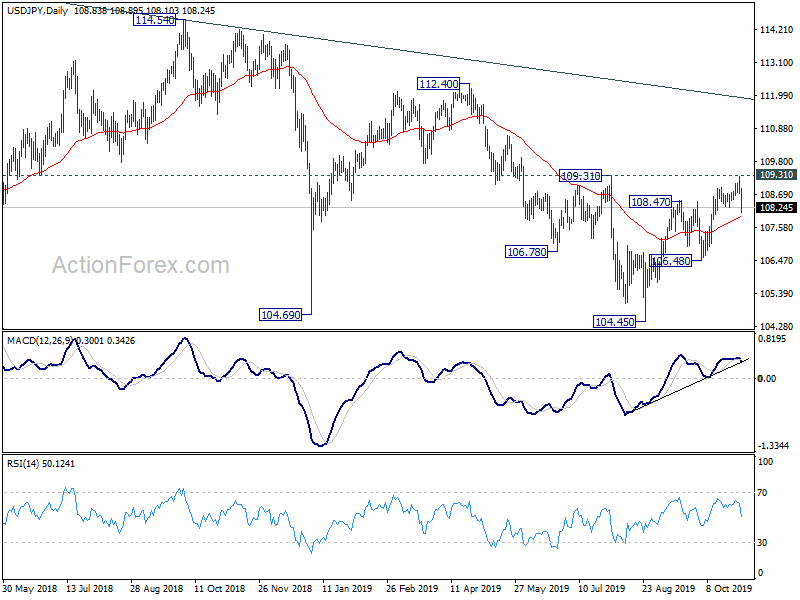

Technically, USD/JPY’s break of 108.25 minor support suggests rejection by 109.31 resistance. More importantly, recent rebound from 104.45 could merely be a correction. break of 106.48 support will reaffirm medium term bearishness and target 104.45 low again. EUR/USD has yet to break through 1.1179 resistance despite yesterday’s rebound. This will remain a focus before weekly close. Break will confirm resume recent rise from 1.0879.

In Europe, currently, FTSE is down -0.88%. DAX is down -0.01%. CAC is down -0.22%. German 10-year yield is down -0.499 at -0.401, back below -0.4 handle. Earlier in Asia, Nikkei rose 0.37%. Hong Kong HSI rose 0.90%. China Shanghai SSE dropped -0.35%. Singapore Strait Times rose 0.68%. Japan 10-year JGB yield dropped -0.0194 to -0.140.

Sentiments weighed down by talk of difficulties in US-China trade talks beyond phase one

Risk sentiments appear to be weighed down by a Bloomberg report that indicated uncertainties over a comprehensive US-China trade deal. Unnamed Chinese officials was said have warned that “they won’t budge on the thorniest issues” regarding trade negotiations. Some officials have “relayed low expectations” on future negotiations unless US would roll back more of the imposed tariffs.

For now, US and China are still on track to complete the phase one of the trade deal based on original time frame, even though the APEC summit in Chile is cancelled due to social unrest. The phase one would cover intellectual property protections, currency, financial services and agricultural purchases. But both sides are said to recognize the difficulties for negotiations beyond that.

To our understanding, the most difficult part would be on subsidies on state-owned enterprises. US would insist on China to reduce the subsidies. But it’s a fundamental principle of the state capitalism model of China that the Chinese Communist Party wouldn’t give up. It’s the key difference between China and Westerns countries which made them systematic rivals, as many described.

US initial jobless claims rose to 218k above expectation of 215k

US initial jobless claims rose 5k to 218k in the week ending October 26, above expectation of 215k. Four-week moving average of initial claims dropped -0.5k to 214.75k. Continuing claims rose 7k to 1.69m in the week ending October 19. Four-week moving average of continuing claims rose 8.75k to 1.686m.

US PCE slowed to 1.4%, core PCE slowed to 1.7%

US personal income rose USD 50.2B or 0.3% mom in September, matched expectations. Personal spending rose 0.2% mom, or USD 24.3B, matched expectations too. Headline PCE price index slowed to 1.3% yoy, down from 1.4% yoy, below expectation of 1.4% yoy. Core PCE price index slowed to 1.7% yoy, down from 1.8% yoy, matched expectations.

Canada GDP grew 0.1% mom in Aug, three month grow slowed to 0.5%

Canada GDP rose 0.1% mom in August, below expectations of 0.2% mom. Goods-producing industries were up 0.2% after two months of declines, led by a rebound in manufacturing, while services-producing industries edged up 0.1%. Overall, there were gains in 14 out of 20 industrial sectors. On a three-month rolling average basis, real gross domestic product rose 0.5% in August, compared with a 0.8% increase in July.

