Dollar rises broadly in early US session after strong ADP employment data. But it’s outshone by both Australian Dollar and Sterling. The Aussie is apparently helped by return of risk appetite as well as an RBA’s governor that’s comfortable with current monetary policy. On the other hand, Swiss Franc and Euro are the weakest ones, dragged down by selling against Sterling. Yen is not far away as the third weakest.

Technically, 0.6777 minor resistance in AUD/USD is a level to watch. Break will suggests that the pair has successfully defended 0.6670 low and bring stronger rebound back towards 0.6849 resistance. 121.60 minor resistance in EUR/JPY is another level to watch as break will align its outlook with USD/JPY, and bring retest of 122.87 high. Nevertheless, upside of EUR/JPY could be capped by decline in EUR/USD, which is now heading back to 1.0992 support.

In Europe, FSTSE is currently up 0.58%. DAX is up 1.37%. CAC is up 0.98%. German 10-year yield is up 0.0398 at -0.358. Earlier in Asia, Nikkei rose 1.02%. Hong Kong HSI rose 0.42%. China Shanghai SSE rose 1.25%. Singapore Strait Times rose 1.38%. Japan 10-year JGB yield rose 0.0164 to -0.033.

US ADP jobs grew 291k, strong among services and mid-sized businesses

US ADP report showed 291k growth in private sector jobs in January, well above expectation of 155k. By company size, small businesses added 94k jobs, medium businesses added 128k, large businesses added 69k. By sector, goods-producing companies added 54k while service-providing companies added 237k.

“The labor market experienced expanded payrolls in January,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Goods producers added jobs, particularly in construction and manufacturing, while service providers experienced a large gain, led by leisure and hospitality. Job creation was strong among midsized companies, though small companies enjoyed the strongest performance in the last 18 months.”

Also released, US trade deficit widened to USD -48.9B in December versus expectation of USD -47.4B. Canada trade deficit narrowed to CAD -0.4B in December versus expectation of CAD -1.2B.

ECB Lagarde: Coronavirus adds a new layer of uncertainty

ECB President Christine Lagarde said in Paris today, “the short-term uncertainties are mainly related to global risks – trade, geopolitical and now the outbreak of the coronavirus and its potential effect on global growth.”

“While the threat of a trade war between the United States and China appears to have receded, the coronavirus adds a new layer of uncertainty,”

Though, for ECB, Lagarde said the current forward guidance on interest rates and asset purchases acts as an effective automatic stabilizer.

Eurozone PMI composite finalized at 51.3, tide may be turning for the economy

Eurozone PMI Services was finalized at 52.5 in January, down from December’s 52.8. PMI Composite was finalized at 51.3, up from December’s 50.9. Among the member states while reported the data, Germany PMI composite hit 5-month high of 51.2. France PMI Composite dropped to 4-month low of 51.1. Italy PMI Composite hit 3-monthhigh of 50.4.

Chris Williamson, Chief Business Economist at IHS Markit said: “A further rise in the headline PMI to the highest since last August adds to evidence that the tide may be turning for the eurozone economy. Although growth remains subdued, with the survey signalling a quarterly GDP growth rate of just under 0.2%, manufacturing is showing welcome signs of stabilising after the heavy downturn seen last year and services growth remains encouragingly resilient, thanks largely to the improving labour market.”

UK PMI composite finalized at 53.3, economy picked up since general election

UK PMI Services was finalized at 53.9 in January, up from 50.0 in December. PMI Composite rose to 53.3, up from 49.3, back in expansion region for the first time since last August. Markit noted there was robust and accelerated increase in new orders. Growth expectations also continued to improve.

Tim Moore, Economics Associate Director at IHS Markit, said: “January’s PMI surveys give a clear signal that the UK economy has picked up since the general election, as a diminishing headwind from political uncertainty translated into rising business and consumer spending. We maintain our nowcast of UK GDP rising by approximately 0.2% in the first quarter of 2020, which represents an improvement on the sluggish conditions seen at the end of last year.”

Swiss SECO consumer sentiment rose to -9, economic expectations brightened significantly

Swiss SECO consumer sentiment rose to -9 in Q1, up from -10, but missed expectation of -8. It’s staying below long-term average of -5. SECO said, “consumer sentiment remains below average overall, as households’ own budget situation is still gloomy. ” Nevertheless, “expectations regarding general economic development have brightened significantly”, up from -19 to -7, just above long term average of -9.

RBA to continue to look at both sides of the rate cut equation

In an address to the National Press Club today, RBA Governor Philip Lowe said the rate hold yesterday “reflects a judgement about the benefits from a further reduction in interest rates against some of the costs and risks associated with very low interest rates.”

He added, a further cut would help households balance sheet adjustment and “bring forward the day that consumption strengthens”. It would also have a further effect on the exchange rate which would ” boost demand for our exports and therefore support jobs growth.” However, there were global concerns on the “resource allocation” and “confidence” on very low interest rates. It could also encourage more borrowing for house purchases and increase risk of problems down the track.

