Euro continues to trade with a soft tone in Asian session, and there is no sign of recovery after yesterday’s post ECB selloff. Australian Dollar is also weak after poor PMI data, even though markets are pushing RBA cut bets from February to April. On the other hand, market concerns over coroanvirus outbreak is somewhat supporting the greenback for now. Over the week, though, Sterling is the strongest followed by Yen. Canadian is the weakest followed by Aussie.

Technically, Euro, Sterling will be the focuses in European session, with important economic data scheduled. EUR/USD is on track to test 1.0981 support. Firm break there would pave the way to retest 1.0879 low later in the month. EUR/JPY might have a take on 120.17 support. Break will be a strong sign of near term bearish reversal. EUR/GBP could take the lead to retest 0.8276 support. GBP/JPY is neutral, stuck in range of 142.80/144.52. A breakout could be seen today.

In Asia, Nikkei rose 0.13%. Hong Kong HSI is up 0.15%. China market is closed. Singapore Strait Times is up 0.17%. Japan 10-year JGB yield is up 0.0025 to -0.021. Overnight, DOW dropped -0.09%. S&P 500 rose 0.11%. NASDAQ rose 0.20%. 10-year yield dropped -0.029 to 1.740.

Coronavirus an emergency in China, but not international health emergency yet

Regarding the new coronavirus outbreak in China, WHO Emergency Committee panel chair Didier Houssin said it’s a “bit too early” to consider it a”Public Health Emergency of International Concern.” It’s now just “an emergency in China”. And, “it has not yet become a global health emergency. It may yet become one.”

As of the situation in China, according to government data, death toll reached 25, with number of confirmed cases exceeding 800. Ten cities in Hubei province are now locked up, with public transportation restrictions, including Wuhan, Huanggang, Xianning, Qianjiang, Xiantao, Ezhou, Chibi, Huangshi, Enshi and Zhijiang.

Japan CPI core accelerated to 0.7%, BoJ minutes show concerns on overseas

Japan national CPI (all-item) accelerated from 0.8% yoy in December, up from 0.5% yoy, beat expectation of 0.7% yoy. CPI core (ex-fresh food), rose to 0.7% yoy, up from 0.5% yoy, beat expectations. CPI core-core (ex-fresh food, energy) also rose to 0.9% yoy, up from 0.8% yoy and matched expectations. While core CPI remains well below BoJ’s 2% target, the pickup should be welcomed by the central bank.

In the minutes of December BoJ meeting, some members expressed concerns that gloomy global outlook could underscores market expectations. A few members noted “considering the risk that overseas economies could recover only to a small extent or slow further, the outlook for exports could not be viewed optimistically.”

Falling global demand might also hurt household income. Some noted that “Close attention should be paid to how developments in corporate profits … would affect winter bonuses.” Capital spending has shown signs of weakness, which is a “matter of concern” too.

Japan PMI composite rose to 51.1, domestic-led economic recovery

Japan PMI Manufacturing rose to 49.3 in January, up from 48.4, beat expectation of 48.7. PMI Services rose notably to 52.1, up from 49.4, back in expansion. PMI Composite also rose to 51.1, up from 48.6, turned into expansion.

Joe Hayes, Economist at IHS Market, said: “Positive signs have emerged for Japan’s economy at the start of 2020, with flash PMI data pointing to a domestic-led economic recovery”. While Q4 would likely post an “ugly decline in GDP”, January PMI will “certainly allay fears” of an “impending technical recession”.

Australia PMI composite dropped to record low 48.6, softness spilled over to 2020

Australia PMI Manufacturing dropped to 49.1 in January, down from 49.2. PMI Services dropped to 48.9, down from 49.8. PMI Composite dropped to 48.6, down from 49.6. That’s the record worst contraction reading since the survey started in May 2016.

CBA Chief Economist, Michael Blythe said: “The January ‘flash’ results show the softness in the Australian economy at the end of 2019 has spilled over into the early part of 2020.” But, “the gloom should not be overdone. Key leading indicators like new orders and employment are showing a notably stronger result than the ‘headline’ PMI readings. And expectations about future business remain at encouraging levels”.

New Zealand CPI rose 0.5% qoq on transport costs, NZD recovers mildly

New Zealand CPI slowed to 0.5% qoq in Q4, down from 0.7% qoq, but beat expectation of 0.4% qoq. Annually, CPI accelerated to 1.9% yoy, up from 1.5% yoy, but missed expectation of 2.2% yoy. Transport cost was a main driver of quarterly inflation pickup, rose 2.1%. Recreation and culture rose 1.6%. Housing and household utilities rose 0.5%. On the other hand, food prices dropped -0.6%.

Looking ahead

PMIs from Eurozone and UK will be the major focuses in European session. Later in the day, Canadian Dollar will look into retail sales for the next move. US will also release PMIs.

