Sentiments in the markets were lifted by news that China is going to step up credit support to the economy. Commodity currencies strike a strong come back, as led by New Zealand and Australian Dollar. On the other hand, Swiss Franc and Yen are back under pressure. Sterling also continues to pare back some gains as traders hesitate to push it through near term resistance level against Dollar and Yen. The greenback is mixed for the moment, as housing data provide little inspiration.

Technically, bias is GBP/USD and GBP/JPY is turned neutral after they fail to take out 1.3012 and 141.50 resistance levels decisively. Though, further rise remains in favor and these two level will stay in focus. AUD/USD’s recovery from 0.6769 extends higher today but it’s limited below 0.6841 minor resistance so far. Thus, further decline remain in favor to 0.6670 low. Though, break of 0.6841 will turn focus back to 0.6929 resistance instead.

In Europe, currently, FTSE is up 1.08%. DAX is up 0.84%. CAC is up 0.09%. German 10-year yield is up 0.002 at -0.331. Earlier in Asia, Nikkei dropped -0.53%. Hong Kong HSI rose 1.55%. China Shanghai SSE rose 0.85%. Singapore Strait Times dropped -0.61%. Japan 10-year JGB yield dropped -0.0046 to -0.091.

Released in US session, US building permits rose 5% mom to 1.46m annualized rate in October, above expectation of 1.39m. Housing starts rose 3.8% mom to 1.31m, below expectation of 1.32m. Canada manufacturing shipments dropped -0.2% mom in September, above expectation of -0.5% mom.

UK CBI industrial order expectations improved to -26, thick fog of Brexit uncertainty lifted somewhat

UK CBI industrial order expectations improved to -26 in November, up from -37 and beat expectation of -30. 13% of manufacturers reported total order books to be above normal, but 40$ said they were below, giving a rounded balance of -26%. It remains well below long-run average of -13%.

Anna Leach, CBI Deputy Chief Economist, said: “While the thick fog of uncertainty from a No Deal Brexit has lifted somewhat, the manufacturing sector remains under pressure from weak global trade and a subdued domestic economy. Order books remain below average, and output volumes continue to fall. When taking into account the deteriorating outlook for manufacturing globally, it’s clear that the outlook for the sector remains precarious.

“The General Election is an opportunity for all parties to explain how they will shore up our economy. Ratifying a Brexit deal and moving on to build a vibrant future relationship with our biggest trading partner, based on frictionless trade, will be vital – both for UK manufacturers, and business as a whole.”

Also released in European session, Eurozone current account surplus narrowed to EUR 28.2B in September. Swiss trade surplus narrowed to CHF 3.50B in October.

Germany BDI: Manufacturing output to contract -4% this year

Germany’s BDI industry association said that “after six consecutive years of growth, Germany’s industrial sector is stuck in recession since the third quarter of 2018.” Manufacturing output is expected to contract -4% this year, versus 1.2% growth in 2018. Exports will only increase 0.5% in 2019, down from 2.1% in 2018, weakest since global financial crisis in 2009.

BDI also said global industrial output is production and is set to rise 1% this year only, slowed from two years of 3% growth. It added “in industrialized countries, we even expect industrial production to stagnate. In emerging economies, industrial production will only grow by two percent. That’s the lowest production increase in ten years.

China PBoC to step up credit support to the economy

China’s PBoC Governor Yi Gang indicated the central bank will step up credit support to the economy. Yi said during a meeting with commercial banks that capital replenishment will be promoted to increase bank’s lending ability. Additionally, countercyclical adjustments will be stepped up to ensure growth in money supply and social financing.

Markets are expecting PBoC to lower the Loan Prime Rate (LPR) tomorrow, for the third time since it’s introduced the benchmark in August. Yi urged lenders to reference the LPR to set their own lending rates.

BoJ Kuroda: Plenty of scope to deepen negative interest rate

BoJ Governor Haruhiko Kuroda said in the semi-annual parliament testimony that “there is plenty of scope to deepen negative rates from the current -0.1%.” However, he emphasized “I’ve never said there are no limits to how much we can deepen negative rates, or that we have unlimited means to ease policy.”

Kuroda also reiterated that “Japan’s economy is expected to continue expanding and inflation will gradually head towards our 2% target”. And, “we need to remain vigilant to downside risks, particularly those regarding the global economy.” He also noted that “the effect of China’s policy measures is taking somewhat long to appear. But China’s economy will likely sustain growth of around 6% for the time being.”

RBA minutes noted a case to ease further

Australian Dollar stays generally pressured today as RBA’s November meeting minutes struck a more dovish than expected tone. Board members noted that “a case could be made to ease monetary policy”. They refrained from easing further this month because of the concerns about “the negative effects of lower interest rates on savers and confidence”. They, however, retained the view that lower interest rates could support economic growth via traditional channels, such as “a lower exchange rate, higher asset prices and higher cash flows for borrowers.