ECB de Guindos: Monetary policy not reached limits, but negative impact increasingly evident

ECB Vice President Luis de Guindos warned that the “collateral effects” of the ultra-loose monetary policy are “increasingly significant”. Hence, monetary policy “can’t be the only response to the economic slowdown” in the Eurozone. He added, “monetary policy can provide liquidity in the case of the risk of Brexit or trade wars, but it’s not the solution to these issues, which are the factors behind the slowdown”. He emphasized, “we can alleviate the situation but we can’t resolve it.”

De Guindos also added that “I wouldn’t say that monetary policy has in any way reached its limits, but I would say that the negative impact on financial stability is increasingly evident, which means it needs to be complemented with fiscal policy.” the advantage of negative rates is that “it has boosted investment, consumption and that’s behind the recovery”. But on the negative side, some real estate markets in Europe are of overly buoyant valuations of assets, and banks’ earnings have also taken a hit.

Separately, Governing Council member Ignazio Visco said “Eurozone inflation remains at an excessively low level and the risk of a de-anchoring of medium-long term expectations is appearing.” He added monetary policy will remain expansionary to sustain demand.

Eurozone GDP grew 0.2% in Q3, CPI slowed to 0.7% in Oct, unemployment unchanged at 7.5%

Eurozone GDP grew 0.2% qoq in Q3, unchanged from Q2’s rate, beat expectation of 0.1% qoq. Over the year, GDP grew 1.1% yoy. CPI slowed to 0.7% yoy in October, down from 0.8% yoy, matched expectation. However, CPI core accelerated to 1.1% yoy, up from 1.0% yoy and beat expectation of 1.1% yoy. Unemployment rate was unchanged at 7.5%, above expectation of 7.4%. That’s still the lowest level since July 2008.

Also released, Italy GDP grew 0.1% qoq in Q3, below expectation of 0.2% qoq. German retail sales rose 0.1% mom in September, below expectation of 0.3% mom. France CPI slowed to 0.9% yoy, missed expectation of 1.1% yoy.

Aussie jumps after strong building permits and receding RBA cut bets

Australian Dollar surges broadly today firstly with the help from post FOMC selloff in Dollar. In the background, Aussie has been riding on optimism towards US-China trade negotiations recently. The strong housing data today also eased concerns of a renewed downturn in the housing markets. Building permits rose 7.6% mom in September, way above expectations of 0.1% mom. Other data, while missed, were not disastrous. Private sector credit rose 0.2% mom in September versus expectation of 0.3% mom. Import price index rose 0.4% qoq in Q3 versus expectation of 0.5% qoq.

As Westpac noted in a report today, RBA should stand pat at its next meeting on November 5. Market pricing of a December cut also dropped from 80% back on October 4 to 25%. But most notably, market pricing of a February cut halved from 100% on October 4 to 50% today. While the pricing of February cut was not Westpac concurs with, that’s a factor in driving the Aussie higher today.

Also from down under, New Zealand building permits rose 7.2% mom in September, above expectation of 2.3% mom. ANZ business confidence rose to -42.4 in October, above expectation of -53.5.

BoJ stands pat, new forward guidance indicates clear easing bias

BoJ left monetary policy unchanged today as widely expected, but stepped up its signal for more easing ahead. Under the yield curve control framework, short term policy interest rate was held at -0.1%. Also, the central back will continue to increase monetary base at JPY 80T a year, with purchases of JGB to keep 10-year yield at around 0%. The decision was made by 7-2 vote, with Y. Harada and G. Kataoka dissenting as usual.

The forward guidance was changed to: “As for the policy rates, the Bank expects short- and long-term interest rates to remain at their present or lower levels as long as it is necessary to pay close attention to the possibility that the momentum toward achieving the price stability target will be lost.” Previously, BoJ said its committed to keep “current ultra-low rates for an extended period of time, at least until the spring of 2020.” It’s a clear message that BoJ is ready to cut interest rates again any time if outlook deteriorates further.

At the post meeting press conference, Governor Haruhiko Kuroda confirmed that the new forward guidance aimed at clarifying the stance that “policy bias is leaning towards additional monetary easing.” Regarding the tools, BoJ could “cut interest rates, increase asset buying or accelerate the pace of increase in base money”.

Also from Japan, industrial production rose 1.4% mom in September, above expectation of 0.4% mom. Housing starts dropped -4.9% yoy in September, above expectation of -6.7% yoy. Consumer confidence rose to 36.2, above expectation of 35.5.

China PMI manufacturing dropped to 49.3, sixth straight months in contraction

China NBS PMI Manufacturing dropped to 49.3 in October, down from 49.8 and missed expectation of 49.8. It’s the sixth straight month of contraction reading. Looking at some details, new export orders dropped for the 17th month to 47.0, down from 48.2. Employment improved slightly but remain deep in contraction at 47.3, up fro 47.0. NBS PMI Non-Manufacturing dropped to 52.8, down from 53.7 and missed expectation of 53.7. It’s also the lowest reading since February 2016.