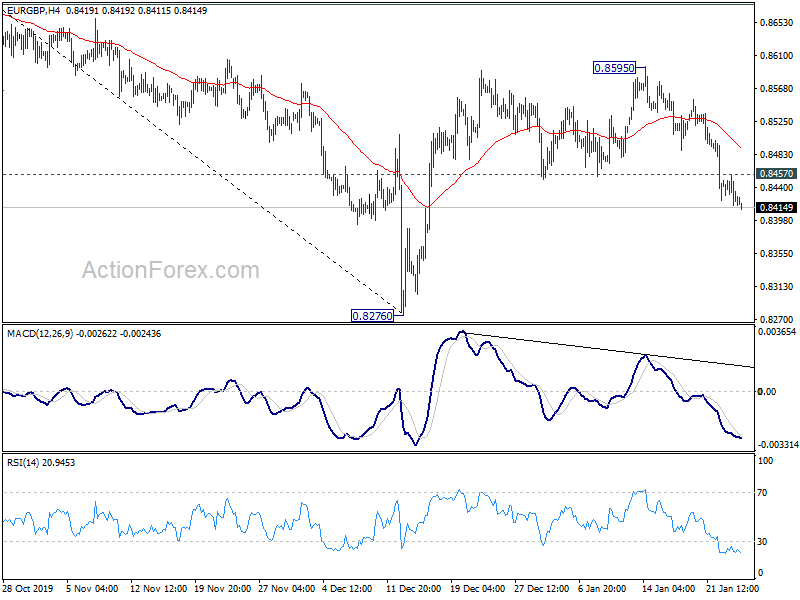

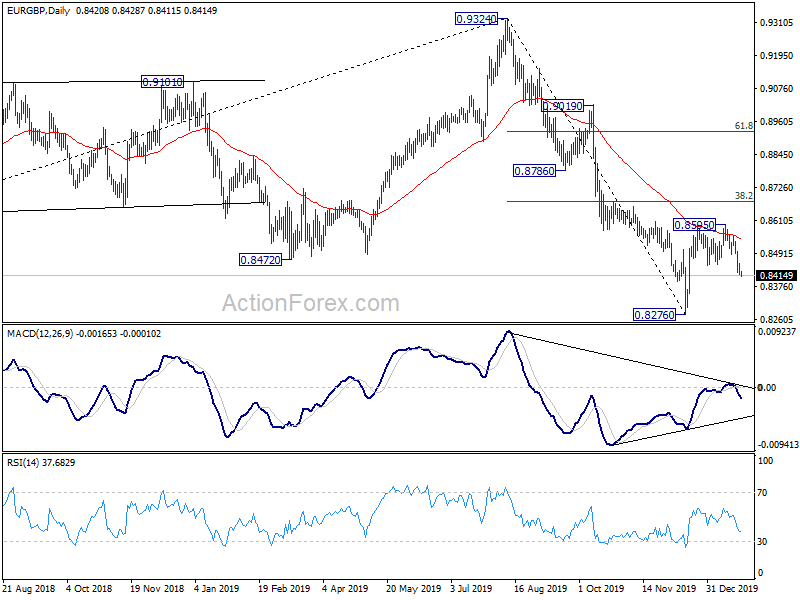

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8408; (P) 0.8433; (R1) 0.8449; More…

Intraday bias in EUR/GBP remains on the downside as fall from 0.8595 is in progress. Corrective rise from 0.8726 should have completed. Further fall would be seen to retest 0.8726 low. Break will resume larger down trend from 0.9324. On the upside, above 0.8457 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8595 resistance holds, in case of recovery.

In the bigger picture, decline from 0.9324 medium term top is till in progress. As long as 0.8786 support turned resistance holds, further fall is expected to 61.8% retracement of 0.6935 to 0.9324 at 0.7848. Nevertheless, break of 0.8786 will argue that fall from 0.9324 has completed and turn focus back to this high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.50% | 0.40% | 0.70% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.90% | 2.20% | 1.50% | |

| 22:00 | AUD | CBA Manufacturing PMI Jan P | 49.1 | 49.2 | ||

| 22:00 | AUD | CBA Services PMI Jan P | 48.9 | 49.8 | ||

| 23:30 | JPY | National CPI Core Y/Y Dec | 0.70% | 0.70% | 0.50% | |

| 0:30 | JPY | Manufacturing PMI Jan P | 49.3 | 48.7 | 48.4 | |

| 8:15 | EUR | France Manufacturing PMI Jan P | 50.5 | 50.4 | ||

| 8:15 | EUR | France Services PMI Jan P | 52.1 | 52.4 | ||

| 8:30 | EUR | Germany Manufacturing PMI Jan P | 44.6 | 43.7 | ||

| 8:30 | EUR | Germany Services PMI Jan P | 54 | 52.9 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Jan P | 46.9 | 46.3 | ||

| 9:00 | EUR | Eurozone Services PMI Jan P | 53 | 52.8 | ||

| 9:30 | GBP | Manufacturing PMI Jan P | 48.8 | 47.5 | ||

| 9:30 | GBP | Services PMI Jan P | 51.1 | 50 | ||

| 13:30 | CAD | Retail Sales M/M Nov | 0.10% | -1.20% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | -0.20% | -0.50% | ||

| 14:45 | USD | Manufacturing PMI Jan P | 52.3 | 52.4 | ||

| 14:45 | USD | Services PMI Jan P | 53.1 | 52.8 |

{kind=link}