Yen and Swiss Franc turn softer today as global markets rebound. China’s coronavirus seems to be suddenly off investors mind, at least temporarily. Meanwhile, Australian Dollar is the strongest one for today, as partly supported by RBA’s hold, as well as easing risk aversion. Canadian Dollar follows as the second strongest. Though, upside of Loonie is limited by weakness of WTI oil price, which breaches 50 handle.

Technically, with today’s recovery, USD/JPY’s focus is back on 109.26 minor resistance. Break will suggest that pull back from 110.28 has completed at 108.30. That will also argue that larger rebound from 104.45 is not completed. While AUD/USD recovers today, it’s kept well below 0.6777 resistance. Near term outlook remains bearish with focus on 0.6670 low. Decisive break there will resume medium term down trend.

In Europe, FTSE is up 1.42%. DAX is up 1.40%. CAC is up 1.46%. German 10-yaer yield is up 0.038 at -0.403. Earlier in Asia, Nikkei rose 0.49%. Hong Kong HSI rose 1.21%. China Shanghai SSE rose 1.34%. Singapore Strait Times rose 1.29%. Japan 10-year JGB yield rose 0.005 to -0.050.

Eurozone PPI at 0.0% mom, -0.7% yoy

Eurozone PPI came in at 0.0% mom, -0.7 yoy in December, matched expectations. Non-durable consumer goods rose 0.5% mom, capital goods rose 0.1%. Intermediate goods and durable consumers goods dropped -0.1% mom. Energy dropped -0.5% mom. Total industry exclude energy rose 0.1% mom.

EU27 PPI was at 0.2% mom, -0.4% yoy. The highest increases in industrial producer prices were recorded in the Netherlands and Romania (both +0.5% mom), and Greece (+0.4% mom), while the largest decreases were observed in Estonia (-1.3% mom), Portugal (-1.0% mom) and Finland (-0.7% mom).

UK construction PMI rose to 48.4, downturn lost intensity

UK PMI Construction rose to 48.4 in January, up from 44.4, beat expectation of 44.9. While that still suggests contraction, it’s the best reading since May 2019. New orders were close to stabilization. There was a boost from receding political uncertainty. Business optimism also rebounded to its highest since April 2018.

Tim Moore, Economics Associate Director at IHS Markit, said: “The construction sector downturn lost intensity in January amid slower reductions in house building, commercial work and civil engineering activity. Measured overall, the latest dip in construction output was much shallower than in December, with survey respondents often commenting on improved willingness to spend among clients since the general election.”

BoJ paying maximum attention on China’s coronavirus outbreak

BoJ Governor Haruhiko Kuroda pledge to “pay maximum attention” to China’s coronavirus outbreak and the impact on Japan’s economy, prices and financial markets. He added that BoJ has been gathering information and exchanging views with global counterparts. And, “we will make sure to take necessary measures when needed.” But for now, “it is too early to adopt further easing steps at the moment,” he said.

RBA keeps cash rate at 0.75%, no indication of rate cut

RBA left cash rate unchanged at 0.75% as widely expected. Australian Dollar recovers as there is no clear sign of imminent rate cut. The central just said “due to both global and domestic factors, it is reasonable to expect that an extended period of low interest rates will be required.” The board “remains prepared to ease monetary policy further if needed”.

RBA expects the economy have a “step up” and grow around 2.75% in 2020 and 3.00% in 2021. Bushfires and coronavirus will “temporarily weigh on domestic growth”. But overall outlook is “supported by the low level of interest rates, recent tax refunds, ongoing spending on infrastructure, a brighter outlook for the resources sector and, later this year, an expected recovery in residential construction.”

Unemployment rate is expected to “remain around” 5.1% for some time, before “gradually declining” to a little below 5% in 2021. Wage growth is “subdued” and is expected to “remain” at current rate for some time. Inflation remains “low and stable”. CPI is expected to be around 2% in the near term and “fluctuate around that rate over the next couple of years”.

Suggested readings on RBA:

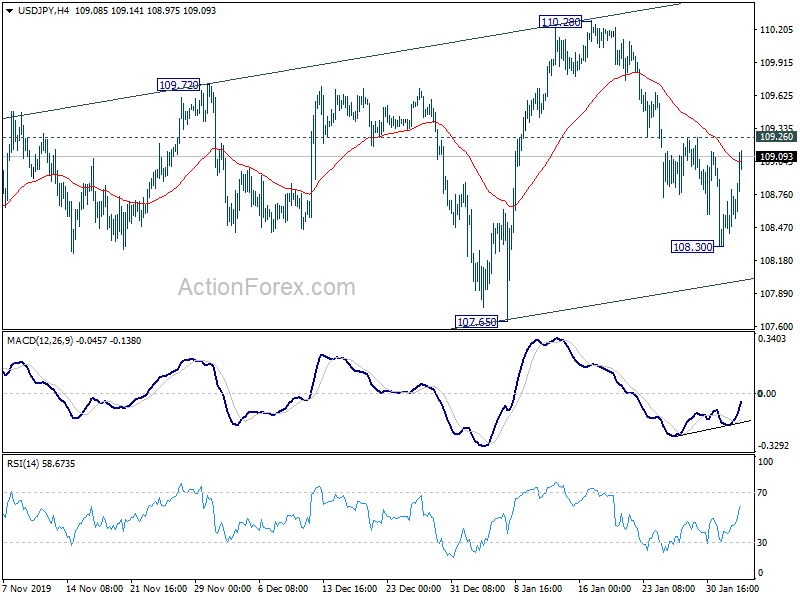

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.41; (P) 108.60; (R1) 108.89; More..

Current development suggests that a temporary low is formed at 108.30 in USD/JPY. Intraday bias is turned neutral first with focus back on 109.26 minor resistance. Break will suggest that pull back from 110.28 has completed. More importantly, larger rebound from 104.45 is still in progress. Intraday bias is back on the upside for retesting 110.28 first. on the downside, break of 108.30 will resume the fall to 107.65 support next.

In the bigger picture, there is no change in the bearish outlook yet in spite of the rebound from 104.45. The pair is staying in long term falling channel that started at 118.65 (Dec. 2016). Rise from 104.45 is seen as a correction and the down trend could still extend through 104.45 low. However, sustained break of the channel resistance will be an important sign of bullish reversal and target 114.54 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | 9.90% | -8.50% | -8.40% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 2.90% | 3.10% | 3.20% | |

| 3:30 | AUD | RBA Interest Rate Decision | 0.75% | 0.75% | 0.75% | |

| 9:30 | GBP | Construction PMI Jan | 48.4 | 44.9 | 44.4 | |

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.00% | 0.00% | 0.20% | 0.10% |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | -0.70% | -0.70% | -1.40% | |

| 15:00 | USD | Factory Orders M/M Dec | 0.70% | -0.70% |

{kind=link}