The overall set of data suggests that while China’s growth is already at lowest pace in 30 years, there is not sign of a turn around yet. The improvements seen back in the end of Q3 were just ripples in a down trend, rather than the start of sustained recovery. The official PMIs will likely remain sluggish in the coming months while a Phase 1 US-China trade deal is unlikely to provide any immediate lift.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.61; (P) 108.95; (R1) 109.18; More…

USD/JPY’s break of 108.25 minor support suggests that a short term top is formed at 109.28, ahead of 109.31 key resistance, on bearish divergence condition. Intraday bias is turned back to the downside for 106.48 support first. Break there will confirm completion of rebound from 104.45 and bring retest of this low. For now, risk will stay on the downside as long as 109.28/31 holds, in case of recovery. However, decisive break of 109.31 will be an early sign of medium term reversal and target 112.40 resistance next.

In the bigger picture, strong support was seen from 104.62 again. Yet, there is no confirmation of medium term reversal. Corrective decline from 118.65 (Dec. 2016) could still extend lower. But in that case, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. Meanwhile, on the upside, break of 112.40 key resistance will be a strong sign of start of medium term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Sep | 7.20% | 2.30% | 0.80% | 0.90% |

| 23:50 | JPY | Industrial Production M/M Sep P | 1.40% | 0.40% | -1.20% | |

| 00:00 | NZD | ANZ Business Confidence Oct | -42.4 | -54.1 | -53.5 | |

| 00:01 | GBP | GfK Consumer Confidence Oct | -14 | -13 | -12 | |

| 00:30 | AUD | Private Sector Credit M/M Sep | 0.20% | 0.30% | 0.20% | |

| 00:30 | AUD | Import Price Index Q/Q Q3 | 0.40% | 0.50% | 0.90% | |

| 01:30 | AUD | Building Permits M/M Sep | 7.60% | 0.10% | -1.10% | -0.60% |

| 02:00 | CNY | Manufacturing PMI Oct | 49.3 | 49.8 | 49.8 | |

| 02:00 | CNY | Non-Manufacturing PMI Oct | 52.8 | 53.7 | 53.7 | |

| 03:30 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 03:30 | JPY | BoJ Outlook Report Q3 | ||||

| 05:00 | JPY | Housing Starts Y/Y Sep | -4.90% | -6.70% | -7.10% | |

| 05:00 | JPY | Consumer Confidence Index Sep | 36.2 | 35.5 | 35.6 | |

| 07:00 | EUR | Germany Retail Sales M/M Sep | 0.10% | 0.30% | 0.50% | -0.10% |

| 07:45 | EUR | France CPI M/M Oct P | -0.10% | -0.30% | -0.40% | |

| 07:45 | EUR | France CPI Y/Y Oct P | 0.90% | 1.10% | 1.10% | |

| 10:00 | EUR | GDP Q/Q Q3 P | 0.20% | 0.10% | 0.20% | |

| 10:00 | EUR | Unemployment Rate Sep | 7.50% | 7.40% | 7.40% | 7.50% |

| 10:00 | EUR | CPI Y/Y Oct P | 0.70% | 0.70% | 0.80% | |

| 10:00 | EUR | CPI – Core Y/Y Oct P | 1.10% | 1.00% | 1.00% | |

| 11:00 | EUR | Italy GDP Q/Q Q3 P | 0.10% | 0.20% | 0.00% | 0.10% |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | -33.50% | -24.80% | ||

| 12:30 | CAD | GDP M/M Aug | 0.10% | 0.20% | 0.00% | |

| 12:30 | CAD | Raw Material Price Index Sep | 0.00% | 2.50% | -1.80% | |

| 12:30 | CAD | Industrial Product Price M/M Sep | -0.10% | 0.20% | 0.20% | |

| 12:30 | USD | Personal Income M/M Sep | 0.30% | 0.30% | 0.40% | 0.50% |

| 12:30 | USD | Personal Spending Sep | 0.20% | 0.30% | 0.10% | 0.20% |

| 12:30 | USD | PCE – Price Index M/M Sep | 0.00% | 0.10% | 0.00% | |

| 12:30 | USD | PCE – Price Index Y/Y Sep | 1.30% | 1.40% | 1.40% | |

| 12:30 | USD | Core PCE – Price Index M/M Sep | 0.00% | 0.10% | 0.10% | |

| 12:30 | USD | Core PCE – Price Index Y/Y Sep | 1.70% | 1.70% | 1.80% | |

| 12:30 | USD | Initial Jobless Claims (Oct 25) | 218K | 215K | 212K | 213 K |

| 12:30 | USD | Employment Cost Index Q3 | 0.70% | 0.70% | 0.60% | |

| 13:45 | USD | Chicago PMI Oct | 47.6 | 47.1 | ||

| 14:30 | USD | Natural Gas Storage | 73B | 87B |

{kind=link}