But the board will continue to look at “both sides of the equation”. “If the unemployment rate were to be trending in the wrong direction and there was no further progress being made towards the inflation target, the balance of arguments would change.” There would be a “strong case for further monetary easing” in those circumstances.

New Zealand unemployment rate dropped to 4%

New Zealand unemployment rate dropped to 4.0% in Q4, down from 4.1%, better than expectation of 4.2%. However, participation rate also dropped to 70.1%, down from 70.4%. Employment was actually flat versus expectation of 0.3% growth. Labor cost index rose 0.6% qoq, unchanged from Q3, slightly better than expectation of 0.5% qoq.

Also released in Asia, China Caixin services PMI dropped to 51.8 in January, missed expectationof 52.6.

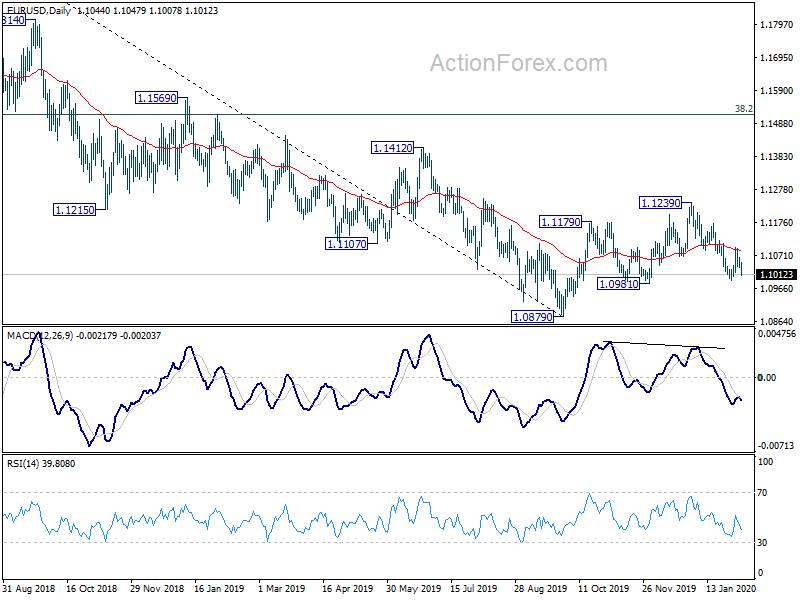

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1031; (P) 1.1047; (R1) 1.1062; More…

Focus is now back on 1.0992 support in EUR/USD with today’s decline. Break there will resume the whole decline from 1.1239. Also, that would add to the case that corrective rebound from 1.0879 has completed at 1.1239. In this case, deeper decline would be seen back to retest 1.0879 low. On the upside, break of 1.1095 will turn bias to the upside for 1.1172 resistance instead.

In the bigger picture, rebound from 1.0879 is seen as a corrective move at this point. In case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Employment Change Q4 | 0.00% | 0.30% | 0.20% | |

| 21:45 | NZD | Unemployment Rate Q4 | 4.00% | 4.20% | 4.20% | 4.10% |

| 21:45 | NZD | Participation Rate Q4 | 70.10% | 70.40% | 70.40% | |

| 21:45 | NZD | Labour Cost Index Q/Q Q4 | 0.60% | 0.50% | 0.60% | |

| 00:00 | NZD | ANZ Commodity Price Jan | -0.90% | 1.60% | -2.80% | -3.40% |

| 01:45 | CNY | Caixin Services PMI Jan | 51.8 | 52.6 | 52.5 | |

| 06:45 | CHF | SECO Consumer Climate Q1 | -9 | -8 | -10 | |

| 08:45 | EUR | Italy Services PMI Jan | 51.4 | 51 | 51.1 | |

| 08:50 | EUR | France Services PMI Jan F | 51 | 52.4 | 51.7 | |

| 08:55 | EUR | Germany Services PMI Jan F | 54.2 | 52 | 54.2 | |

| 09:00 | EUR | Eurozone Services PMI Jan F | 52.5 | 52.4 | 52.2 | |

| 09:30 | GBP | Services PMI Jan F | 53.9 | 49.1 | 52.9 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Dec | -1.60% | -0.50% | 1.00% | 0.80% |

| 13:15 | USD | ADP Employment Change Jan | 291K | 155K | 202K | 199K |

| 13:30 | USD | Trade Balance (USD) Dec | -48.9B | -47.4B | -43.1B | -43.7B |

| 13:30 | CAD | International Merchandise Trade (CAD) Dec | -0.4B | -1.2B | -1.1B | -1.2B |

| 14:45 | USD | Services PMI Jan F | 53.2 | 53.2 | ||

| 14:45 | USD | PMI Composite Jan | 53.1 | 53.1 | ||

| 15:00 | USD | ISM Non-Manufacturing PMI Jan | 55.1 | 55 | ||

| 15:30 | USD | Crude Oil Inventories | 2.9M | 3.5M |

{kind=link}