Suggested readings on RBA:

- RBA Minutes: Members Considered Rate Cut This Month. Disappointing Job Report Raises the Case for Further Easing

- RBA Minutes Signal that the Board is in “Monitoring” Mode

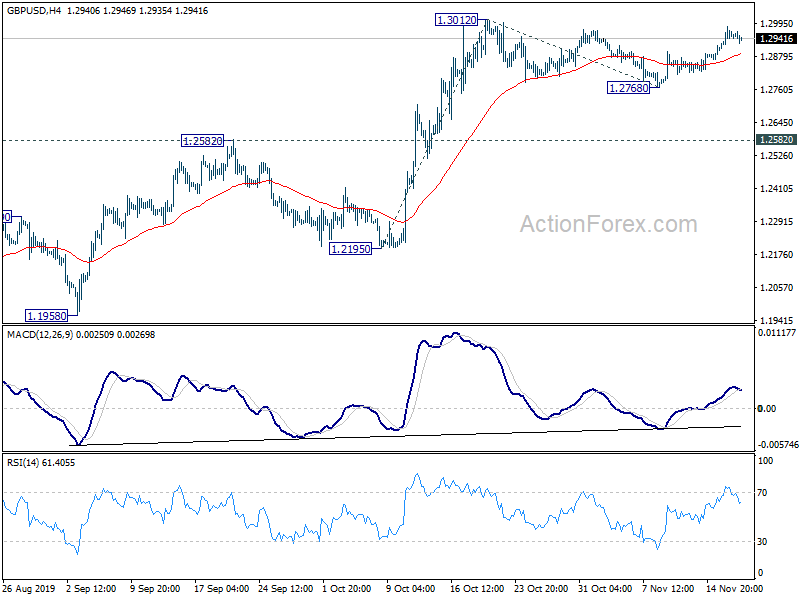

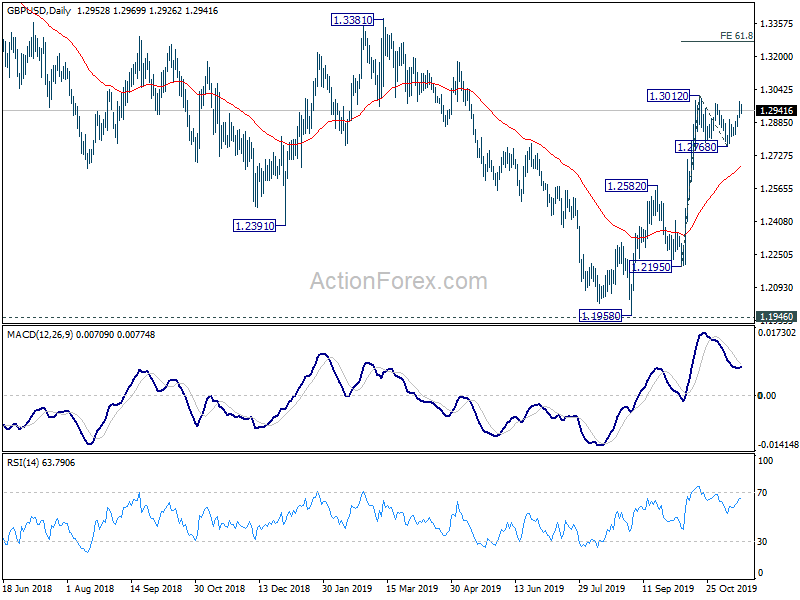

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2914; (P) 1.2949; (R1) 1.2988; More….

GBP/USD’s rally attempt lost momentum as seen in 4 hour MACD. Intraday bias remains neutral with focus on 1.3012 resistance. Firm break there will resume the whole rise from 1.1958. Further rally should be seen to 61.8% projection of 1.2195 to 1.3012 from 1.2768 at 1.3273 next. For now, outlook will remain bullish as long as 1.2768 support in case of retreat. However, break of 1.2768 will bring deeper fall back to 1.2582 resistance turned support.

In the bigger picture, a medium term bottom was formed at 1.1958, ahead of 1.1946 (2016 low). At this point, rise from 1.1958 is seen as the third leg of consolidation from 1.1946. Further rise would be seen back towards 1.4376 resistance. For now, this will remain the favored case as long as 1.2582 resistance turned support holds. However, firm break of 1.2582 will turn focus back to 1.1946 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI – Input Q/Q Q3 | 0.90% | 0.20% | 0.30% | |

| 21:45 | NZD | PPI – Output Q/Q Q3 | 1.00% | 0.40% | 0.50% | |

| 00:30 | AUD | RBA Meeting Minutes | ||||

| 07:00 | CHF | Trade Balance (CHF) Oct | 3.50B | 4.24B | 4.02B | 4.05B |

| 09:00 | EUR | Eurozone Current Account (EUR) Sep | 28.2B | 22.3B | 26.6B | 28.5B |

| 11:00 | GBP | CBI Industrial Order Expectations Nov | -26 | -30 | -37 | |

| 13:30 | USD | Building Permits Oct | 1.46M | 1.39M | 1.39M | |

| 13:30 | USD | Housing Starts Oct | 1.31M | 1.32M | 1.26M | 1.27M |

| 13:30 | CAD | Manufacturing Shipments M/M Sep | -0.20% | -0.50% | 0.80% |

{kind=link}